In 2008, the World Bank issued the first-ever labeled green bond in the amount of $440 million. This issuance opened up a new world of environmental finance that has experienced rapid growth: In 2015, the value of green bonds issued totaled $41.8 billion. and issuers included Apple, the government of China, and the District of Columbia Water and Sewer Authority.

Despite this and increased investment by the private sector, the pressures of population growth, consumption, and development continue to increase conservation needs around the world, while dollars for conservation are plateauing, dwindling, or fundamentally threatened. (Note, for example, the US conservation community’s battle to get the Land and Water Conservation Fund temporarily reauthorized in late 2015.) Meanwhile, investor and environmental communities continue to question what green bonds really mean for financing environmental projects around the world.

To better understand the potential of green bonds and their attendant challenges, we conducted a study in 2015 through the Harvard Kennedy School and Lincoln Institute of Land Policy. Specifically, we looked closely at a particular slice of the green bonds world: green bonds used for sustainable land use and conservation (which as we define as encompassing a broad range of land use activities, including resource extraction through sustainable forestry or agriculture, habitat restoration for the benefit of native species and people, and traditional land preservation to limit human use). Through interviews with issuers, banks, investors, and environmental organizations, we sought to develop a robust body of knowledge about green bonds, and to outline a set of next steps to encourage their responsible growth and utility. (A recent SSIR piece explores this topic from a different angle.)

Matching Supply with Demand

The major challenge to further growth, we found, lies in identifying a sufficient flow of projects that are attractive to private investors. As Charlotte Kaiser, deputy managing director of NatureVest, told us: “There’s clear supply-demand mismatch in the capital markets. There’s a ton of interest among institutional clients for conservation or environmental investment opportunities, and limited product that’s appropriate.”

Are you enjoying this article? Read more like this, plus SSIR's full archive of content, when you subscribe.

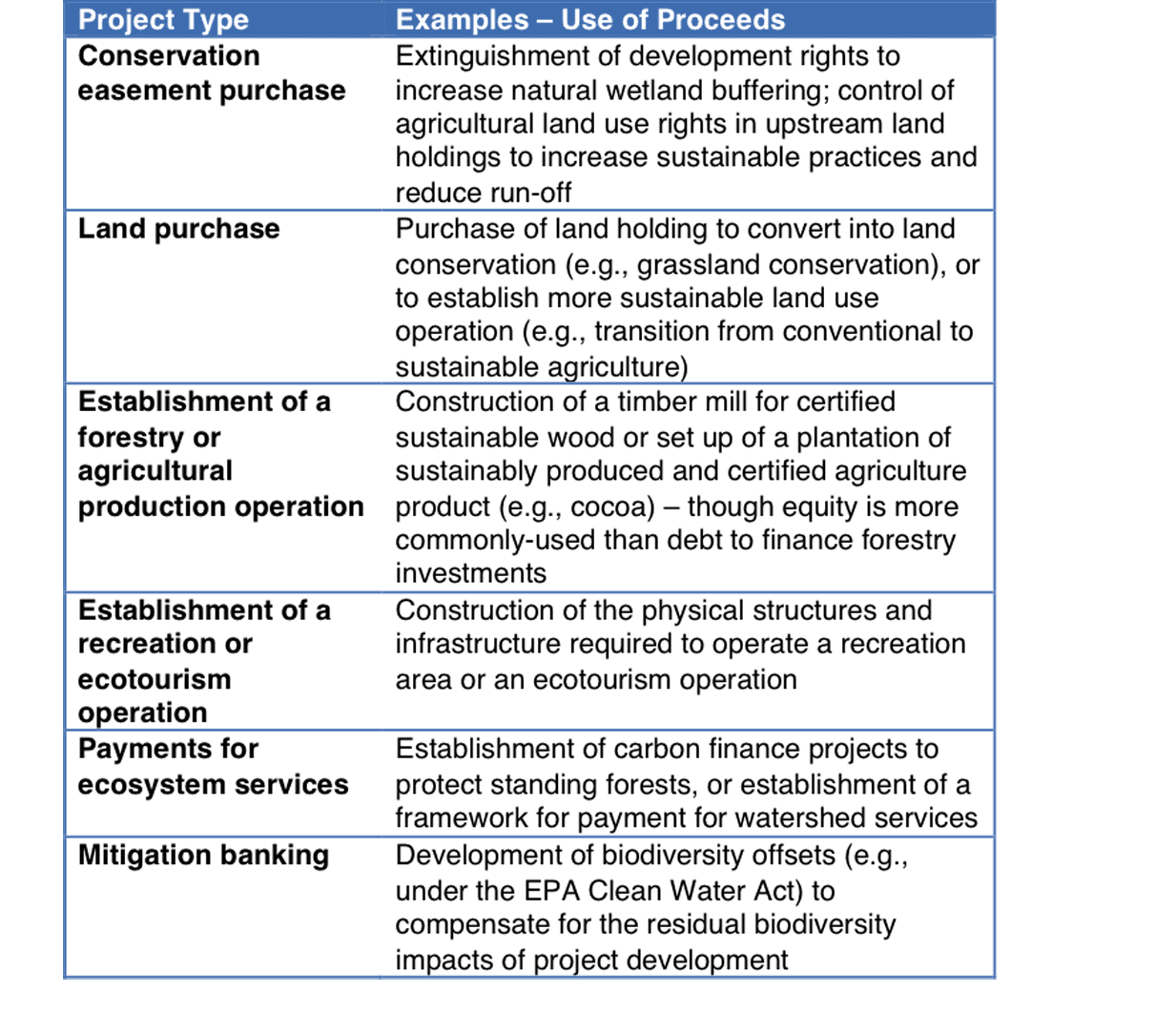

The good news is that there are opportunities to address this challenge and balance supply with demand. In fact, green bonds have the potential to finance a broad range of sustainable land use and conservation efforts, including activities such as those outlined in the table below.

Turning that potential into reality won’t be easy, but it can be done. Our research revealed six market insights that may help investors, issuers, and conversation practitioners better understand the challenge, and in doing so, find the common ground they need to scale the use of green bonds effectively:

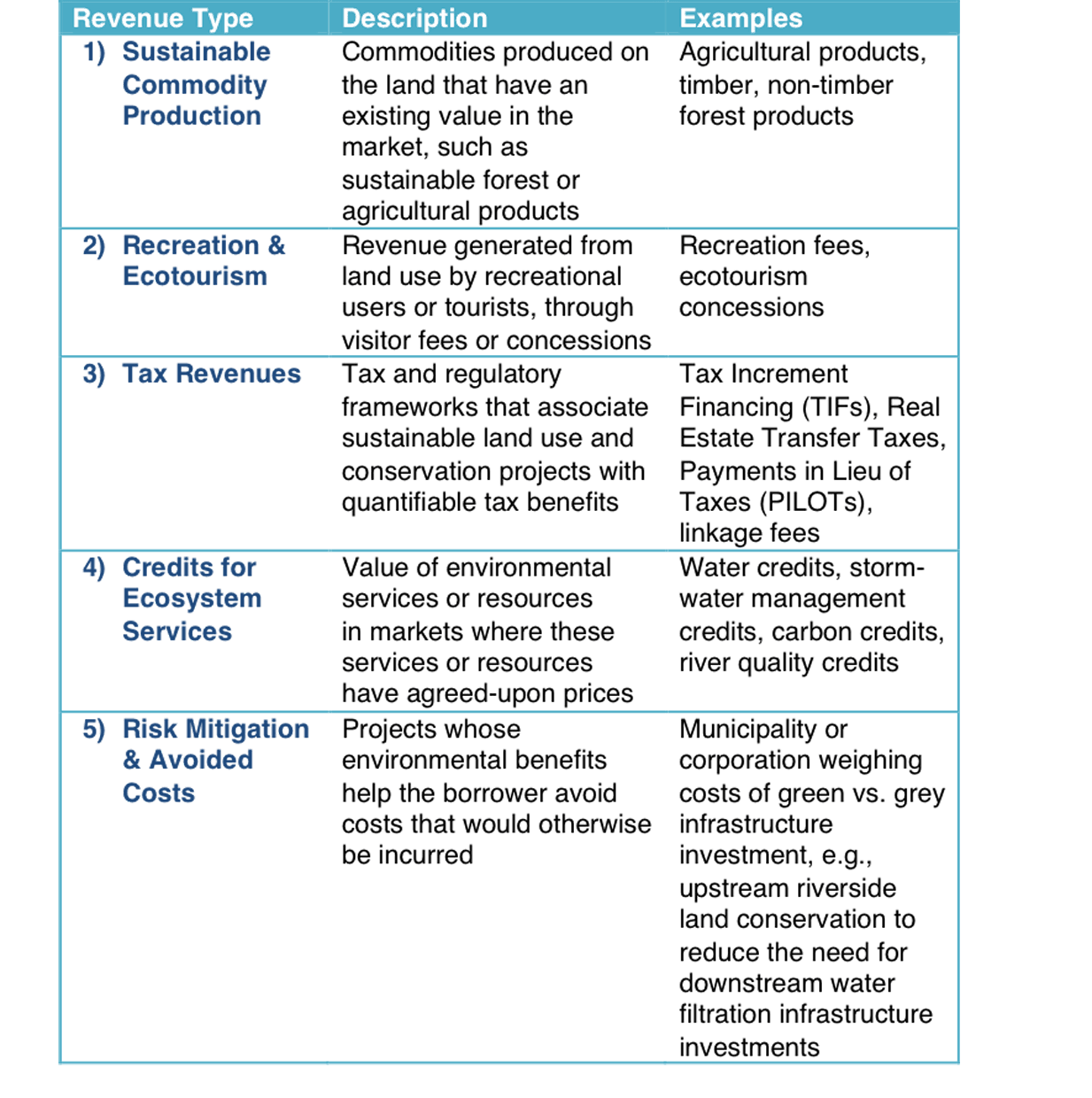

1. There’s currently not enough clarity around how land conservation projects generate cash flows to back bond repayment. It’s much more difficult to understand how a conservation project will create sustainable revenue than it is to understand, for example, how a renewable energy project such as wind development can generate revenue to repay a bond. (In the latter, physical assets can be used to back the deal, and electricity sold to the grid has a clear price and allows investors to make cash flow projections.)

The table below lays out five possible cash flow types for sustainable land use and conservation projects. While it may be possible to project future prices of commodities and recreation fees, as well as tax revenues, it is much more difficult for investors to have certainty around the value of ecosystem services credits or future avoided costs. As a result, investments structured around these types of anticipated revenues tend to be one-offs, geographically specific, and difficult to scale.

As Patrick Coady, former US executive director of The World Bank, put it: “Ecosystem financing projects are currently wrought with fundamental cash flow projection problems: They’re hard to predict, uneven, and subject to regulatory uncertainty. It’s hard to organize a security with a risk level that investors are comfortable with.”

Fabian Huwyler of Credit Suisse echoed these concerns as related to payments for ecosystem services: “Conceptually, we get what ecosystem services are all about. But if you really want to finance and implement a project based on those revenue streams, you need a regulatory environment that provides for cash flows to be generated, has an operating entity that understands what they’re doing, and has the ability to scale it up to an institutional investment level.”

2. Investors need more than project-revenue backed bonds to convince them to move forward. Investors are not ready for green bonds backed only by project cash flows. The difficulty in projecting cash flows around land conservation projects means that investors will see those cash flows as risky, which translates into a high cost of capital for the borrower. Even in cases where projects clearly generate revenue, such as a timber project, the projected revenue may not be sufficient to cover the full repayment of the bond. As a result, green bonds for sustainable land use and conservation to date have been backed by the full faith and credit of the issuing organization. Guarantees or loan back-stopping by organizations such as philanthropies may provide additional assurance around these cash flows and allow for more innovative project revenue bonds to be appealing to investors.

3. Concerns about “additionality” are justified. Of the sustainable land use projects that have been funded by green bonds to date, most if not all would have been funded in any case—by a “traditional” bond. Knowing this has led many in the conservation community to be concerned that green bonds are not actually providing any new financing for land conservation, as well as to express skepticism that green bonds are just a convenient marketing tool for issuers. Josue Tanaka of the European Bank for Reconstruction and Development summarizes the unresolved questions asked by many in the conservation and investment communities: “Are green bonds really driving incremental environmental financing, or is the green bond label just clarifying what would have been happening anyway?”

4. Green bonds do not currently offer a better cost of capital for sustainable land use projects—but this state of affairs may be changing. The conservation community, it seems, has been waiting for a clear signal that there is a benefit to pursuing green bond financing for their projects, aside from the positive marketing benefits. But to date, there is not strong evidence that green bonds provide a better cost of capital than traditional bond financing—that is, investors are not yet willing to pay a premium for the green label, and as a result borrowers are not receiving a lower cost of capital (though there are some anecdotes of instances where issuers have observed a slightly lower cost of capital than they would expect with a normal bond issuance). At the same time, green bond issuances have been consistently and significantly oversubscribed, and many experts we consulted predicted that such high levels of demand could over time result in an increased willingness to pay a premium for green bonds.

5. Matching scales in an ongoing challenge. Another “supply” issue in this equation is finding land-related deals that match the scale of green bond issuances. Large investors are seeking large projects to fund, but finding land conservation opportunities at this scale can be challenging. The average bond issuance for forestry and agriculture projects is estimated at $106 million, which is significantly larger than would be required for many smaller-scale land conservation efforts. The majority of land conservation initiatives may be too small to appeal to investors, unless multiple projects can be bundled into one issuance.

6. Efforts to define “green” may hinder the growth of the market. Many conservation organizations are skeptical about green bonds because of the lack of an agreed-upon standard definition for what constitutes “green.” Our research revealed a spectrum of opinions on this issue: Some interviewees argued that the lack of definition had to be resolved in order for green bonds to become a legitimate environmental finance tool, while others argued that as long as the criteria for a given bond issuance were clear, it was up to investors to decide whether or not to invest based on their own individual criteria for “green” investments. This conversation is unresolved, but for the moment remains a concern for land conservation organizations, which do not want to be seen as taking part in perceived “greenwashing” efforts.

The Way Forward

It’s clear that the explosive growth of green bonds has been accompanied by some significant growing pains. That doesn’t mean that they won’t turn out to be a useful and reliable conservation finance tool, however. To take advantage of green bonds and develop their applicability to land conservation, land conservation organizations and investors should work together to promote and capitalize on the momentum in the market by doing the following:

Find investment sweet spots for green bonds and land. Our research uncovered two areas of opportunity for green bonds and land conservation: state and municipal issuances, and projects related to water and stormwater. State or municipal issuances—a growing area of overall green bond issuances, with $100 million in 2013 up to $2.5 billion in 2014—work well for land conservation for a few reasons: they are at an appropriate scale to fund smaller land conservation projects, can take advantage of the solid credit rating of the issuing state, and can attract place-based investors such as foundations or family offices. Similarly, land conservation projects with a link to water, stormwater, or watershed management may be attractive candidates for green bond financing: water regulation at the federal, state, and local levels creates the foundation for the establishment of credit markets and pay-for-performance investment structures. With a price on water conservation or management, a green bond can be structured with cash flows generated from user fees, from the value of tradable permits, or even in some manner leveraging capital sources such as low-interest loans from the Clean or Drinking Water State Revolving Funds.

Publicize success stories. As more projects in these sweet spots are financed by green bonds, land conservation organizations should help spread the word. Many consulted for this project expressed the need for the “proof in the pudding”—examples of green bond issuances that support land conservation efforts. Many are waiting to see proof that investors are willing to pay for the green bonds label. That’s why it’s important to share any data that supports that particular concern may be important for growing the number of issuances related to land. Issuers and conservation organizations should highlight land-related use of proceeds as models of how these investments can be structured.

Share best practices. As these issuances increase, investors, issuers, and conservation organizations should work together to share best practices that can accelerate the learning process for land conservation stakeholders across the country and the world. Organizations including the Climate Bonds Initiative and Ceres have become hubs of information-sharing, and NRDC and others have released useful resources, such as the Green Muni Bond Playbook.

Making green bonds a meaningful new tool in the conservation finance toolkit will require collaboration across many stakeholders. Communities around the world are at a crossroads related to whether land will be used in a sustainable manner or stripped of its resources. The next few years will prove critical in determining whether or not green bonds can play a role in helping ensure that critical habitats, wildlands, and open spaces are preserved for future generations.

Support SSIR’s coverage of cross-sector solutions to global challenges.

Help us further the reach of innovative ideas. Donate today.

Read more stories by Carolyn Mansfield duPont, James N. Levitt & Linda J. Bilmes.