In November 2015, Dr. Helena Ndume, winner of the Mandela prize and Namibia's most celebrated ophthalmologist, performed cataract surgery on patients attending a blindness clinic in Omaruru, Namibia. (Photo by Brent Stirton/Getty Images)

In November 2015, Dr. Helena Ndume, winner of the Mandela prize and Namibia's most celebrated ophthalmologist, performed cataract surgery on patients attending a blindness clinic in Omaruru, Namibia. (Photo by Brent Stirton/Getty Images)

Global organizations have set ambitious goals to improve human welfare. The mission of the World Bank Group (WBG) is to eliminate poverty and promote shared prosperity. The United Nations has a unified vision for the future of health, prosperity, and development through the adoption of the 17 Sustainable Development Goals (SDGs). The World Health Organization (WHO) has prioritized universal health coverage with a target of worldwide coverage of 80 percent by 2030.

None of these goals, however, is achievable without addressing the major gaps in surgical, obstetric, and anesthesia (SOA) care. Two-thirds of the world’s population lack access to safe surgical care. An estimated 143 million additional procedures per year are needed to save lives and prevent disability.1 Closing this SOA gap through investing in surgical systems represents a critical step in achieving many of the SDGs. Improving surgical care will boost health systems, support the well-being of populations, and create a productive workforce, which will consequently drive economic growth and alleviate poverty.

There is an estimated $2.5 trillion annual spending gap between the cost of achieving the SDGs and the current funding put towards them.2 The private sector has an essential role to play in closing this gap, and investments in global surgery can lead the way in demonstrating how the private sector might do so. In what follows, we argue for a shared value approach for the surgical device and consumables industry (hereafter referred to as “Industry”)—the private for-profit companies that design, manufacture, and sell the equipment and supplies required for surgical and anesthesia care—to address the spending gap. The Industry should pursue this problem as a unique opportunity to create economic value for itself and others while addressing pressing global social problems.

The Shared-Value Approach

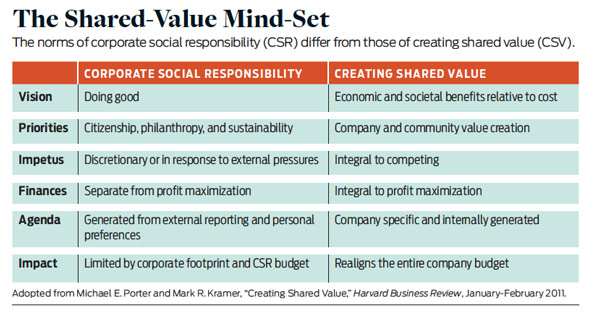

In 2006 Harvard Business School professor and management consultant Michael Porter introduced the idea of creating shared value (CSV) as a separate and distinct strategy from corporate social responsibility (CSR). Shared value holds that private industry can help address the needs and challenges of society while also generating economic value and increased business revenue. By contrast, “corporate social responsibility” is the practice by which companies uphold the social concerns of stakeholders and the public without the expectation of generating economic gains.3 (See “The Shared-Value Mind-Set” on page 48.) Shared value challenges the traditional theory that doing a societal good, such as improving access to surgical care worldwide, requires sacrificing profits based on a sense of responsibility on the part of traditional large corporations. CSR places social progress on the outskirts of a company’s mission, while CSV places it at the center.

CSR’s mission is to “do good” and is often embraced as a response to external pressures to demonstrate a company’s social value and to improve its reputation. But CSR efforts are restricted to discretionary funds, thereby limiting the success of the project. CSV shifts the core of the company’s mission to competing on the basis of improving health outcomes for new, previously underserved markets, therefore simultaneously increasing the company’s profit and benefiting society. Societal progress becomes integral to profit maximization, competition, and budget planning. Shared value recognizes that societal needs define markets and often create costs for companies that could be mitigated through addressing those needs. As Porter concludes, CSV “will drive the next wave of innovation and productivity growth in the global economy. It will also reshape capitalism and its relationship to society.” 4

The case for shared value in global surgery is straightforward. It combines the desires of Industry to find new markets for surgical goods and the needs of health ministers to mobilize resources to improve national health. Investment in surgical systems leads to increased access to surgical care and improved quality of care for those who currently lack it. The population served will enjoy improved health and economic productivity, while Industry opens new markets and creates opportunities for increased productivity in the value chain. These new opportunities, in turn, increase demand for surgical products, improve efficiency, and ultimately boost revenue. In addition, business in general benefits from helping society this way, for example through employee retention, shareholder satisfaction, customer attraction, and government responsiveness in awarding large national contracts.

The Implementation Challenge

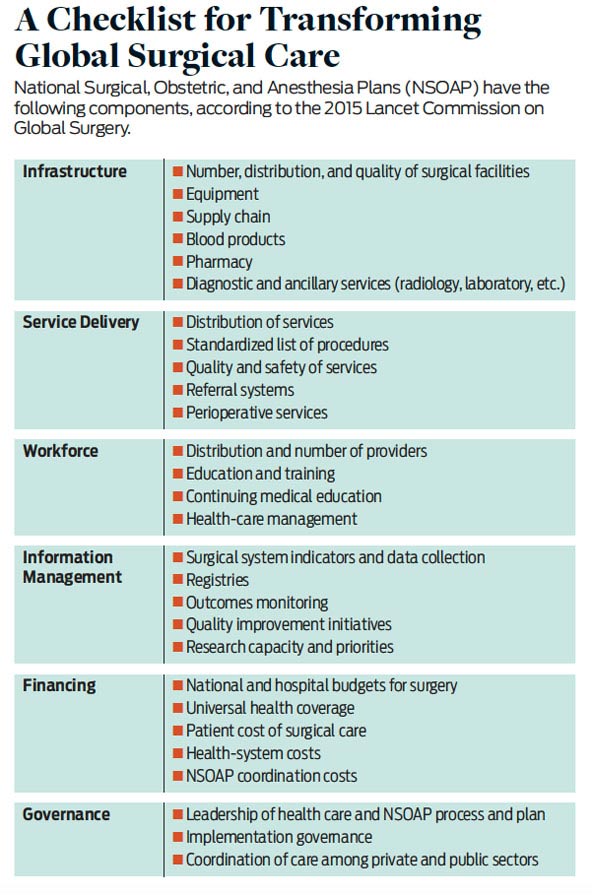

The global SOA gap represents an enormous challenge to care providers. In 2015, The Lancet Commission on Global Surgery described the current surgical landscape in low- and middle-income countries (LMICs) and provided a road map for scaling up surgical services worldwide by 2030. Specifically, it recommended that these countries develop national surgery, obstetric, and anesthesia plans (NSOAPs) to coordinate existing resources and invest strategically in new resources across health systems in order to scale up SOA service delivery. (See “A Checklist for Transforming Global Surgical Care” on page 49.) One out of five LMICs is currently developing NSOAPs and now faces the challenge of implementing them. The sheer scale of building the health system under these policies is so large that it requires ambitious commitments from a wide variety of stakeholders.

In addition to traditional stakeholders such as ministries of health, donor organizations, nongovernmental organizations, and faith-based organizations, the Industry also has the potential to play a leading role in implementing NSOAPs. It not only possesses the financial, organizational, and leadership capacity to expand surgical-service delivery, but also has strong incentives to invest in longer-term strategies that will increase surgical volume, and therefore demand, in previously untapped markets. Industry and its partners have long recognized this potential, but a lack of strategic planning has prevented them from channeling their resources to the scale required.

There is significant potential growth in the global surgery market. For equipment alone the market was valued at $10.5 billion in 2016, with an expected 10.7 percent compound annual growth rate and an estimated market size of $18.5 billion by 2025.5 Given that 73 percent of the world’s population live in LMICs, yet only 6.3 percent of surgeries are carried out in those countries, these projections demonstrate the enormous potential of the LMIC market for scaling surgical services up to even a fraction of the current rates in high-income countries (HICs).6 Economists widely acknowledge the opportunities for growth in LMIC markets: Sub-Saharan Africa, for example, saw an average annual growth rate of 4.4 percent between 2010-2015, compared with low to stagnant growth across the northern hemisphere. Health care is one of the six sectors in Africa marked for high growth and high profitability, according to a 2016 report from the McKinsey Global Institute.

Unlocking this potential, however, requires up-front investment in surgical systems to increase surgical service delivery and meet demand. The estimated total cost to scale up surgical care worldwide in all LMICs by the year 2030 is $300-$420 billion.7 At the country level, Zambia completed the first NSOAP in May 2017, with an estimated cost of $314 million over three years. Tanzania’s NSOAP will require $600 million in investment over seven years. But the cost of not scaling up services in LMICs has also been estimated, and it is enormous: A lack of surgical care will result in $12.3 trillion in lost economic productivity (or 1-3 percent of global GDP) due to otherwise avoidable disabilities and deaths by 2030.8

Up-Front Investments

Although the shared-value case for global surgery is clear, determining how the private sector can most effectively invest is not as obvious. Generating financial returns through shared value requires a long-term approach. Scaling up surgical services requires significant up-front investment long before any increase in revenue or profits is realized.

These up-front investments cannot come from traditional philanthropic donors. In this model, foundations, often funded by Industry uncoupled from their profit-making entities, provide grants to countries aimed at scaling up services. But individual foundational grants tend to focus on narrow, attainable, and short-term projects with significant overhead. Further, these efforts tend to be coordinated with implementing partners, such as NGOs or private health-care providers, rather than through the government and the public health system. These implementing partners feel a pressure for quick results to ensure further investments, and so they tend to prioritize short-term goals with more limited impact over sustainable, long-term outcomes. Additionally, under traditional philanthropic models, funding can be sporadic and unreliable, and wealthy donors hold the power to drive development agendas.

Business, by contrast, can support such up-front investments. When attempting to improve health through a shared-value lens, business aligns its interests with those of donors and ministries of health toward investing in projects which have more significant long-term impact on the health system. The financial cushion of a multibillion-dollar corporation to cover the initial period and the incentive for investors for high returns can ensure sustainable investment and improved long-term health for the population. In addition, when all stakeholders see the goal of achieving shared value, rather than charitable donations, the power dynamics change and all parties are empowered to seek more favorable terms.

This is not to say that the value of philanthropic foundations and their impact should be overlooked. Charities have made an enormous difference in many sectors, in particular by bridging resource gaps created in disasters such as earthquakes and pandemics. But only Industry can magnify the impact of their financial contributions by framing them as long-term investments, rather than acts of philanthropy, toward the implementation of NSOAPs and other health partnerships. This framing signals Industry’s durable commitment, which can attract the attention, resources, and investment of other stakeholders.

Specific Areas of Engagement

To support the development of robust systems across the health-care system and create economic value, Industry must not only invest but also play to its strengths and use its logistics and intellectual capacity. Specifically, Porter describes three ways in which companies can create shared value: (1) reconceive products and markets, (2) redefine productivity in the value chain, and (3) enable local cluster development. (See “Opportunities for Industry” on page 50.) Let us break down these proposals and consider them in turn.

Reconceiving Products and Market | The success of shared value requires an unmet need that can be satisfied by a product or company at scale. Current market forces skew innovation toward increasingly complex, high-cost, niche products that serve few patients and generate only incremental improvements in outcomes.9 But there are an estimated 5 billion people who don’t have access to surgical care—all of whom are potential consumers who require simpler solutions to common problems.10 To address this immense need, Industry must reconceive the markets they seek to serve and the products to serve them. Industry must adapt goods for the new low-resource markets they wish to provision to ensure they can be produced, used, and sold at scale. Companies can then open new high-impact emerging markets rather than continue to compete for an ever-smaller niche.

Product Design | Reaching hard-to-serve populations in difficult environments will require innovative approaches. For current NSOAPs, equipment and infrastructure represent close to one-third of the total cost for scaling up the surgical system. Successful products must be designed for the environment in which they will be utilized. Low-resource markets require products that are affordable, durable, require little maintenance, and can sustain interruptions in basic utilities such as electricity and water. Innovative products adapted in this way open access to new markets. For example, Diamedica is a for-profit company that manufactures anesthesia equipment specially designed for low-resource settings. Its machines can run without oxygen or electricity. By filling this market niche, Diamedica posted a 48 percent increase in net worth between 2016-2017 and a fourteenfold increase in net worth over the last three years.

Larger Industry partners recognize this opportunity to capitalize on innovation as well. In 2016, Medtronic, the world’s largest medical device company, launched Medtronic Labs to bring innovative products to underserved markets in order both to expand access to health care and to grow their businesses. For example, one of their initiatives, Empower Health, capitalizes on mobile devices, glucometers, and automated blood pressure machines to treat patients in West and East Africa with hypertension and diabetes. Using a novel proprietary software application, patients visit community centers where health workers check their blood pressure and glucose levels. The application records the data, and the patients receive real-time feedback on their blood pressure or glucose readings from a remote physician. On the mobile application, physicians view the data and write prescriptions that are sent electronically to the patient’s local pharmacy. Since inception, more than 100 health-care workers have been trained on this software and more than 1,100 patients have been enrolled.

Research Productivity and Development | Developing new products, more efficient delivery, and other innovations also requires strengthening the ability to design solutions in-country. Industry has the expertise, networks, and capacity to enhance research productivity and development in LMICs in order to translate basic research into innovative products and processes.11 By supporting local universities and entrepreneurs—those who are knowledgeable about local ecosystems—companies can save substantial resources in early-stage product development. For example, US medical tech firm Stryker moved research and development of orthopedic implants for the Indian market to India. This has saved costs in the development phase and helped to generate a leaner, less expensive product that is more suited to the context. The in-country research and development team, in turn, pointed out a number of other promising avenues for shared value, such as providing additional training for its products to ensure that providers can use them.12 In addition to providing savings, these local collaborations create employment and investigate opportunities in other areas that have traditionally received little investment.

After-sales Sustainability and Maintenance | In addition to innovation in production, the Industry also needs to develop better ways to ensure after-sales sustainability and equipment maintenance. All too often, equipment goes to waste after any malfunction because spare parts and service can be difficult to obtain. Purchasers recognize that LMICs lack sufficient biomedical equipment technicians (BMET).13 To address this need, companies such as Gradian Health Systems that sell affordable anesthesia machines also offer specialized training courses for anesthesia providers to help them maintain machines. This offering, in turn, builds demand for their products and creates a larger pool of biomedical technicians to improve customer satisfaction and ensure the sustainability of their products.

Redefining Productivity in the Value Chain | Industry can also lower economic costs and create jobs in the countries served by moving research and development in-country. By redefining how products are delivered and sold, Industry can make supply chains more efficient and more reliable for patients. And by increasing the skills and number of providers, companies can also quicken the delivery of the product to the remotest regions, thereby improving volume and quality of care.

Education and Training | Perhaps the greatest barrier to improving surgical care is the number of physicians and ancillary staff equipped to provide quality care.14 Industry must consider providers as a critical component of their value chain. Providers are required to wear scrub caps, use sutures, fire staplers, and order CT scans.

To create demand for new products, professionals need to have the knowledge and skills required to use them, and there must be a workforce to teach in the first place. Industry has long supported education in the surgical sector through training camps, centers, and courses. Johnson & Johnson (J&J), for example, has supported professional education through a decades-old partnership with the Nairobi Surgical Skills Centre, which trains Kenyan surgeons on new techniques and equipment. In Ghana, through the Medical and Surgical Skills Institute (MSSI), J&J has partnered for more than 10 years with local academic centers to help fund and provide supplies for the training of more than 16,000 health-care providers. Although these courses generate immense value in the short term, a reliable pipeline of new specialists is needed in the longer term.

Long-term Partnerships | Industry can vastly increase the number and density of specialist providers by supplementing the short specialist courses it provides today with longer-term partnerships. These initiatives can include full educational curricula, in-kind assistance with training materials and models, and financial support. When education is provided for a product, it has the potential to build brand loyalty and familiarity. The operators of the devices often have the most influence in purchasing decisions, and so if they become comfortable and proficient with the product, they will demand more. By supporting and expanding the skilled workforce of surgical care, more procedures will be performed, more products will be used, and more patients will be treated.

To illustrate these points, consider Novo Nordisk’s 1994 adoption of a new market-entry strategy in China. The company focused on a more holistic treatment regime for diabetes that would include physician training, patient education, and local production of insulin. At that time, there were too few educational programs in China providing diabetes education to providers in order to treat the country’s growing population of diabetics. To fill this gap, Novo Nordisk partnered with the Chinese government and the World Diabetes Foundation to develop physician-training programs for diabetes diagnosis and management. The company also supported the development of diabetes guidelines, a national diabetes program, and community-based efforts for diabetes prevention. By 2010, 220,000 physicians had received formal training to treat diabetes. Today, China is Novo Nordisk’s third-biggest market and second-largest for insulin, with a 63 percent market share and insulin sales of $711 million. In a country with 96 million diabetics, the company’s long-term commitment to diabetes education and treatment will continue to pay off through brand loyalty, profit, and saved lives.

Supportive Supervision Programs | Companies can also offer educational programs outside of teaching hospitals. In many high-income countries, medical-device representatives join the surgeons in the operating room to provide intraoperative education and after-sale support. Companies could adopt a similar model for LMICs. By providing short trainings to enable specialists to fulfill the traditional role of sales support representatives, companies can also help specialists guide the use of a product while also providing general mentorship around surgical skills. This strategy offers a cost-effective way to provide after-sale education and support while also benefiting surgical quality.

Enabling Cluster Development | In their seminal 2006 Harvard Business Review article on creating shared value, Porter and coauthor Mark Kramer describe the most successful and impactful approaches to shared value as those that act on a “cluster”—that is, all of the interrelated businesses, suppliers, communities, and infrastructure related to their product. The surgical health system is an example of a cluster. Providing equipment without offering training or ensuring a well-functioning supply chain will not increase capacity; providing training without specialists to train will not increase supply; and offering surgical services without educating communities about referral pathways to care will not increase demand.

For example, Stryker recognized the need for cluster development when it sought to win market share in India, where 80,000 knee replacements are performed annually. The company first focused on local product development by investing in trainees at its Global Technology Centre in Gurugram in partnership with All India Institute of Medical Sciences. This partnership quickly designed a knee-replacement device that has since been clinically approved and is now available at an affordable local price. Stryker soon realized that many surgeons were inadequately trained to perform joint surgery and therefore invested in hands-on training, demonstrations, and mentoring for more than 100 surgeons in two years. Stryker has since turned to infrastructure-investing by building high-quality operating rooms and support technology. Only by acting in concert with the six components of an NSOAP—service delivery, workforce, infrastructure, information management, financing, and governance—can Industry improve health-care service and create shared value.

To be sure, strengthening these pillars simultaneously is a daunting task. Scaling the degree of financial investment that Tanzania’s surgical system requires, let alone several countries or a region, represents a financial challenge beyond the capacity of any one philanthropic entity. But a coalition of Industry partners that works alongside ministries of health, NGOs, academic institutions, the transportation and energy sectors, and others to support a health cluster, holds promise.15 When a health cluster is fully supported, using local suppliers becomes easy, local training can adequately support products, the supply chain has the requisite transportation and logistics, and ultimately the whole health system, the health-care economy, the health of the society and economy are transformed.

Sustaining coalitions between multiple competing private partners and public sector can be difficult, but it is essential for any company or organization to grow in emerging surgical markets. As these markets mature, all players can benefit from new opportunities, healthy innovation, and competition that improves value for Industry and consumers alike.

Supply Chains | Weak management of supply chains hampers safe and consistent surgical service delivery and depresses demand.16 Yet this problem plagues the majority of district and regional hospitals worldwide, leading to shortages of surgical equipment and medications.17 Many surgical patients spend the most money on transportation to and from the hospital, and they incur added risk when the hospital cannot guarantee service. Because of this, patients often go to higher-level hospitals farther away from their homes in order to obtain service even for simple surgical problems.18 This circumvention of the referral system leads to a highly inefficient distribution of patients, with higher-level centers overrun with simple diagnoses and lower-level hospitals with no patients and empty beds. This trend, in turn, limits surgical volume to only a few hospitals, some of which operate well over capacity.

Industry partners can apply logistics to help stabilize and streamline the surgical supply chain, and thereby increase the number of sites providing care, and ultimately the surgical volume and demand for Industry products. For example, Novartis recognized the massive underserved health market of rural India, which is home to 70 percent of the country’s population. Novartis quickly realized that its unreliable supply chain depressed growth and soured patients on the health system. Among other strategies, Novartis invested heavily in a dense network of local distributors to reduce shortages.

Industry could see additional gains by improving supply chains more broadly. Failures along one supply chain, such as surgical sutures, can depress downstream demand for other complimentary products, such as hernia meshes or implants. Industry partners that address all the needs related to a new surgical product (such as hospital delivery, training, and maintenance) will not only strengthen surgical supply chains and stabilize delivery of care, but also increase demand for their products.

Management Capacity | Finally, Industry can also improve surgical systems by supporting management capacity, which has a known correlation with health-system performance. Researchers have identified weak management as a major barrier to health-systems development in LMICs.19 Industry offers a wealth of expertise in this area.20 In 1956, General Electric founded Crotonville, the first and arguably most successful corporate university in the world, after it determined that management capacity limited its growth.21 In low-resource settings, the responsibility of health-care management often falls on clinicians, who are already overwhelmed and have little managerial experience.22 By offering management education, Industry can contribute to building a new generation of health managers who will improve the surgical system and the health system more broadly, as well as contribute to stronger health clusters and shared value.

Limitations to the Model

The shared-value model offers an approach sufficiently ambitious to address the scale of the global surgery problem and yet practical enough to be implemented with clear, concrete steps. But it is not immune from criticism. For starters, skeptics and development traditionalists may question any partnership with private, for-profit corporations. For example, despite many successes, World Bank Group President Jim Yong Kim has drawn the ire of development economists for seeking to use private capital markets to finance WBG partnerships with the financial sector and transform the WBG’s role in international development.

The shared-value model aims to align incentives between private sector corporations and public or nonprofit development projects, but this balance can be difficult to strike. While governments and development organizations are responsible to the communities they support through social investment, corporations must also balance their fiduciary responsibility to shareholders. Tension and market failures are inevitable. Generating acceptable returns—both financial and social—is a challenging undertaking on its own, and requires patience and adaptability.

In addition, partnerships with Industry can also be fragile. NGOs are likely to remain committed to underlying causes, and health ministries remain responsible for the health challenges of their constituents. By contrast, Industry partners that view development projects as investments may more readily seek to shut down programs that do not meet profit targets and reallocate resources to more profitable ventures. As the shared-value model gains traction, it will be important to create incentives and contracts with local health systems to ensure long-term commitments to provide a reasonable return on investment to Industry for the risks they assume in any shared value project.

Global surgery offers too much business promise to remain simply a cause for charity. It must become recognized as a viable model for creating shared value and economic growth that will help close the $2.5 trillion annual funding gap needed to meet the SDGs. Investment in global surgery can produce significant economic value for Industry, improve human welfare, fulfill the moral imperative for health equity, and spark economic productivity in countries and whole regions. Charity alone will never achieve these ends. Only the creation of shared value sets us on the right path.

This article appeared in the Fall 2019 issue of the magazine with the headline: “A Surgical Roadmap for Global Prosperity”

Support SSIR’s coverage of cross-sector solutions to global challenges.

Help us further the reach of innovative ideas. Donate today.

Read more stories by Kristin A. Sonderman, Isabelle Citron, Alexander W. Peters & John G. Meara.