(Photo by Holly Lindem)

(Photo by Holly Lindem)

Though it occurred a dozen years ago, the sale of Ben & Jerry’s continues to haunt social entrepreneurs. The sale’s notoriety keeps growing, moreover, because of the central role it plays in current debates over the development and enactment of new US corporate forms—such as low-profit limited liability corporations (L3Cs), benefit corporations, and flexible purpose corporations—that attempt to embed a company’s social mission into its legal structure.

The story of Ben & Jerry’s is a legend in two acts. In Act One, Ben Cohen and Jerry Greenfield, two underachievers with counterculture values, open an ice cream store in a renovated gas station in South Burlington, Vt. The company, founded in 1978, becomes a social enterprise icon. It is fair to its employees, easy on the environment, and kind to its cows. The company pioneers the pursuit of business with a double bottom line—profits and people—that Cohen and Greenfield called the “double dip.” In its heyday (circa 1990), the company was a kind of corporate hippie, wearing its convictions on its labels with funky-named flavors like Cherry Garcia, Whirled Peace, and Wavy Gravy. Peace, love, and ice cream!

In Act Two, set in 2000, the mood sours. Ben & Jerry’s is sold (out) to Unilever, the world’s third-largest consumer goods company, described by one commentator as “a giant multinational clearly focused on the financial bottom line.”1 News of the sale sends “shudders and shivers through the socially responsible business community.”2 An all-too-brief and unexpectedly wonderful trip becomes a bummer. If Ben & Jerry’s was a kind of corporate Woodstock, this sale was its Altamont. (As a fitting coda, Unilever discontinued Wavy Gravy in 2003 because it wasn’t profitable enough.)

This article aims to dispel the idée fixe that corporate law compelled Ben & Jerry’s directors to accept Unilever’s rich offer, overwhelming Cohen and Greenfield’s dogged efforts to maintain the company’s social mission and independence. Contemporaneous observers concluded thus, such as the stock analyst who claimed in 2000 that “Ben & Jerry’s had a legal responsibility to consider the takeover bids. … That responsibility is what forced a sale.”3 Cohen says the same thing—on a 2010 NPR radio segment on social enterprise, he said that “the laws required the board of directors of Ben & Jerry’s to take an offer, to sell the company despite the fact that they did not want to sell the company.”4 Greenfield agrees: “We were a public company, and the board of directors’ primary responsibility is the interest of the shareholders. … It was nothing about Unilever; we didn’t want to get bought by anybody.”5

Corporate law has been fingered as the culprit in Ben & Jerry’s sale, which has become the poster child, proof text, and Exhibit A for the proposition that the traditional business corporation is fundamentally inhospitable, if not outright hostile, to social enterprise. Consider this passage from the summer 2009 issue of the Stanford Social Innovation Review: “[A]mong social entrepreneurs, Unilever’s purchase of Ben & Jerry’s serves as a cautionary tale of how easily corporate fiat can undermine social responsibility. ‘The board was legally required to sell to the highest bidder,’ says [an attorney with expertise in social enterprise]. Neither Ben Cohen nor Jerry Greenfield wanted to sell the company, but because it was public they had no choice.”6

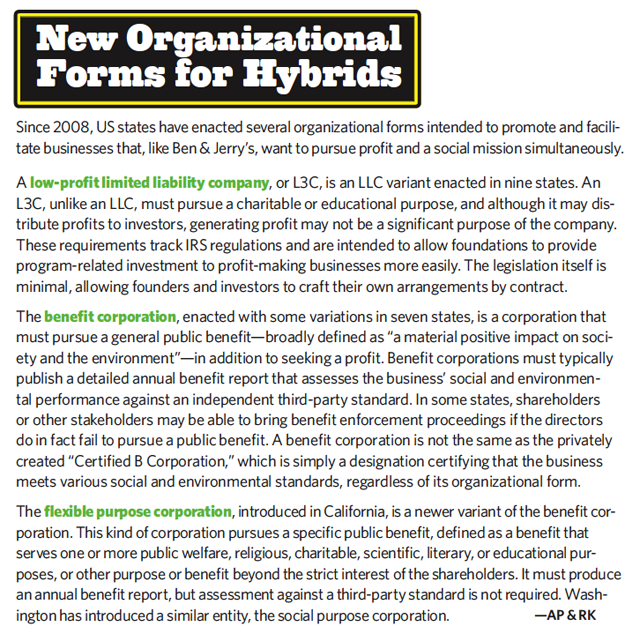

If the corporate form is bad for social enterprise, social entrepreneurs should use more suitable alternatives. Proponents of new legal forms—such as L3Cs, benefit corporations, and flexible purpose corporations—invariably cite the sale of Ben & Jerry’s to show why such forms are necessary or attractive. (See “New Organizational Forms for Hybrids,” below.) For example, a legislative report on SB 201, California’s Flexible Purpose Corporation act, states that “The story of Ben and Jerry’s Ice Cream is an example of why a new entity form is sought.” It then repeats the now familiar story: “Even though Ben and Jerry did not want to sell out, they had little choice.”7

Proponents of these forms claim they could have prevented the sale of Ben & Jerry’s, and prevent future such scenarios. After Vermont enacted its Benefit Corporation Act in 2011, one commentator asserted that “If Vermont’s law had been around 11 years ago, Ben Cohen and Jerry Greenfield might not have had to sell their ice cream company. … [T]he laws of shareholder responsibility forced the hippie founders to sell, even though they wanted to keep control. Now, with today’s law, a new kind of corporation is created that prevents exactly that.”8

Because the sale of Ben & Jerry’s is a critical fixture in debates over new legal forms, it’s essential to get it right. This article challenges the canonical account of that sale. It exposes the underlying assumptions about corporate law as erroneous: Corporate law does not require publicly traded corporations to maximize shareholder wealth. We describe the elaborate machinery that Ben & Jerry’s built to resist hostile takeovers and explain why these defenses, had they been invoked, would almost certainly have worked.

The Ben & Jerry’s sale does not make the legal argument for new forms. Rather, it is a lesson in how social entrepreneurs can use existing forms in creative ways to protect an enterprise’s social mission—even if they decide to forgo such protection in the end. (Of course, if the social entrepreneur remains the sole owner of the business, such protections aren’t even necessary.) The Ben & Jerry’s story contains other lessons for social entrepreneurs, including the impact of financial performance on mission and the idea that committed decision makers are the best security for mission sustainability.

From Humble Beginnings

When Cohen and Greenfield first started out, they were simply trying to earn a living. It was only when the business began to take off that they began the transition toward a progressive enterprise. Cohen was disappointed that Ben & Jerry’s was “just a business, like all others, [that] exploits its workers and the community.”9 A friend, however, challenged him, pointing out that he could change whatever he didn’t like about the business. Over time, Cohen and Greenfield came to view their business as, in Cohen’s words, “an experiment to see if it was possible to use the tools of business to repair society.” At the end of each month, said Cohen, he and Greenfield would ask of themselves and the company: “How much have we improved the quality of life in the community? And how much profit is left over at the end of each month? If we haven’t contributed to both those objectives, we have failed.”10 By their own expectations, and many others’, they were extraordinarily successful.

From the outset, Cohen and Greenfield were deeply committed to Vermont’s economy and environment. They relied heavily on local suppliers of milk to make their products. They hired a local artist to design their cartons and graphics. As the company’s need for capital increased, they resisted venture capitalist financing, which typically requires relinquishing significant control over the company. Instead, it sold stock to Vermont residents, thereby reinforcing the company’s local roots. In 1985 the company formalized its philanthropy by creating the Ben & Jerry’s Foundation. Cohen endowed it with $850,000 worth of his shares, and the company agreed to contribute 7.5 percent of its pretax profits.

For a while the company thrived, but in the early to mid-1990s, Ben & Jerry’s once-stellar financial performance began to lag, even as its other bottom line—social contributions—went from strength to strength. In 1994, the company’s annual report disclosed that sales growth slowed and it had suffered its first financial loss. By 1999 the stock had dropped nearly 50 percent from its peak, because of the company’s weaker financial performance. Some investors argued that the company’s social mission was a luxury it could no longer afford.

Ben & Jerry’s anemic stock performance attracted interest from prospective buyers who thought they could manage the company more profitably. Dreyer’s Grand Ice Cream tried to buy the company in 1998, but Ben & Jerry’s board refused. Other buyers were rumored to be interested when in early 2000, Cohen and a group of investors (including Body Shop founder Anita Roddick) offered to take the company private at $38 a share—about double the stock price of a few months earlier.11 Dreyer’s made another bid, which in turn prompted Unilever to offer $43.60 a share. Although Unilever spoke about nurturing the social mission, many observers were skeptical.

Despite reported reluctance, Ben & Jerry’s board announced on April 11, 2000, that it had approved Unilever’s offer. (Melodramatically, some refer to this day as “4/11.”) The transaction, valued at $326 million, was finalized with overwhelming shareholder support. Cohen’s and Greenfield’s shares were worth close to $40 million and $10 million respectively. After more than 20 years as an independent enterprise, Ben & Jerry’s became a wholly owned subsidiary of Unilever.

The deal, according to Ben & Jerry’s securities filings, contained some provisions intended to maintain the corporation’s social mission. Although Unilever controlled the financial and most operational aspects of Ben & Jerry’s, the subsidiary had its own independent board of directors to help provide leadership for the social mission and the brand’s integrity. The new board included Cohen and Greenfield, and its members, not Unilever, would appoint their successors. Moreover, this subsidiary board had the right to sue Unilever, at Unilever’s expense, for breaches of the merger agreement.

Unilever also promised to continue contributing pretax profits to charity, maintain corporate presence in Vermont for at least five years, and refrain from material layoffs for at least two years. Finally, Unilever agreed to contribute $5 million to the Ben & Jerry’s Foundation, award employee bonuses worth a total of $5 million, and dedicate $5 million to assist minority-owned and undercapitalized businesses.

Ben & Jerry’s today is described on Unilever’s website as a “wholly owned autonomous subsidiary of Unilever.” Although Ben & Jerry’s has clearly preserved some of its unique values, most observers are disappointed. Cohen and Greenfield too have reportedly “expressed concerns that the company has shifted away from its original mission of social responsibility.”12 As was stated in a post on the Stanford Social Innovation Review’s blog, “[n]obody wants to end up like Ben & Jerry’s.”13

The Legal Landscape

It is widely believed that corporate law forced Ben & Jerry’s directors to accept Unilever’s rich offer and sell the company. This perception reflects the erroneous view that corporate directors must always act to maximize shareholder value. The best and arguably only support for this view is from Dodge v. Ford, a 1919 decision from the Michigan Supreme Court. That court opined that a “business corporation is organized and carried on primarily for the profit of the stockholders.”

Dodge v. Ford is an anomaly, as other courts have not followed its view of shareholder primacy. In the blunt words of respected Cornell Law School corporate law professor Lynn Stout, “shareholder wealth maximization is not a modern legal principle.”14 Other state courts have recognized this, including New Jersey’s Supreme Court, which stated that “modern conditions require that corporations acknowledge and discharge social as well as private responsibilities as members of the community within which they operate.”15

Most state legislatures have resisted the tenets of Dodge v. Ford by enacting statutes that expressly authorize corporate directors to look beyond shareholder wealth maximization. Vermont enacted one, nicknamed “the Ben & Jerry’s law,” after the company had successfully lobbied Vermont’s legislature. Vermont’s “other constituency” statute, as these laws are called, is illustrative: It provides that when directors make decisions they may consider such matters as “the interests of the corporation’s employees, suppliers, creditors, and customers; the economy of the state, region, and nation; [and] community and societal considerations, including those of any community in which any offices or facilities of the corporation are located.” State statutes also give corporations wide latitude to donate profits to charities.

In practice, courts are deferential to board decision making. Under a doctrine called the business judgment rule, unless the directors have a conflict of interest, nearly all board business decisions are beyond judicial review. If there is a potential benefit to shareholders, the courts will not interfere. In this way board decisions advancing a social mission are effectively immune from challenge; there’s no limit to the human mind’s ability to conceive of some benefit accruing to shareholders at some point, even if in the far-distant future. Absent special circumstances, a board’s decision to reject a proposed merger would easily survive a court challenge.

Was Corporate Law the Villain?

By the time Unilever approached Ben & Jerry’s in early 2000, the company was well defended. Its founders, lawyers, and lobbyists had taken many steps to prevent a hostile takeover. In addition to promoting Vermont’s enactment of an “other constituency” statute, the company had adopted a “poison pill.” A poison pill thwarts hostile acquisitions by making them prohibitively expensive. To cancel a poison pill, an acquirer must either find a friendly board or get one elected. Because elections for Ben & Jerry’s board were staggered, an acquirer would need at least two elections scheduled a year apart to elect the board of its choice.

In the case of Ben & Jerry’s, Unilever could not have elected a friendly board, as the two founders and another early employee, director Jeff Furman, effectively controlled enough votes to direct the election of board members. The company had two classes of common stock, one with 10 votes per share and the other with one vote, and between them they held three-quarters of the super-voting stock. (This capital structure was not unique to Ben & Jerry’s. The New York Times Co. and Google, for example, have issued super-voting stock to enable their heirs or founders to maintain control.)

Faced with an entrenched unfriendly board, a would-be acquirer might have gone to court claiming that corporate law required the board to redeem a poison pill. If the court chose to scrutinize the situation carefully, it would have examined whether the board’s failure to redeem a pill was reasonable in relation to the threat that Unilever posed to Ben & Jerry’s. The legal standard is murky, but there have not been many cases where courts have ordered a pill’s redemption.

Finally, Unilever might have asserted that Ben & Jerry’s was for sale and so the board was obliged to sell the company to the highest bidder. This was unlikely for two reasons. First, although Vermont courts have not been presented with this situation, most state courts that have considered it have rejected any such obligation. Second, even if the obligation might theoretically exist, this situation was unlikely to trigger it. Although it’s true that the board was considering a sale, it had not committed itself. If the matter were litigated, most courts would hold that there was no obligation to sell on grounds that neither the breakup nor sale of Ben & Jerry’s was inevitable.

Suppose, however, that a Vermont court had required the board to act to redeem its poison pill or enter into a merger agreement. Cohen and Greenfield still had one more card to play in order to preserve Ben & Jerry’s independence. A board’s decision to redeem a pill merely allows a tender offer to be submitted to shareholders for their approval. It does not mean the offer will succeed. If a majority of shareholders do not agree to tender their shares for sale, the attempted takeover fails. If they did not tender, they retained their stock and their control of the company.

Similarly, even if the board approves a merger, although it’s a legally binding obligation, shareholders must vote in favor of the merger before it becomes effective. Because of the principal stockholders’ ownership of super-voting stock, a hostile acquirer could not have gained voting control of the company or a merger finalized without their approval.

The crucial point is that even if Ben & Jerry’s directors had a fiduciary duty in their capacity as directors to accept or facilitate a transaction, they had no such duty in their capacity as shareholders, and as such were empowered to support or oppose the transaction as they saw fit. As shareholders, they were entitled to enjoy the benefits of selfish ownership, which ironically in this context could have been exercised altruistically to maintain the company’s social mission.

If the super-voting stock were somehow insufficient, Ben & Jerry’s had yet one more defense: an unusual class of preferred stock that held veto rights over mergers and tender offers. The Ben & Jerry’s Foundation owned all of this preferred stock. A takeover of Ben & Jerry’s thus required the foundation’s agreement, and two of the three directors of the foundation were the same principal stockholders. The foundation itself could not be taken over because its board members selected their own successors. In any event, the foundation’s directors were unlikely to be sued because the only party who could sue them was Vermont’s attorney general.

There is one complication in the analysis above. For reasons that are unclear, Ben & Jerry’s organizational documents granted the board the right to redeem the preferred and super-voting stock. It is an interesting question whether a court would ever find that a board’s fiduciary duties required the redemption of these securities in order to eliminate their voting rights. The board would, after all, owe fiduciary duties to the holders of super-voting stock, and a duty of good faith and fair dealing to holders of the preferred stock. Ben & Jerry’s own public statements support this analysis. The company’s securities filings disclosed that its capital structure would make it difficult for a third party to acquire control if the transaction were not supported by the principal stockholders or the foundation.

Nonetheless, this possible loophole shows only that Ben & Jerry’s didn’t get its defenses quite right, not that some flaw in corporate law required the sale. Shrewder lawyering would have made Ben & Jerry’s corporate independence even more unassailable. Corporate law permitted super-voting stock and the granting of a veto to a charitable foundation. Moreover, corporate law allows directors to reject an offer, at least where the directors have not irrevocably committed themselves to a sale.

Although Ben & Jerry’s legal defenses to a forced sale appeared impregnable, the board unanimously agreed to sell the company. Why? Some cynically claim that the founders were ready to cash out. After all, Cohen and Greenfield grossed nearly $50 million from the sale. Moreover, Ben & Jerry’s faced some operational issues that a takeover could solve, such as product distribution. People close to the decision say they were motivated by fear of litigation, followed by a judgment that they would have to satisfy personally. If the directors were held personally liable—a remote possibility—Ben & Jerry’s charter included a provision that would have indemnified them.

Lessons for Social Entrepreneurs

This revised and richer account of Ben & Jerry’s sale offers valuable lessons for aspiring social entrepreneurs. The legal consequences of an entrepreneur’s choice of for-profit organizational form are likely to be smaller than often portrayed. Financial success is also essential to staying is control. Most important, the chief safeguard for maintaining the social mission is the people in control.

A hybrid legal form is neither necessary nor sufficient to maintain a social enterprise | Although the publicly traded corporate form can be challenging, many businesses employing it have pursued social missions with vigor and endurance. The list includes prominent firms such as The New York Times Company, Whole Foods, Starbucks, and the Body Shop (before it encountered operational problems unrelated to its form), and less well-known companies like EV Rentals and Interface Carpets. These firms use several strategies, legal and nonlegal, to ward off hostile takeovers. Foundations and super-voting stock are not uncommon. In some cases, new forms include provisions that could make an enterprise’s social mission harder to dislodge, yet such provisions are used by conventional for-profit corporations as well.

Financial success is critical to maintaining control | Ben & Jerry’s early financial successes enabled its founders to negotiate powerful control mechanisms from a position of strength. Ultimately the most important change at Ben & Jerry’s was not its directors’ legal ability to resist takeovers, which indeed increased over time. Rather, it was the declining health of the business itself. In its final years as an independent company, Ben & Jerry’s sales, financial performance, and stock price had stagnated, and the company faced various operational challenges.

Successful and promising companies are better positioned to take on new investors while retaining controlling positions for the founders. When Google went public in 2004, for example, with super-voting stock for the insiders, the company candidly admitted that public shareholders’ voting rights would have little impact on the company’s direction. Facebook’s 2012 initial public offering of stock allowed its founder, Mark Zuckerberg, to retain control through a combination of super-voting stock and contractual arrangements with other shareholders. (Interestingly, both companies also asserted that providing services, rather than making a profit, was their top priority.)

Although it is true that even successful companies are bought, it is also true that shareholders tend to back successful management. Put differently, takeovers often result from poor stock performance, which usually results from weak financial performance. Investment bankers commonly observe that the best defense is a high stock price. Had Ben & Jerry’s remained successful, its directors would have felt more comfortable rebuffing offers, as they had done several times before.

It’s the people! | Ben & Jerry’s defenses made the company virtually impregnable to hostile takeover. Yet in the end, Ben & Jerry’s directors chose to accept a generous offer, even at a cost to the social mission, rather than allow the company’s defenses to be tested. Anti-takeover protections are only as effective as the people positioned to use them.

Regardless of the for-profit organizational form in which a business is housed, people who exercise control over the company will usually be able to thwart its social mission. One oft-repeated objection to new forms is that they aren’t much more effective at screening out conventional for-profit people and businesses with conventional for-profit souls. So long as the organizational structure is adequate, it will be the decision makers who make the difference. The surest way to maintain a business’ social mission is to put committed people in charge. (Cohen and Greenfield attempted to achieve this by negotiating the creation of an independent and robust board for the post-acquisition subsidiary.)

When critics claim corporations are inherently pathological, they mean that they encourage antisocial decision making by their employees. Executives at hybrid forms likely feel less pressure to maximize profits at society’s expense. Yet the causation is uncertain: Does a virtuous form make directors more virtuous, or do the virtuous seek out businesses so formed?

Conclusions

Because new forms are being represented as correctives to the cause of Ben & Jerry’s sale, it’s critical to identify the true causes and manner of what happened. Hence the irony. The full account of that sale does not make the case for new forms; rather, it illustrates how social entrepreneurs can use existing forms to protect an enterprise’s social mission—even if they choose not to assert such protections. Proponents of benefit corporations and the like should be pressed to identify real and unavoidable instances of the Ben & Jerry’s scenario, or stop using it to demonstrate the dire need for such forms.

Of course, even if new forms for social enterprises are not legally necessary, some structural innovations might prove useful nonetheless. A standard form, “off-the-rack” legal entity designed expressly for social enterprise would presumably save rising social entrepreneurs the trouble of (re)discovering tested solutions to its perennial challenges. A distinct legal form might also convey information and influence perception, for example, by assuring investors and potential investors that the company’s managers will not pursue profits über alles, and perhaps cultivating consumer loyalty to a social enterprise brand.

To date, a significant amount of resources has been devoted to developing social enterprise forms and lobbying states to enact them. As an exercise in political entrepreneurship, this strategy has produced results: Eight states have L3Cs, seven states have benefit corporations, and one has a flexible purpose corporation. It is an open question, however, whether this approach fosters more social innovation than would otherwise occur, or promotes it more effectively.

Social entrepreneurship might benefit from states competing to become the Delaware of an emerging “social enterprise law.” At the same time, fueling this competition yields diminishing returns. When a form has been enacted in one state, it is available to residents of every state. You don’t have to live or operate in Vermont to set up a Vermont L3C. What then is the point of pressing more states to enact the L3C, which is primarily intended to attract capital from relatively sophisticated investors—namely, grantmaking foundations?

We should remember that what really matters is not the organizational form but rather the formation and flourishing of social enterprises. It remains to be seen whether new forms will nurture new social enterprise icons or be an unhelpful (but tasty!) distraction. By moving beyond the received wisdom on the Ben & Jerry’s sale, we can better focus our energy on where it will do the most good.

Support SSIR’s coverage of cross-sector solutions to global challenges.

Help us further the reach of innovative ideas. Donate today.

Read more stories by Antony Page & Robert A. Katz.