Today, Haiti is still struggling to regain its footing more than a year after a disaster that literally shook the ground beneath it – with 250,000 people killed, 500,000 displaced, and a cost to the economy estimated between $7.2 billion and $13.2 billion (according to the Inter-American Development Bank). As if the initial effects weren’t bad enough, a series of additional challenges followed the earthquake: controversy about presidential candidates and alleged fraud in the election on November 28, the destruction wrought by Hurricane Tomas, an ongoing and deadly cholera epidemic, and riots brought on by growing resentment of international agencies and donors.

Though money has poured into Haiti for disbursement by aid organizations such as the American Red Cross, Mercy Corps, and World Vision, security concerns and scant use of traditional banks made distributing cash difficult and slow. In cash-for-work programs and other cash-based interventions, there are security concerns for both staff and beneficiaries. The threat of riots when payments are delayed is an ever-present concern for payers, while beneficiaries face the risk of being robbed on their return home. For those arriving home safely, saving can be a difficult proposition; Haitians’ immediate needs are so great and so many of them lack stable employment in competitive, productive markets.

In this context, I’m co-leading Dalberg’s research on the potential for new mobile-based payment systems that offer a safer, more affordable, and faster alternative to distributing cash in a country where 85% of households have access to a mobile phone (according to Voila, a mobile network operator) but only 10% of the population is served by the financial sector (in a study by USAID). This potential was the impetus for the Haiti Mobile Money Initiative (HMMI), a joint program of the Gates Foundation and the U.S. Agency for International Development (USAID) that is using a $10 million incentive fund to spur the growth of the mobile money industry. The program is managed by Haiti Integrated Finance for Value Chains and Enterprises (HIFIVE), an innovative division of USAID working to improve access to financial services.

After interviewing people from across the mobile money ecosystem in September and October 2010 in Port au Prince, and learning about the myriad challenges to launching mobile money, it was great to see two partnerships of mobile network operators and banks successfully launch mobile-phone-based virtual wallets and begin competing for shares of the HMMI fund by expanding their clientele. The award of the HMMI’s first cash prize – $2.5 million to Digicel and Scotiabank – marks a major milestone in the evolution of Haiti’s mobile money industry: the first partnership to reach 10,000 transactions spread across 100 mobile money agents.

With this milestone, mobile money is beginning to realize its potential for making cash-for-work and other aid programs faster and more cost- effective. Questions remain, however, as non-governmental organizations (NGOs) such as World Vision and Mercy Corps begin to rely on mobile money for their disbursements: What will be the overall costs and benefits? What obstacles will be encountered in implementation?

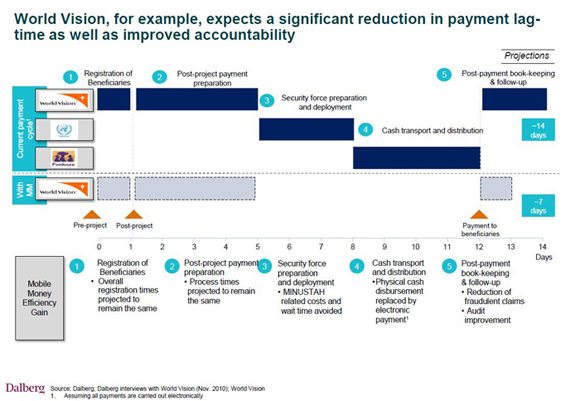

When my colleague Lorenzo Bernasconi and I interviewed leaders of these NGOs, many felt that mobile money held enormous promise for reducing registration times and costs for aid recipients, increasing the speed of cash disbursement, improving safety and privacy for clients, and increasing financial access for the majority of Haitians. Jean Capili, senior manager of innovation and partnering at World Vision, put it this way: “We are excited about the potential mobile banking has for participants in our cash for work program and for future programs that can utilize such mobile technology. It is an alternate mode of payment that is more secure and will reduce the existing number of days in which participants get paid, which in turn means they can purchase necessities for their children faster.” Indeed, World Vision estimated that the cash disbursement time-lag could be lowered by as much 50%, as illustrated below.

In mid-2011 and early 2012, we’ll carry out two additional rounds of research on the costs and benefits of mobile money for NGOs and government payers in Haiti – as well as the efficacy of the prize mechanism and the effects on Haitians’ lives. While our initial analysis delved into these NGOs expectations and plans, this subsequent analysis will begin to show how mobile-based payments work in practice. We will seek to answer questions like:

- What time and cost savings have NGO‘s realized in Haiti using mobile payment solutions?

- What were the required investments to introduce mobile money platforms?

- What are some of the key risks and challenges in using mobile platforms?

- When is distribution through a mobile banking platform more cost effective than cash?

- What has the reaction been among beneficiaries?

I am particularly excited about this research because the potential impact for programs in access to finance, agriculture, and health is so significant. These solutions, if effective, could increase delivery times, reduce corruption, improve tracking, and reduce costs for the full range of NGO programs working with cash payments. Around the world, examples already include the use of mobile-based payment solutions for cash-for-work programs, conditional cash transfers, loan repayments, and voucher programs for agricultural inputs and health care. Where mobile money platforms already exist, as in Kenya, new aid programs can build on the existing infrastructure.

In the coming months, I will be continuing this research in Haiti and working with funders and nonprofits to apply these lessons to their own portfolios of programs. Check back here for an update on our research later in the year. In the meantime, the Gates Foundation and USAID will continue to award prizes as Haiti’s mobile money industry grows.

Read more stories by Matt Daggett.