In the aftermath of a drought in North Horr, Kenya, people who are unbanked and without credit like Arbay, above, have been forced to sell their livestock to buy food. (Photo courtesy of UNICEF/UN0123957/Knowles-Coursin)

In the aftermath of a drought in North Horr, Kenya, people who are unbanked and without credit like Arbay, above, have been forced to sell their livestock to buy food. (Photo courtesy of UNICEF/UN0123957/Knowles-Coursin)

Credit cards. Bank accounts. ATMs. These are simple tools that many of us take for granted. Even if we’re struggling financially, thanks to an elaborate system of banks and credit, we often have the means to get by.

This is not the case in much of the world. The World Bank estimates that there are 1.7 billion people, or 31 percent of all adults, who are “unbanked,” and in some developing economies, it’s as high as 61 percent. Women are at an even further disadvantage, making up 55 percent of the unbanked.

These 1.7 billion people that the traditional banking system has left behind—who are often already economically challenged—have little means to easily send and receive money, build up a savings account, gain access to credit, or secure insurance. And with no financial cushion, emergencies can be devastating.

Cracking the Problem With Blockchain Technology

As Christine Moy and Jill Carlson described on the World Economic Forum blog, blockchain offers surprising promise in expanding financial inclusion to more of the world. They describe the technology as “global, open-sourced, and accessible to all who have access to the Internet, regardless of nationality, ethnicity, race, gender, and socioeconomic class.”

While many associate blockchain with cryptocurrencies like Bitcoin or Dogecoin—and perhaps to greed, illicit activity, or environmental carnage—the technology, at its core, is simply a decentralized way to organize transactions in a database, or ledger, so that multiple untrusted parties agree on the state of those transactions without the need of a middleman. All recorded transactions are immutable, transparent, and encrypted. In this sense, blockchain is redefining the role of banks, governments, or corporations by enabling financial transactions that can be more secure, cheaper, and more efficient than traditional alternatives.

For years, most of these ideas about blockchain and financial inclusion were mostly theoretical. They were abstract. Now, the theory is materializing with applications that are starting to show early results in tackling humanitarian problems. At UNICEF, as part of our Innovation Fund, we invested about $2 million in blockchain projects, and about 2,000 ether and 1 bitcoin through our CryptoFund—an effort made possible with the initial support from the Ethereum Foundation, and consequent partnerships with Animoca Brands, Chainlink, and Huobi Charity. In the last investment round, we focused on solutions that would build pathways to financial inclusion for the many people who are still excluded. We reviewed more than 400 projects and invested in eight, and while we are still validating the use of blockchain technology in a humanitarian setting, these projects are starting to improve lives in countries such as Kenya and Argentina.

Four Ways to Use Blockchain for Financial Inclusion

1. Payment services. Moving money can be expensive. Western Union can charge up to 35 percent for transfers of less than $10. This might be a minor nuisance for a wealthy New Yorker, but for someone living in Kenya, that could mean a child goes to bed hungry. Hefty fees are a problem, and so is access. The 1.7 billion people who are unbanked not only have a harder time sending and receiving money, but also often lack the means (such as a passport, proof of income, reliable Internet, and a smartphone) to open an account. Over the last decade, mobile payments showed big progress to this end. A study from the Innovations for Poverty Action, for example, found that when a Kenyan mobile money service expanded its reach, “an estimated 185,000 women changed occupations, and 194,000 households, primarily female-headed households, were lifted above the poverty line.” But mobile payments have room for improvement in the quest to financially include more people.

Chance Uwamahoro, Leaf’s engagement specialist, shows a refugee community in western Rwanda how the Leaf application works. (Image courtesy of Leaf Global Fintech)

Chance Uwamahoro, Leaf’s engagement specialist, shows a refugee community in western Rwanda how the Leaf application works. (Image courtesy of Leaf Global Fintech)

One project UNICEF has invested in is Leaf, which is based in Rwanda and allows people to send and receive money directly from their phone, even if it’s not a smartphone. No passport or internet required. As of October 2021, a total of 5,871 users (based in Kenya, Uganda, and Rwanda) completed 97,819 transactions. The average transfer from person to person is $4.97, an amount that would incur punishing fees with traditional money transmitters. Many of the users are Rwandan refugees from DR Congo—now able to receive funds from families in other countries—and others are using Leaf to buy things like food and vegetables.

We also invested in a similar Kenya-based project, called Kotani Pay, which lets Kenyans dial a short code on their phone (even if it’s a low-end mobile) to send and receive cryptocurrencies, and then to convert it to Kenyan shillings. As of October 2021, a total of 2,598 users (based in Kenya, Uganda, and Rwanda) completed 137,195 transactions. Users have transferred more than $400,000 accumulated dollars to date, and the average transfer from person to person is $1.

Both Leaf and Kotani Pay are using blockchain to enable more efficient money transfers. They provide the same benefits to a user as mobile money, to which they add a secure peer-to-peer transaction interface that operates at lower fees (free to operate and below 2 percent to cash out) and lower transaction time (3-5 seconds). As obvious as these numbers may seem to anyone in a developed country operating with apps like Venmo, access remains a pressing issue in low-income countries. The United Nations has determined that in order to reduce global inequality by 2030, we need to reduce the cost of international remittances to less than 3 percent.

While mobile money was built as a domestic option, Leaf and Kotani Pay operate on a borderless, decentralized application. This means that the only additional fee associated with international transfers is the currency conversion.

With instant, cheap, traceable transactions that can hold multiple currencies, in multiple mobile networks both nationally and internationally, blockchain applications are becoming an attractive technology to use for remittances, especially for small money transfers.

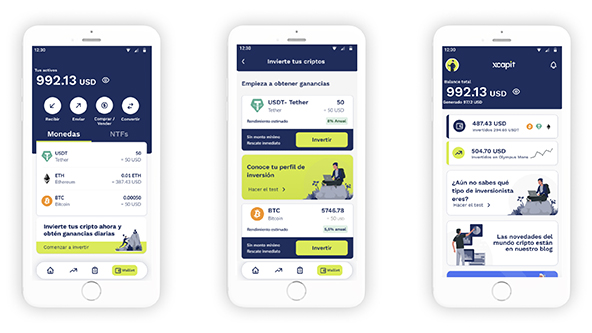

Screenshots of Xcapit’s mobile application show the total balance of the crypto wallet, the user’s assets, the total amount invested and earned. (Image courtesy of Xcapit)

Screenshots of Xcapit’s mobile application show the total balance of the crypto wallet, the user’s assets, the total amount invested and earned. (Image courtesy of Xcapit)

2. Saving. Traditionally, banks have functioned as an intermediary between people with financial surplus or shortage of money, earning the spread of the transaction (the difference between the interest rate that a bank charges a borrower and the interest rate a bank pays a depositor). While the banking system has met that aim, its complexity and high operating costs have only allowed them to do so with barriers to entry that leave many behind. In fact, much of the world has no access to savings accounts, meaning that if villagers or farmers are fortunate enough to have any savings at all, it’s often in the form of physical assets, such as cattle. These assets are difficult to liquidate in emergencies, and hoarding cash makes people more vulnerable to inflation.

Xcapit, based in Argentina, is using blockchain’s decentralized ledger to provide an alternative platform that makes it easier (and less intimidating) for those who lack a bank account, credit, or financial fluency to save and invest. Any person is eligible and can open an account by simply downloading the app and activating the wallet. To start investing, the only thing they need is to have cryptocurrencies, which they transfer from another platform or buy through Xcapit’s app partners. After completing a screening process that consists of filling in personal information (which can be as basic as name and cell phone number), users choose how much money they would like to invest and at what risk level. They can learn about their investor profile while answering a test embedded in the app, and Xcapit has built different financial products that yield different returns. Users can see the performance of their investments on their app, and choose to redeem the money at any point. The money, even while it’s invested, is always in their wallet.

Blockchain allows Xcapit to provide a simple investment interface where users can rely on the security of the network to know their assets are safe, and benefit from a simpler and cheaper investment process. For the past two years, it had 3,590 users from Argentina, Mexico, Brazil, and Colombia with average investments of $1,500, and managed approximately 3.6 million in total. From January 2021 to October 19, its active strategies yielded up to 15.36 percent in Bitcoin units and up to 8.83 percent in dollars.

3. Credit. Imagine facing a true emergency—your home catches fire, your savings are depleted, and you have zero ability to borrow. Credit scores, which banks have traditionally used to determine credit eligibility and type, have a predominant role in economic growth. They enable families to buy homes and get consumer credit, give businesses access to capital, and help countries smooth consumption levels in times of crisis. But more than a third of the population has no credit history and therefore has no safety net in difficult times. The International Finance Corporation meanwhile estimates that almost half of micro, small, and medium enterprises in developing countries have an unmet credit gap of $5.2 trillion every year.

The blockchain project Grassroots Economics, also funded by UNICEF’s Innovation Fund, based in Kenya, aims to close the credit gap in low-income communities. It’s a powerful concept: In times of crisis, villagers might not have a line of credit or a stack of cash, but they do still have actual goods and services, such as crops or clothes or even the labor of a cook or schoolteacher. Grassroots Economics creates something called Community Inclusion Currencies, or CICs, that allows it to issue tokens backed by all of the actual goods and services in a specific community, such as the town’s water, food, or the work of carpenters or babysitters. Kenyan villagers can use the tokens to secure a line of credit, backed by their own resources, to use in emergencies.

The CICs allows people to monetize resources so that they can give or take credit without Kenyan shillings or a bank. Instead, based on historic trade, people can get up to 10 percent of their past annual revenue as credits for future production, allowing them to continue trading beyond their current liquidity. As users trade tokens via a feature phone, all transactions are recorded on a blockchain, maximizing the security that users have when transacting with each other. Similar to the banking system, people who build good credit can enable loans by the same community. In 2020, Grassroots Economics had 58,400 users performing almost half a million transactions using their token equivalent of $3 million. Over 95 percent of users redeemed their CICs.

4. Insurance. Insurance policies tend to require IDs, proof of financial solvency, and additional paperwork that can present a barrier to entry. And even for those who have insurance, when the catastrophe hits, who pays the damages and how much is never very clear.

While there are fewer blockchain projects tackling insurance than other categories of financial inclusion, the technology does offer potential. ETHERISC and ACRE Africa (supported by our partner, Ethereum Foundation), for example, partnered to build a decentralized insurance policy aimed at protecting small farmers in Africa. The application offers farmers weather index insurance that uses smart contracts (self-executing contracts on a blockchain) to trigger payouts when extreme weather situations affect their crops. These smart contracts act like a simple if-then formula; if it rains 5 inches within 24 hours in a given area, for example, the insured farmer immediately receives a payout according to the agreed contract for flood-related damages. The contracts are connected to real-time weather data on temperature, rainfall, wind speed, hours of sunshine, and even hurricanes and hail. The automated system improves the operations for the insurer company, and transparent and fair payouts protect the farmers in the event of a climate related risk.

Without the transparency and automation the blockchain application enables, farmers would need to prove the damage, a process that can be lengthy and potentially prevent them from quickly recovering from the casualty. To date, 17,000 Kenyan farmers have received this insurance and are benefitting from the agility of the system.

Five Lessons to Help Accelerate the Learning Curve

These projects are very much in motion, and they’re helping real people buy food for their children, deal with emergencies, and begin to use financial tools previously out of reach. But blockchain for social good, and specifically financial inclusion, is still in its inception. While its promise is no longer theoretical, it’s clear that we need additional players exploring, prototyping, investing, and supporting applications. Here are five lessons from our experience that we hope can help others accelerate the learning curve.

First, the impact of a blockchain solution depends foremost on user adoption, and end-users don’t care about blockchain. Rather, they care about access, benefits, and how easy the application is to use. Solutions need to be user-friendly and put the user at the center. The main advantage for Leaf users, for example, is the ability to make cross-border transfers at a lower cost, regardless of how it happens on the back end.

Second, local teams are important to success. A product that works in Silicon Valley may not work in rural Kenya, simply because of a connectivity issue. Relying on teams that understand the local context, local public policies, and local assets and challenges are important to the project’s fruition. Kotani Pay worked within the constraints of middle-range feature phones, as well as a lack of Internet connectivity and interoperability across different mobile providers. As Kenyan locals, team members not only understood the problem they wanted to solve, they experienced it.

Third, there are multiple blockchain platforms (the infrastructure on top of which developers build a blockchain), and the choice is important. These platforms can differ by size, security level, speed, transaction fees, and energy consumption, all of which affect user experience. Xcapit, for example, built a multichain wallet allowing its users to choose the platform they prefer.

Fourth, blockchain applications need to be flexible enough to adapt to the fluctuations and technology updates, especially because the technology’s infrastructure is developing at the same time. Grassroots Economics, for example, had to change the blockchain platform it used three times to bring down user fees. Each modification requires time and a working budget, and if startups don’t anticipate this, they can end up high and dry before they get the chance to prove the solution works.

Finally, smart contracts are an attractive feature, since they create efficiencies in traditional systems, but it’s important to prioritize outcome-based measurement to assess how. More often than not, social innovators measure impact by the number of people a solution reaches, but this is not enough to understand how those solutions improve lives, and in what ways they are different or better than their precursors.

For example, although the information that ETHERISC and ACRE Africa insure 17,000 users is important, we can get a clearer understanding of the value of the solution with data like how much faster insured farmers receive payouts and how many resources the insurance company saves by using the self-executing contracts. Evidence is instrumental to determining (or not) whether these innovations are worth supporting further.

The projects highlighted above are showing how blockchain, as a ledger of information, can enable multiple parties that don’t trust each other to agree on the flow of financial transactions and take advantage of greater financial inclusion. To move the industry forward, we need developers to make the blockchain infrastructure more efficient and environmentally conscious, governments to create the legislation that regulates and stabilizes) the market, entrepreneurs to both pilot blockchain solutions and share their results, and funders that can provide capital to promising applications. We owe it to the 31 percent of the world’s population to keep exploring solutions that provide equal access to opportunities. Even if blockchain is only part of the answer, it’s worth exploring further.

Read more stories by Cecilia Chapiro.