Climate change and poverty are among the most pressing issues of our day—and they are inextricably linked. As a poor country develops its economy, it tends to use more fossil fuels that emit more greenhouse gases. Yet, the poor are also those most affected by environmental degradation. Extreme weather destroys agricultural production, as well as the water resources and coastal ecosystems on which the poor rely for their survival. This translates into problems like food shortages in Sub-Saharan Africa, shifting rain patterns in South Asia, the loss of reefs and declining fish stocks in South East Asia, and the decimation of storm-vulnerable coastal communities and cities.

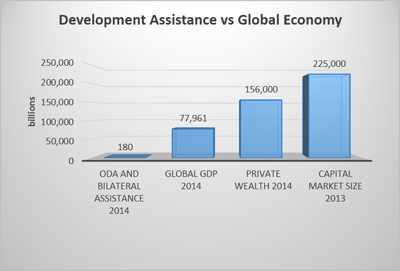

While extreme poverty may be on the decline at a global level, relative poverty is on the rise. Poverty alleviation programs haven’t delivered the hoped-for progress, and market-based approaches such as impact investing, microfinance, and crowdfunding don’t currently operate at sufficient scale. The Organization for Economic Cooperation and Development (OECD) estimates that official development assistance to developing nations peaked at $135.2 billion in 2013 and—together with bilateral grants—reached $180.3 billion in 2014.

Yet developing countries need trillions of dollars more to address these interrelated problems. At COP21, developed country governments committed an additional $100 billion a year for developing countries through 2020, and more thereafter. But that commitment isn’t binding, and it fundamentally understates the funding required.

Leveraging Private Capital

Private capital, if directed to these purposes, can fill the gap. The current size of global capital markets exceeds $225 trillion and global private wealth exceeds $156 trillion. Private capital's scale, global reach, and sheer power dwarf funding from governments, development institutions, and philanthropies that now invest in developing countries.

In addition, nothing else comes close to private capital's efficacy. According to the World Bank the private sector produces 90 percent of the jobs in the developing world. The challenge is to direct sufficient volumes of private capital toward poverty reduction, climate adaptation, and advancing sustainable economic development as reflected in the United Nation’s Sustainable Development Goals (SDGs).

Past as Prologue: The Clean Development Mechanism (CDM)

Until recently, the principal model for selecting and incentivizing private investment in development projects that mitigate greenhouse gas emissions while alleviating poverty was the Clean Development Mechanism (CDM), inaugurated by the Kyoto Protocol. The CDM employs a market-based system that issues saleable certified emission reduction (CER) credits—each equivalent to one ton of CO2—for qualifying projects that reduce or avoid CO2 emissions in developing countries. Industrialized countries can use the CERs to meet part of their emission reduction targets under the Kyoto Protocol. Although it has critics and is under revision following COP21, the CDM has supported more than 7,900 projects in 107 countries and issued more than 1.6 billion credits since its creation. A second financing mechanism beginning to take shape is the Green Climate Fund (GCF), which has a mission to invest in climate change adaptation and mitigation

A Special Purpose Digital Currency

Last year, the B20 Energy Forum, drawing on our earlier work on social credits, recommended that the G20 support "various incentives structures, such as a social credits mechanism to attract private capital for sustainable economic development." We believe implementing this recommendation could have enormous impact. To that end, we are expanding on our previous work on social credits and propose a new digital currency: sustainable development (SD) credits. This currency would serve as an additional incentive for private investment in projects that advance the SDGs, or greenhouse gas emission abatement and adaptation targets agreed on at COP21. Developing countries could use SD credits to stimulate the flow of private investment into infrastructure, renewable energy, clean water projects, health care access, elder care, public transportation and housing, agriculture, and education and training.

Establishing the Currency

Countries that launched the currency would enter into a binding international agreement with one another that would establish the terms and institutional arrangements for the currency. Unlike other digital currencies, such as Bitcoin, the agreement would create a multinational executive board (just as the CDM did) to issue the currency, select appropriate investments, and allocate the new currency to qualifying projects. SD credit transactions would be recorded in a public, distributed ledger based on blockchain technology, and the currency would exist only in accounts established by the distributed ledger to ensure security and transparency.

Although nothing identical to SD credits exists, some organizations have implemented similar technical features. For instance, the Bank of England recently experimented with and confirmed the viability of a similar digital currency. Switzerland's WIR—a complementary, non-digital special purpose currency—is also similar in some respects, and the United Nations Research Institute for Social Development continues to monitor and analyze a number of other alternate currencies.

Countries that establish SD credits would agree to recognize the currency as legal tender for payment of taxes and other public levies, making it a form of fiat money. It would meet many of the same criteria as the US dollar, Euro, and Yen, which aren’t based on a commodity, such as gold.

Companies and people would be able to use SD credits as they would other currency, as legal tender to buy goods and services, as well as pay public levies. The states establishing the currency would also endeavor to convince development finance institutions—particularly the World Bank and regional development banks—and developed countries to accept the currency for repayment of development loans. These features would enhance the official liquidity of developing countries.

Valuing the Currency

The value of fiat money typically derives from supply and demand for the currency, but we suggest that countries accepting the SD credits as legal tender consider assigning a “par” or exchange value that would establish the value of the credits when they are used as payment of public levies. One strategy would be to tie the currency to the value of the International Monetary Fund Special Drawing Right. The executive board would manage the record of issuance and credit value. The actual exchange value in the market, however, would differ depending on various factors, particularly supply and demand for the currency. We believe that the agreement by developing countries to accept the currency as legal tender would ensure its widespread acceptance.

Allocating the Currency

The executive board would establish the terms, conditions, and criteria for allocating the currency to qualifying projects, including the timing and utilization of the currency in a project. One of the most noteworthy features of CDM was the approval of appropriate projects through a designated national authority in each country. We recommend a similar arrangement for the selection and funding of projects to determine whether they would assist the host country in achieving its SDGs.

The board would allocate and grant SD credits to a project in sufficient volume to incentivize the required level of private investment for that project. The total value and timing of the grant would depend on the qualifying criteria, including those factors required to enhance private capital's return on investment, compensate perceived developing country investment risk, and underwrite additional costs that the project's social investment strategy may imply. The SD credits would be designed to encourage investment in risky, poor countries and reward investors who take the gamble. SD credits might be allocated to a project as a stand-alone incentive, or in tandem with support from a re-invigorated CDM or Green Climate Fund.

One role of the board would be to craft new types of facilities that establish the terms of the grant of the currency. A facility, unlike a loan, wouldn’t require repayment; it would allocate the currency draw-down timing and conditions over the life of the project, calibrating the level of flows for a particular project based on several factors—including the economic status of the developing country, the climate change impact of the project, and the extent to which the project is designed to address and meet the SDGs.

How SD Credits Could Work

Say an investor, a UK-resident business, decides to invest in the construction and operation of a chain of private hospitals and medical clinics in India. The executive board would review the project, and the Indian government—having assessed the needs of its people, and established priorities for the types, locations, and numbers of medical facilities it needs—would also review the project via its designated national authority.

The board—with support of the national authority, and based on criteria tied to poverty alleviation and climate mitigation—would establish an account of SD credits on which the project would draw. The project—subject to the conditions, timing, and structure of the grant facility—would use the currency to purchase goods or services or to pay public levies.

The SD credits could be donated, used in a bilateral exchange among private individuals, or used by an international investor, such as our UK-resident business. For the latter, which has a tax liability in the UK arising from the project, there’s an additional benefit: Using SD credits for payment of taxes in a developing country may also make that payment eligible for tax advantaged credit under an international tax treaty (there are more than 3,000 double taxation treaties globally) Thus, when the business used the currency to pay taxes in India, the payment, as with any currency, would be creditable against payment of UK taxes under the India-UK Double Taxation Convention. In essence, the UK government has agreed that taxes paid in India are taken into account and offset against a corresponding tax actually payable in the UK. The UK has similar double taxation treaties in place with about 120 other countries.

Conclusion

It’s time for a new and pragmatic approach that harnesses the most potent force we have at our hands at this time: private capital. Many investors in the global marketplace increasingly display interest in sustainable investments and openness to new investment strategies. Yet, poverty and climate change remain urgent global problems. Finding ways to channel the force of private capital to address these issues isn’t only the right thing to do, it’s the smart thing to do.

Read more stories by Jonathan D. Cahn & Ali Adnan Ibrahim.