In my role as senior vice president of innovation, strategy, and execution at the Housing Partnership Network (HPN), I am tasked with helping to ensure that the social enterprises we sponsor are effectively launched, managed, and monitored, using sound business principles. But when I started on the job about sixteen months ago, I found a curious thing: These social enterprises were reporting philanthropic grant dollars raised by HPN to fund them as “revenue” on their profit and loss statements. I looked further into this practice and found that it was fairly common across the nonprofit sector.

Because of this approach, many of the newer HPN-affiliated businesses appeared, based on their financial statements, to be profitable. That was accurate, in so much as their recognized revenues outpaced their expenses. However, to my mind, that view distorted these businesses’ financial fundamentals. If I characterized grant dollars as invested capital rather than revenue on the balance sheet, it became clear quickly that instead of being slightly profitable, some of these social enterprises were actually very unprofitable.

This finding wasn’t surprising, since these social enterprises were technically still in startup mode. Nonetheless, the observation piqued my interest, so I started looking at the financial reports of other, more well-established nonprofits and social enterprises throughout the United States. I found that this same reporting convention was more the rule than the exception.

The practice makes a certain amount of sense, since social enterprises are typically focused more on serving a social need and less on making a profit. However, from my experience working in startup environments, I believe that this kind of reporting can prove damaging if it’s the only way an organization looks at its finances. It’s fine to keep financial statements in this format for basic reporting or auditing purposes, but it’s also very important to understand how an enterprise is truly performing.

This is why for each social enterprise we sponsor at HPN, we now generate an alternative set of financials that recognizes grants as equity rather than as revenue. These grants are not truly equity, as the funders usually don’t seek a return on their financial investment other than the success of the stated mission. Nevertheless, this second classification scheme provides a more realistic view of the enterprise’s performance.

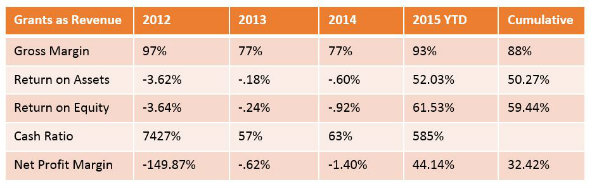

To illustrate the difference that this treatment of cash inflow reporting can make, consider the charts below, which show two different takes on a financial snapshot of one of the social enterprises that HPN supports. The first shows how financial ratios are represented when grants are treated as revenue. The second shows how treating grants as equity affects these ratios.

As shown, the financial ratios around return on assets, return on equity, and net profit margin change significantly when cash in-flows are categorized as equity. This new approach offers several advantages:

An Impetus to Improve Performance: Recasting the way cash inflows are reported forces leaders to focus on their organization’s profit and loss performance instead of on how much cash they have left in the bank to execute their plan. Focusing on what looks like a healthy cash position can foster a sense that there is plenty of time to build and execute on a business plan. And that false sense of security can stifle the urgency that would otherwise drive the organization to meet key milestone objectives. Reporting grant money as equity provides the impetus (in the form of a concrete metric) to improve performance and can push business leaders to focus on sales generation.

A Business-Focused Way to Prioritize Goals: When grants are booked as revenue, a manager can look at a profit and loss statement and say, “Hey, we’re doing great. We broke even this year.” On the first chart above, for instance, booking grants as revenue shows the enterprise breaking even in 2013. However, when those funds are placed on the balance sheet as an “equity” investment, instead, the profit margin deteriorates to negative 239 percent. The first set of figures is much easier on the eyes, but consider how those positive numbers might affect a leadership team’s perspective on priorities. Reporting grants as revenue, unfortunately, has the potential to compel business leaders to go and find more “grant revenue” instead of concentrating their efforts on generating real revenue.

A Funder-Friendly Emphasis on Sustainability: Grants are typically not designed to be available in perpetuity as a source of revenue. (If you find a funder with that orientation, please drop me a line!) Foundations and impact investors want to seed enterprises with just enough capital that they can become self-sustaining; they don’t want these fledgling businesses to return to the well each year expecting a new infusion. Funders will appreciate a social enterprise’s desire to become independent. They want (and need) to know you understand that they are supporting your incubation and startup phases and not supporting your business forever more. Armed with realistic financials, they may even be willing—and able—to help you move more purposefully toward self-sustainability, by offering additional support in the form of strategic development or process expertise.

A Path That Can Develop Stronger Managers: Reality is nuanced, but performance and results in business are driven by scorecards. Measuring metrics such as return on equity and net profit margin will drive a different result than focusing on how well a manager attracts grant revenue to his or her social enterprise. True innovation results from figuring out how to make a business model sustainable. As an added bonus, this approach can help business leaders become more accustomed to the stresses of running a business driven by numbers. Piling on the pressure? Sure, but how else does a piece of coal become a diamond?

For all of these reasons, I believe that all managers of social enterprises should endeavor, at a minimum, to generate a version of financial statements that casts grants as equity on their balance sheet. Doing so will force them to examine their profit and loss statements in an unvarnished way and motivate them to make business decisions focused on generating a successful double bottom line—a social return and a financial one.

Hold up the mirror at a slightly different angle. The results might surprise you.

Read more stories by Mark Lederhos.