The United States Social Impact Bond (SIB) sector has entered a phase of rapid growth. Four projects are on the ground, up to 20 are in active development, and interest continues to expand among diverse stakeholders. That makes this an opportune moment to pause and assess the strengths and weaknesses of the field, and identify where we need to build capacity to successfully establish SIBs as a viable financial tool.

In this article, we will use as our guide a set of assessments developed by The Bridgespan Group called a “strong field framework.” The framework involves five components: shared identity, standards of practice, knowledge base, leadership and grassroots support, and funding and supporting policy. In the case of the young SIB market, this process provides urgently needed input to strengthen the field going forward.

What Is “the Field"?

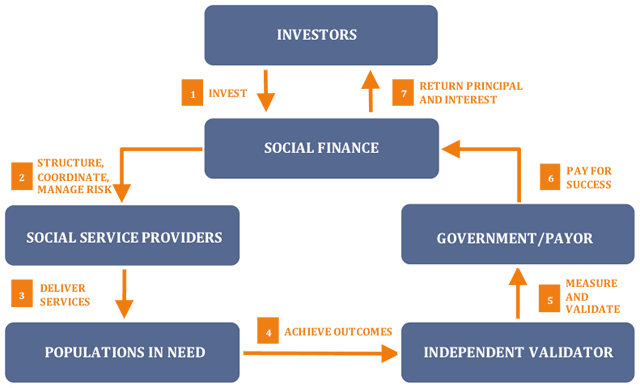

The stakeholders in the SIB sector—governments, financial institutions, foundations, individual investors, intermediaries, service providers, and potential beneficiaries—are many and varied. The ultimate objective of an SIB is to form an uncommon partnership among these stakeholders in pursuit of a common goal.

Stakeholders in the social impact bond partnership. (All images courtesy of Social Finance)

Stakeholders in the social impact bond partnership. (All images courtesy of Social Finance)

Shared Identity

For each aspect of the strong field framework, we will pose a series of questions meant to assess the SIB sector in this regard.

What are the issues that this field is trying to address?

- The chronic lack of sustainable growth capital for highly effective nonprofits. Among nonprofits surveyed by the Nonprofit Finance Fund, 56 percent reported that they were unable to meet demand for their services in 2013.

- The lack of government accountability and insufficient attention to funding what works. In a now-iconic call to action, two former officials in the administrations of Barack Obama (Peter Orszag) and George W. Bush (John Bridgeland) published an article in mid-2013 arguing that less than 1 percent of government spending “is backed by even the most basic evidence that the money is being spent wisely.”

- Pressure on government to provide safety net services at the bottom of the cliff, at the expense of upfront services designed to prevent people from falling off the cliff in the first place.

The weighting of these goals and emphasis on sub-goals varies widely, however. Some foundations are primarily interested in developing a more evidence-based public sector, for example, while other stakeholders are deeply committed to bringing new investor classes into the space.

What is the target population?

There is probably broad alignment around a very high-level response to this question: The target is underserved populations across a wide spectrum of issue areas. But there is debate around which target populations SIB projects would best serve. The next wave of SIBs will feature attempts to reach new and diverse beneficiaries, such as the homeless, preschool-age children, and low-income, first-time mothers. Some of these populations may present more compelling investable opportunities than others. The benefits of high-quality early childhood education, for example, have been widely demonstrated in empirical studies, but these benefits are difficult to quantify within an investor-friendly timeframe. Thus market participants hold varying opinions on whether to use SIBs to finance interventions that offer the most readily quantifiable, short-to-medium term benefits, or to serve those populations that are most in need.

What is the field’s desired outcome for the target population?

The broad response is likely improved life outcomes; stakeholders tend to agree that measuring outcomes rather than outputs is central to the SIB concept.

The exact definition of “outcomes,” however, is unclear and individual to each transaction. With regard to prison recidivism, is the number of formerly incarcerated individuals who do not return to prison a sufficient outcome? Do we also need to measure the number who find full-time employment? The overall benefit to society? Over what timeframe should we measure results?

Is there a common approach to the field?

Yes. The common approach is to develop and participate in innovative financial solutions such as SIBs to raise investment capital to fund high-performing nonprofit organizations. Stakeholders also agree, in concept, on the importance of basing investor returns on a solid evidence base drawn from rigorous evaluation and measurement techniques. While there is a broad common approach, however, there is not a standard instrument or template for the SIB.

Are field members clear about what the field is collectively trying to accomplish?

In fact, participants do not always agree on exactly what innovation they are championing; some focus on innovation in financing techniques, others on innovation in social services. Opinions vary about whether the market should use SIBs solely to finance expansion of proven programs or to experiment with new interventions as well.

Participants also disagree on the end goals of the SIB sector. Is it about bringing new money to tackle our thorniest problems, or sharpening the social sector’s focus on prevention, outcomes, and evidence? Will it become self-sustaining thanks to ongoing capital market participation, or will we hand over our work to the government?

How well do diverse and distinct organizations and individuals in the field collaborate?

In some cases, the field is characterized more by competition than collaboration. Within a given transaction, collaboration is not only normal, but also essential. Competition across transactions, however, is significant.

Nonprofit service providers are competing for scarce financial resources; financial institutions are competing for the small number of investor-ready transactions and committed impact investors; intermediaries compete for deal mandates from government commissioners. Indeed, government procurement processes tend to foster competition rather than collaboration.

Also, importing a financial model to achieve social value can lead to some issues in fostering collaboration among groups not used to working together on a transactional basis, such as financial institutions and nonprofit organizations. In part, this is a natural cultural divide between organizations and people who have very different aims, training, and pressures. Banks work at the fast pace of the capital markets, while government and nonprofits are accustomed to a more deliberate pace. Moreover, mutual trust may be in short supply: Government officials may not trust that investors will deliver funds for capital calls, while investors may not trust that future legislatures will appropriate funds for outcome payments.

Also, related to the competitiveness within the field, information-sharing among market participants is limited. State governments and financial institutions, in particular, are wary about sharing detailed information about transactions.

These difficulties reflect the inconvenient truth that the goals of these different stakeholders may diverge; bankers are seeking to shape a financial instrument that will attract impact investors, while governments aim to enhance taxpayer efficiency and service providers want to ensure fidelity to their model.

Standards of Practice

Are there codified approaches and standards of practice in the field?

As noted above, common approaches and practices are still very far from “codified” in the SIB sector. To some extent, the lack of codified standards is acceptable, perhaps even desirable, at this point in time. There is a distinct danger of standardizing too early, before we have determined exactly what constitutes “best practices” in this field.

For example, it is not yet clear whether randomized controlled trials (RCTs) should be considered “best practice” for all SIB transactions. Market participants also differ strenuously on the value and desirability of credit enhancements in SIB projects, as well as the level of performance measurement and management attached to each deal. Moreover, questions remain about which investors SIBs should attract. How big a role non-philanthropic impact investors should play versus foundations? Is there or will there ever be a role for finance-first investors (those investors seeking a competitive, risk-adjusted market rate of return)? As a corollary to this, what rate of return is appropriate?

There are no widely accepted answers to these questions yet, which suggests that the field has a long way to go before it develops standards of practice.

Are there exemplary models and resources available?

The short answer is no. The first SIB project worldwide was launched in 2010 in Peterborough, UK; official results will not be available until this summer (though some interim takeaways are available), and no other project has been on the ground long enough to provide useful feedback.

This means that we do not yet know what “exemplary” looks like. Was Peterborough exemplary? Frankly, the answer is also probably no; as the first-ever SIB project, Peterborough will undoubtedly offer many opportunities for improvement. The same is probably true of other early-stage projects now unfolding.

An ex-prisoner confers with counselor in Peterborough prison project.

An ex-prisoner confers with counselor in Peterborough prison project.

Informational resources on SIBs are available from a number of organizations that have explored the SIB field, ranging from the UK Cabinet Office to McKinsey, RAND, the Nonprofit Finance Fund, and the Center for American Progress. These resources are an excellent source of “SIB 101” knowledge, but—with the exception of the UK Cabinet Office—offer less information on the detailed mechanics of structuring a transaction.

How well developed is the research and knowledge base?

The knowledge base is weak but poised to improve rapidly in the next 5-7 years. Results from the up to 100 projects in the global pipeline will greatly enhance our knowledge about what works and what doesn’t work in the SIB sector.

Leadership, Policy, and Support

Are there influential leaders and exemplary organizations working to advance the field?

Yes, absolutely. Philanthropic organizations such as the Rockefeller Foundation and Laura and John Arnold Foundation are working to advance the field in important ways.

There is also significant conceptual support at the federal level for projects based on pay-for-success (PFS). Congressmen Todd Young (R-IN), John Delaney (D-MD), and a bipartisan group of co-sponsors recently introduced the Social Impact Bond Act, the country's first federal-level SIB legislation. The $300 million legislation would direct federal funds to SIB feasibility studies, evaluations, and outcomes payments on contracts executed with state and local governments. In addition, the White House hosted an impact investing roundtable in June where private-sector participants announced more than 20 new commitments totaling more than $1.5 billion; several focused on PFS.

New federal financial support for PFS has also become available. In June, the federal Corporation for National and Community Service (CNCS) announced the launch of an $11.2 million Social Innovation Fund PFS grant competition. The effort will support the development of additional PFS projects by supporting technical assistance to state and local governments.

The biggest gap in this field is the absence of one widely respected affinity group or association to bear some of the burden of information sharing, education, and market development. Several pioneers in the field, including the Nonprofit Finance Fund and Harvard SIB Lab—as well as Social Finance US and Third Sector Capital Partners in the role of intermediaries—have done important work to help build a market ecosystem. These pioneers bear heavy first-mover costs, however, and have limited ability to support the entire field.

Is there a broad base of support from the main constituencies?

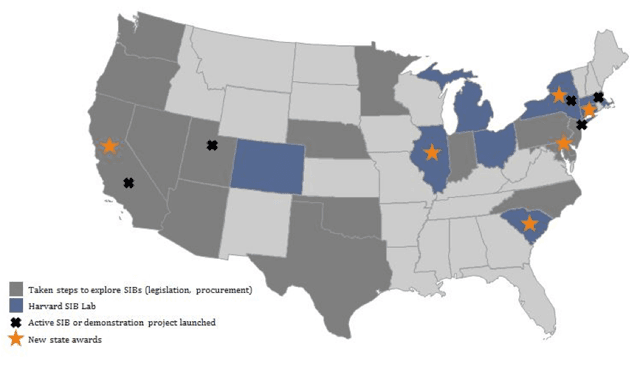

SIB activity in the United States, June 2014.

SIB activity in the United States, June 2014.

The SIB concept generally enjoys bipartisan support: Conservatives embrace its focus on government efficiency, while progressives laud its ability to serve more at-risk individuals. This support, however, has not generally translated into actionable policy. Most states lag far behind in developing a legislative framework to facilitate SIBs. Also, some governments at the state and local levels are wary of the optics of SIB deals; they may face criticism for using taxpayer money to repay wealthy investors. In addition, launching an SIB is time-consuming and complex for governments at this early stage.

In the foundation world, as noted above, some large and influential organizations have taken the lead in helping to get the SIB market off the ground. Moving forward, however, the willingness of foundations to participate in SIB transactions through program-related investments (PRIs) will be critical. Very few foundations—only a few hundred out of the many thousands of operating in the United States today—make PRIs, however. The will and ability of foundations to expand their PRI operations and use these funds to invest in SIBs may be a vital element for the establishment of a vibrant, self-sustaining SIB market.

Another class of investors, high-net-worth investors, report that they want their financial investments to align with their social and financial values, and that they are willing to accept higher risks and/or lower returns in pursuit of this goal. Indeed, the New York State Social Impact Partnership, launched by Social Finance at the end of 2013, was the first SIB ever to be distributed through the the wealth management platform of a major financial institution (Bank of America Merrill Lynch), and drew in over 40 investors. It is not yet clear, however, that expressions of support for the principle of double-bottom-line investing will translate into substantial and sustained flows of capital to SIBs.

Is the field supported by an enabling policy environment that supports and encourages model practices?

As noted above, the policy environment is generally supportive of the PFS concept, but efforts could be deepened to foster the market’s growth. Particularly at the federal level, the lack of a holistic set of supportive policies for impact investors is potentially constraining. Clarifying IRS guidance on foundation mission investments—including the standards for assessing production of income on PRIs—may catalyze further philanthropic participation in SIBs. Other policies, such as banks’ ability to invest Community Reinvestment Act (CRA) funds in SIBs and favorable tax regulations for investors, may add further support.

Recommendations

This process has revealed a number of areas in which the SIB sector does not correspond well to the strong field framework. Some of these shortcomings are probably less critical than others; e.g. some simply reflect the newness and youth of the market (for instance, the lack of cohesion around best practices). Others, however, risk emerging as real obstacles to the development of a strong field, and we should address them; the field needs investment, energy, and support to succeed at this juncture, including:

- Supportive public policy. The public sector needs to expand active support. At the state and local levels, government should move from a procurement mindset to an impact commissioning mindset—focused on measuring outcomes rather than counting heads. The passage of enabling legislation to allay appropriations risk is critical. At the federal level, the government should embrace supportive impact investing policies, as well as a commitment to using the bully pulpit of the Executive branch.

- Shared identity and standards of practice. The SIB sector urgently needs an industry-wide affinity group to complement the work of early supporters like the Nonprofit Finance Fund in developing collaborative rather than competitive norms, coordinating information-sharing, and educating stakeholders.

- Sustainable leadership and support. Foundations may choose to transition their support for the SIB sector from grants and credit enhancements toward investments. Capacity-building within foundations to overcome the obstacles to vibrant PRI programs, therefore, is essential.

Toward a Strong SIB Field

This assessment demonstrates that the United States SIB sector still lacks vital elements of a strong field; if we do not address these gaps, they could undermine the evolution of the field towards sustainability and maturity.

Most of all, it tells us that SIB market participants should be intentional and thoughtful about not just launching individual SIB transactions, but also about collaborating to foster a strong field that will ultimately benefit our most vulnerable citizens.

This article, based on our own observations and experiences in the SIB market, is intended as a first step in that direction. To advance this process in the months ahead, Social Finance will undertake to test our hypotheses through a broad data collection effort from the field, with the ultimate goal of developing a strategic road map to the strong field framework that will form the backbone of a robust PFS sector.

Stay tuned!

Read more stories by Tracy Palandjian & Jane Hughes.