For the past few decades, global health has been the poster child for development aid. Images abound of young African children receiving a vaccine droplet from a Western doctor, aid workers distributing malaria nets in remote villages, and—most recently and poignantly—medical workers covered head to toe in yellow protective suits treating Ebola patients. These images, and the aid they represent, are not inaccurate—donors spent $31.3 billion on global health in 2013, five times the amount spent in 1990—but they are incomplete.

Commonly missing are stories from the countries receiving this aid that represent the robust private health marketplace that is rapidly growing, and increasingly playing a critical role in financing and providing health services to low- and middle-income consumers. This is the part of the picture we wanted to understand in greater depth and detail when we conducted our analysis of the opportunity for global health impact investing (actual investing, not donations) in East Africa and India at the end of 2014. We wanted to hear from investors active in the field to understand why they chose to invest in health, how their approach to the sector has evolved, what level of intermediation and infrastructure exists for scalable capital deployment, and what trends they were seeing that present opportunities or challenges (or both) for future investment.

In our conversations with more than 30 active impact-oriented investors, we heard numerous mentions of the promise, growth, and maturity of the private health market in these regions, mostly due to friendly converging trends: a growing middle class, widespread access to technology and information sharing, active participation of multi-national corporations, increased mobility and urbanization, and the recognition that governments can’t do it all (nor should they—in the United States, the country that spends the most government money on health care, only 35 percent of health spending is public, the remaining 65 percent is private). These trends, paired with sustained double-digit private sector health care growth, paint a pretty rosy picture.

But as the private sector expands to complement—and in some cases compete with— public sector efforts, there have been significant growing pains, particularly among funders and impact investors. Donors and aid agencies increasingly embrace new, market-driven solutions to health problems, but have not made sufficient changes to how they deploy funding to adapt to the needs of the enterprises and organizations they want to support. Similarly, impact investors seek market or near-market returns, but have not adequately accepted that in most cases they cannot accomplish their goals by solely serving the “highest impact” bottom-of-the-pyramid (BOP) populations.

The result—for funders and the enterprises seeking their funding—is a bit of a mess. Growing pools of capital across asset classes are seeking to support private sector health solutions while enterprises are searching for money to seed, grow, and scale their businesses. But the two are often misaligned. To be clear, this is not to unique to the health sector. In fact, much of what we heard during our interviews is similar to already documented sentiments shared across the fast-growing but relatively nascent impact investing industry, as explained in reports such as Omidyar’s “Priming the Pump,” and the World Economic Forum’s “From the Margins to the Mainstream.”

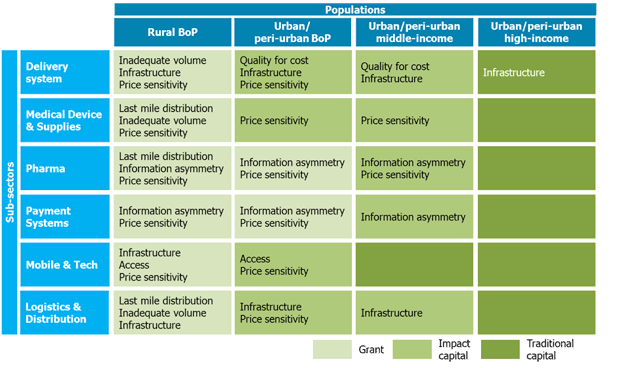

In an attempt to make some sense of the marketplace, and better understand where and when impact investors can enable by channeling more useful capital into global health, we developed a framework that characterizes the most “investable” sub-sectors within health and the needs of individual enterprises at different stages of their development (see below). This framework is intended to serve as a resource for investors interested in global health and help them identify the right type of capital for enterprises with different risk profiles across the health sector before they start to invest, because, as we learned from the case studies in our report, sometimes the wrong money is worse than no money at all.

Market Context & Capital Characteristics

(Image by Beth Bafford and Sarah Gelfand, from “Opportunities and Challenges for Global Health Impact Investors in India and East Africa”)

(Image by Beth Bafford and Sarah Gelfand, from “Opportunities and Challenges for Global Health Impact Investors in India and East Africa”)

To assess certain investable opportunities in global health, we suggest that investors take a few initial steps:

- Identify the market failures at the intersection of specific sub-sectors, and target consumer populations to understand the inherent challenges in the ecosystem. For example, most health care delivery enterprises exclusively targeting rural BOP populations (the cell in the upper-leftmost corner of the grid) contend with low patient loads, high distribution costs, and patients’ limited ability to pay.

- Understand how adept the entrepreneurs are at building a business model that addresses and solves for these hurdles, and see where they are in their stage of development.

- Lastly, once you understand the true needs, determine the characteristics (timing, flexibility, and structure) and type of capital (equity, debt, and hybrid) that will catalyze future maturation and growth.

In short, start with an understanding of the context and needs, and make sure the capital fits the business instead of bringing inflexible capital to the market expecting the enterprises to do the bending. If impact investors can jointly take this approach, we will have an extraordinary opportunity to strengthen enterprises that, despite the challenges they face, can sustainably save and improve the quality of lives for millions.

Read more stories by Beth Bafford & Sarah Gelfand.