Mission-related investments (MRIs)—those that generate a financial return as well as seek to generate social and/or environmental benefits—have attracted several types of investors. Socially responsible investments (SRIs), environmental, social, and governance (ESGs), and impact investments are the most common approaches to making MRIs.

It’s no secret, however, that assessing these dual-objective investments can be profoundly challenging. While metrics for measuring the financial performance of an investment strategy are universally clear, metrics for measuring social or environmental impact are not so well established. There are several imperfect options available for measuring social or environmental impact, but assessing the degree to which an investment strategy can achieve both typically leads to more questions than answers, including what attributes make an investment strategy an MRI? Is a trade-off between social/environmental impact and financial return necessary when pursuing MRIs? And how should an investor evaluate the ability of an MRI strategy to achieve both social/environmental impact and a financial return?

Thus, judging the efficacy of a mission-related investment strategy is an inherently subjective task, and can lead to “superficial” investment decisions that appear to balance both financial and social impact returns but on closer examination do not. However, a framework can provide for a more rigorous approach and help investors make more-informed decisions when evaluating MRI strategies.

The P4 Assessment Framework

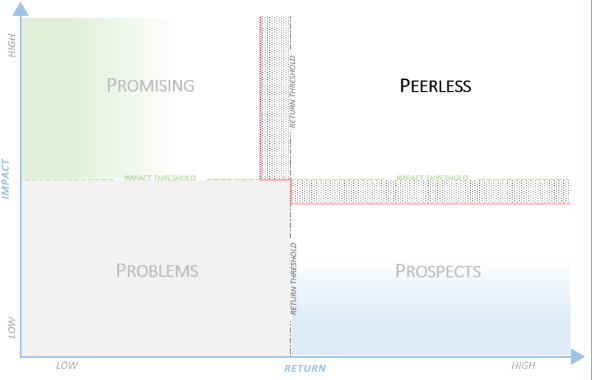

My colleagues and I at Colonial Consulting have developed the P4 Assessment Framework, a tool designed to better assess and categorize the ability of an MRI strategy to achieve an investor’s desired level of both social or environmental impact and financial return. The framework below categorizes MRI strategies into four quadrants according to their level of impact and financial return, with impact on the y-axis and financial return on the x-axis.

A framework for examining the impact and return of MRIs. (Chart by Andrew Siwo, Colonial Consulting)

A framework for examining the impact and return of MRIs. (Chart by Andrew Siwo, Colonial Consulting)

Here is a breakdown of the four quadrants:

- Peerless investment opportunities are those that generate high financial returns relative to their asset class and also achieve high impact. Impact investments and ESG strategies classified as “peerless” are expected to produce reports and track metrics relevant to their investment strategy. The types of returns achieved by peerless investment strategies prove that a trade-off is not inherent to MRI investments. To quote Michael Whelchel, co-founder of the boutique impact investment bank Big Path Capital, “Investors [who] are unfamiliar with the range of return outcomes across MRIs often mistakenly believe that an impact and return ‘trade-off’ is inherent.” Peerless opportunities perform in line with or outperform a target financial benchmark, however these types of investment strategies are hardest to find.

- Promising investment opportunities generate low financial returns relative to their asset class and achieve high impact. Promising investment strategies produce impact reports and track metrics relevant to their investment strategy. These investment strategies struggle to achieve high financial returns. They may perform in line with a target financial benchmark but generally underperform.

- Prospects are investment opportunities that generate high financial returns relative to their asset class and achieve low impact. While these investment opportunities achieve high financial returns, they struggle to achieve a significant social or environmental impact. Though their financial performance may be in line with or exceed a target financial benchmark, these strategies may also lack a convincing ESG or impact strategy.

- Problems are investment opportunities that generate low financial returns relative to their asset class and achieve low impact. These strategies can perform in line with a target financial benchmark, but generally underperform. Problem investment opportunities tend to lack a convincing ESG or impact strategy that equates to the type of impact that some investors desire.

Separating the Haves and the Have-Nots

The growing interest in various MRIs has led to a proliferation of products and has prompted firms to launch new ESG strategies or shape existing strategies into appearing MRI-focused. When examined as an MRI, some strategies are unable to withstand scrutiny. In some instances, managers with self-proclaimed MRI strategies do not evince the bona fides expected of this style of investing. Take, hypothetically, an MRI strategy called Healthcare Impact Fund that invests in private health companies. If the manager does not produce impact reports, does not intend to improve healthcare, or does not track relevant health-related metrics, its claim of being an impact investment strategy is untenable. (This is frequently referred to as “impact washing.”)

Despite the achievements of MRIs, they are unlikely to replace the role of relief work and are arguably less effective at addressing problems that require a humanitarian solution, such as natural disasters. It is conceivable that, in some instances, intentionally structuring a program-related investment (PRI) could be a more appropriate use of capital when the pursuit of a market-rate investment solution is determined to be an inferior option. In the words of Roy Swan, director of mission investments at Ford Foundation, “While some qualifying PRIs may deliver financial returns in excess of expected market returns, PRIs also have a greater tolerance for higher volatility around expected returns, which allows a PRI investor to accept a greater risk premium discount to be catalytic.” In other words, a PRI investment in an investment manager with a real estate strategy designed to preserve affordable housing through an opportunistic strategy (acquiring properties that need significant rehabilitation and perceived to be riskiest) may tolerate a return that deviates from the market expectation for such risk to accomplish a charitable purpose. An MRI investment, by contrast, would not.

There are few barriers to launching an MRI strategy and wide latitude concerning how managers market their investment products to warrant an MRI label. Of course, not all managers will deliver on their impact and financial return promises. As investors become increasingly active in adding MRIs to their portfolios, there will be more opportunities for them to align their assets with their values. The United Nations’ Sustainable Development Goals (SDGs) offer a useful reference for identifying challenges that investors and investment managers might address. And investment consultants and advisors can help evaluate the merits of an investment strategy and analyze the appropriateness of each opportunity for their clients’ investment portfolios.

As part of due diligence in assessing a strategy, investors should evaluate factors that include an investment manager’s philosophy, investment process, track record, competitive edge, and performance incentives. Performance incentives are helpful in determining the alignment of interests between the investor and investment manager. Since management fees are determined by asset size, investment managers can be undisciplined with respect to fund size. Managers who limit the amount of capital investors can commit are generally better aligned with investors than those who have an unlimited capital target.

Limitations of the P4 Framework

The “high/low” threshold on both axes in the P4 framework illustrates that impact and return can vary for each investor, as well as each MRI product. As a result, the framework can be overly simplistic in that it distills return and impact into binary categories. It also does not precisely define what high or low means.

The red line in the framework reminds us that MRI products do not always fit neatly within the quadrants. Some investment opportunities classified as promising or prospects are on the fringe, falling just short of becoming peerless. In cases where there is a stronger interest in achieving either impact or specific financial returns, investors may need to conduct additional analysis to determine the degree to which an MRI strategy aligns with their goals.

The ability to assess an MRI strategy has often eluded institutional investors due to a lack of tools to effectively measure the simultaneous achievement of social or environmental impact and financial return. The P4 Framework can be a convenient guide to plot, compare, and select MRI managers based on an investor’s impact and return goals.

Read more stories by Andrew Siwo.