Social impact bonds (SIBs) hold extraordinary potential. They represent a more effective way to distribute grant dollars, catalyze investment in the nonprofit sector, unlock impact data, and foster greater transparency and accountability. For a nonprofit sector that to date has been shackled with an opaque and inefficient capital market, any of these benefits would be transformative.

The underlying pay-for-success concept alone is groundbreaking. It brings together donors, impact investors, and nonprofit organizations to fund impact in a completely new, performance-driven way. SIBs provide investors an opportunity to fund a nonprofit organization’s work and earn a financial return based on impact. This allows donors to make performance-based donations that explicitly link capital with impact. Equally importantly, it puts nonprofits in the driver’s seat, giving them control over how much money they need to raise over specific time periods in order to achieve their goals.

But there’s a problem. Despite their potential, SIBs have failed to gain meaningful traction. In the United States, for example, approximately 12 SIB deals have been launched since 2012, raising only about $140 million in initial private investment, which is less than 0.01 percent of the $1.7 trillion in total annual nonprofit revenue and contributions.

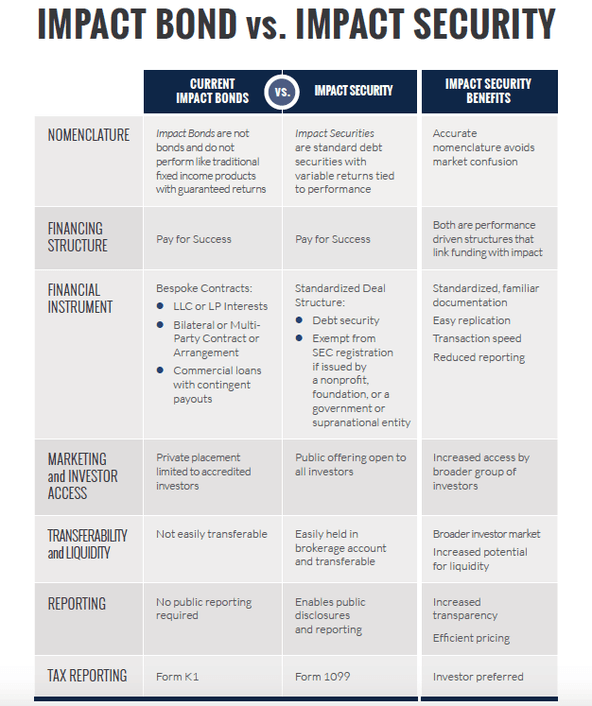

Why is that the case? One major reason is that calling these arrangements “bonds” is misleading. None of the SIBs put in play so far—nor many of their cousins, the development impact bonds, environmental impact bonds, and so on—has actually been a bond. Some people familiar with the field are willing to acknowledge that issue, accept it, and move on. But they are in the minority. Would-be investors who are not intimately acquainted with the nuances of SIBs—and this includes most would-be investors—may not know that the investments are not bonds. And so for most, calling a SIB a “bond” becomes a stumbling block that requires explanation, detracting from the positive and innovative aspects of pay-for-performance instruments.

For example, contrary to what reasonable would-be investors might expect, SIBs do not perform the way traditional bonds do. The term “bond” generally signals a relatively safe, fixed-income product with principal protection and specified returns. In contrast, SIBs are more equity-like. They provide variable returns tied to impact and often do not offer principal protection.

What’s more, SIBs are not legally structured as bonds. So far, most SIBs have been multi-party contracts, LLC or LLP interests, or commercial loans with contingent payouts. They are not securities, and the ramifications of that fact are significant. Privately negotiated, customized arrangements are not amenable to standardization, transparency, or liquidity, which curbs their potential to scale.

As Stephen Foley wrote in the Financial Times, “Social impact bonds need help to fulfill their potential: if the nascent investment vehicle is to become a big asset class, it needs a new name among other things.”

Problems Beyond the Name

Beyond the misnomer, a few other problems with SIBs are worth addressing. As it stands, the underlying structure of pay-for-success financing limits its potential. A recent Social Finance report about SIBs cites standardization as important to achieving scale, and it’s right: these instruments can’t truly transform the market if they aren’t standardized.

In addition, SIBs are not widely accessible to a broad range of investors. Interests in these customized instruments have been offered only as private placements limited to accredited and institutional investors, and they are considered “restricted securities,” which means they are not easily transferable.

Finally, since SIBs aren’t subject to public reporting requirements, data on their impact is inconsistently reported.

A Better Approach

These issues raise several questions: What if we could tweak the formula? What if an impact bond was actually a debt security—a financial instrument similar in legal structure to a corporate bond or municipal bond that can be bought or sold between various parties and has basic standardized terms such as obligations to make payments to investors upon the occurrence of certain events? In other words, what if we combined the pay-for-success model with an established, scalable, and tradable capital markets structure, and named it accordingly? And what if we called it an “impact security”?

This new structure would have five main benefits.

1. Credibility: Accurate nomenclature would promote the product’s integrity and build its credibility in investor circles. As mentioned above, attracting investor participation at scale requires accurate terminology.

2. Real scalability: A standard debt security would offer consistent, familiar documentation that allowed for easy replication and faster transaction speeds, resulting in a more scalable product.

3. Expanded investor access: If the debt security were issued by a nonprofit, a foundation, or a government or supranational entity, it would be exempt from SEC registration and available as a public offering open to all investors, accredited and non-accredited. This would expand the pool of eligible investors and could permit crowdfunding.

4. Transparency: A debt security model would facilitate public disclosures and reporting, which would lead to enhanced transparency and pricing that was more responsive to market data.

5. Liquidity: Debt securities could easily be held in brokerage accounts and be readily transferable. That would increase the potential for liquidity, which could broaden the investor market.

As everyone who has ever participated in an SIB knows, the hardest part of implementation is not the deal structure. It’s all of the other considerations: namely, impact assessment and practical challenges involved in working with the government. Adopting a standardized debt security model would simplify pay-for-success financing, help foster integrity, and promote broader participation in the emerging pay-for-success sector. With “impact securities,” we could transform the way billions of dollars are distributed, and in doing so, fulfill the full promise of this multi-trillion-dollar sector.

Read more stories by Lindsay Beck, Catarina Schwab & Anna Pinedo.