ESG investing strategies—investing plans that align with a healthy environment, social responsibility, and good governance—are some of the fastest-growing strategies in asset management.

According to a report from the US SIF Foundation, US institutional assets invested in ESG strategies reached $8.72 trillion in 2016, up 32.7 percent from 2014. ESG’s appeal isn’t limited to larger investors; ESG mutual funds are among the most talked-about consumer investment products on the market. Approximately $81 billion of environmentally friendly “green bonds” were issued last year, according to data from the Climate Bonds Initiative, providing institutional and retail investors a way to engage in ESG investing.

Yet many investment managers and their clients still have a narrow view of what ESG investing entails. This can limit their capacity to drive change and receive competitive investment returns. For some, ESG investing means only divestment: the wholesale exclusion of certain industries and companies from a portfolio based on set of ESG criteria (such as undesired consumer, labor, or environmental practices). Some investors may also assume that ESG investing necessitates accepting diminished returns. However, there are a number of serious flaws with this line of thinking.

First, divestment rarely impacts corporate behavior; instances of pure divestment driving change are hard to come by. ESG investors currently represent a small fraction of the investment marketplace, meaning there will always be other investors to replace them and reap the benefits. Recent academic research shows that "sin stocks” (such as tobacco, alcohol, and defense) continue to outperform comparable stocks even after controlling for well-known return predictors.

Divestment also means investors lose influence or ability to seek change via shareholder action. Worse still, by excluding entire sectors, divestment can reduce diversification, increase risk, and result in lower returns, as many investment experts are quick to point out.

But if divestment is often not a successful way to drive change, what is?

The answer is active engagement. The High Meadows Institute defines “active engagement” as action by a shareholder to influence or induce strategy/policy change in a given company. Shareholders usually do this through investment managers who act on their behalf to amend business practices. Research shows that when investors engage with companies on ESG issues that are material to an industry (such as apparel industry labor practices), both a company’s ESG and financial performance can make significant progress. For example, a 2012 Harvard Business School study found that successful engagements generated abnormal returns (the difference between actual and expected returns) of 7.1 percent for investors in the 18 months following the engagement.

A well-versed ESG investor should understand two approaches to engagement: private and activist.

Private engagement

Large institutional investors that wish to pursue a working, long-term relationship with a company usually pursue this approach, and engagement usually does not involve other investors or the public. Private engagements may involve petitioning a company to consider an ESG goal via emails, letters, phone calls, and meetings. Engagements of this nature have seen a dramatic rise: 64 percent of asset managers and 53 percent of asset owners reported increases in this type of engagement in a recent Conference Board poll.

The pros and cons of a private engagement stem from what one would expect: They happen in private. Keeping the discourse surrounding an ESG issue behind closed doors can allow the investor and investee to reach an agreement without concerning additional parties. However, a company may be unwilling to budge without pressure from additional shareholders.

Jem Hudson, vice president of the Boston-based asset manager Breckinridge Capital Advisors, emphasizes that a private engagement should establish a constructive dialogue between involved parties. In an interview, she states that the ideal ESG engagement will find “a sense of alignment in which Breckinridge and the company are on the same side.”

A testament to collaboration-over-confrontation, Hudson uses a questionnaire to promote conversation between her firm and the company targeted for private engagement. Via this process, Breckinridge aims to ascertain the quality of the target company’s ESG management and effectiveness, and the link between ESG efforts and financial results.

“The aim is to encourage companies to think carefully about what we are asking,” she said. “The team will then go through the questions during the engagement call, asking companies to elaborate on selected points.” With this information in hand, investors and companies can work toward a mutually beneficial solution. This dialogue-based approach, combined with regular follow-up, is an effective way to push ESG issues behind closed doors.

Activist engagement

However, reinforcing an agenda sometimes requires the added voting power or influence of other parties. In this case, opting for an activist engagement in tandem with other shareholders is the best way forward. Socially responsible investing (SRI) asset managers like Walden Asset Management have traditionally been the leaders of the method, but the approach is rapidly increasing in popularity as many of today’s largest asset managers and owners get on board. The recent proxy vote at the 2017 Exxon annual meeting was a notable example: An unprecedented 62.3 percent of shareholders voted to instruct the oil giant to report on the impact of global measures designed to keep climate change to less than 2 degrees centigrade.

Activist engagements offer a considerable risk-reward exchange. Finding other sympathetic shareholders is complicated by the need to work alongside multiple parties, making this route rather involved. Furthermore, shareholder resolutions are non-binding: A company’s management could meet a successful public engagement with indifference.

But for ESG goals of paramount importance, a well-coordinated public engagement may be the definitive strategy to enact meaningful change. Consider the below data from an EY study on public, activist engagements in 2015:

- 34 percent were environmental/social

- 32 percent were board-focused

- 18 percent were strategic/anti-takeover

- 15 percent were related to compensation

It is not a coincidence that ESG issues are the top of this list. Collaboration with other shareholders can be a decisive factor in ESG advocacy.

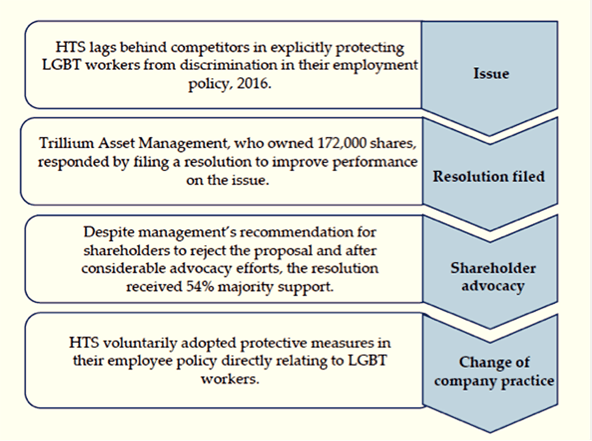

A notably successful use of this tactic came in April of 2016 when Boston-based, ESG-focused Trillium Asset Management engaged in an activist campaign against J.B. Hunt Transportation Services (HTS). HTS was in the minority as a Fortune 500 company that did not have explicit protections for LGBT employees in its policy. Given that the company’s drivers operated in many states with varying levels of legislative protection for those in the LGBT community, Trillium viewed HTS adopting these best practices as essential.

HTS’s board recommended that shareholders vote against the proposal, which it deemed “unnecessary.” Despite this, Trillium’s resolution passed, in large part due to thorough lobbying on its part. This infographic details the process by which Trillium engaged HTS and its shareholders to reach the desired outcome.

HTS lacked a policy explicitly protecting LGBT workers. Trillium Asset Management started a public engagement which resulted in HTS adopting such measures. (Image by High Meadows Institute)

HTS lacked a policy explicitly protecting LGBT workers. Trillium Asset Management started a public engagement which resulted in HTS adopting such measures. (Image by High Meadows Institute)

A private engagement would have been ineffective in this scenario. If HTS was unwilling to concede to Trillium’s suggestions in a public setting, there’s virtually no chance the company would have acquiesced without the added pressure. Here, Trillium effectively engaged fellow shareholders to protect the health of its investment: a difficult proposition without the support of fellow shareholders.

Private and public engagement strategies on ESG have their place and should be seen as complimentary, not as opposites. The public awareness and potential to swing the investor base garnered from a public engagement may not be worth the massive effort. Likewise, a company approached about an ESG issue by private means may not budge without shareholder pressure. What is clear, however, is that conversational and collaborative methods are effective tools in the ESG space. Engagement is the best way to ensure that ESG investors achieve they change they want, while generating competitive returns.

Read more stories by Chris Pinney.