Can Business Save the Earth?

Michael Lenox and Aaron Chatterji

200 pages, Stanford Business Books, 2018

We are at a crossroads. If we are to address climate change, let alone our broader sustainability challenges, we need significant disruptive innovation across a wide-number of sectors.

Will we be able to energize our innovation ecosystem to create the disruptive, sustainable technologies we need? Will we create the conditions under which sustainable innovations can flourish?

Our book is about how we may collectively catalyze business and markets to innovate sustainable technologies. We adopt a systems perspective, arguing that social sector leaders of all types—nonprofit leaders, policymakers, academics, business leaders, entrepreneurs—all play a role. There is no simply solution. Thus, this book is for everyone. We discuss how the innovation system works and provide specific suggestions on the levers available to each stakeholder to drive sustainable innovation.

Given the current political climate, it would be understandable to lose faith in our ability to address our sustainability challenges. We remain optimistic, however. Sustainable disruption is occurring across the economy even with the US federal government actively working to revive dying old technologies. Social sector leadership is critical to continue the path towards future technologies that drive economic growth, create jobs, and help secure a sustainable future. Working together, we can catalyze innovation in sustainable technologies. —Michael Lenox and Aaron Chatterji

The Innovation Imperative

Many scientists, policymakers, and business leaders argue that to address our sustainability challenges requires innovation on a massive scale. Simple calls to “cease and desist”—to stop engaging in activities that have negative environmental consequences—are neither realistic economically nor likely sufficient to drive us toward sustainability. Similarly, calls to simply reduce consumption, while sensible, are like the proverbial little Dutch boy holding back the floods by putting his finger in the dike. People will continue to demand products and services, and producers will provide them. Any reduction in per-person consumption needs to more than compensate for the increasing number of people in the world to reduce net impact. Absent wholesale changes in worldwide attitudes and consumption patterns, we need entirely new products, services, business models, and production processes that simultaneously create value to humans while minimizing, or even ameliorating, environmental impacts.

To illustrate this point, consider global climate change. An influential study by the Princeton Environmental Institute estimates that in order to keep carbon emissions flat over the next fifty years, we will need to trim our projected carbon output by roughly eight billion tons per year by 2060. The study’s authors identify fifteen strategies to achieve these reductions, from wind, solar, and nuclear energy to energy efficiency and carbon capture. Importantly, they observe that no one strategy is sufficient. The upshot is that we must simultaneously innovate across multiple technologies and adopt multiple approaches if we have any hope of meeting this goal.

Some argue that we already have the technology necessary to address our sustainable challenges. Renewable energy is gaining momentum and, as a result, is starting to compete with fossil fuels. According to the REN21 Global Status Report, renewable sources provided 19 percent of global energy output in 2014. Organic farming techniques demonstrate the viability of agriculture that does not overly rely on irrigation and fertilizers. Tesla and the introduction of electric vehicles by the likes of BMW and Nissan demonstrate that alternatives to gasoline-powered automobiles are viable. The technology exists, the argument goes; what we lack is the will to adopt.

We disagree. Technology cannot be considered in isolation from the broader socioeconomic system in which it is embedded. Innovation is not just invention—defined as the creation of something new. Innovation is the marriage of invention and commercialization. For an innovation to be viable, it must create value for individuals who are ultimately willing to subsidize the development, installation, and scaling of a new technology. Solar cells and wind turbines are wonderful technologies. Innovation has helped improve their efficiency and lower the cost of their manufacturing—as much as 200% in the case of solar cells from 2010 to 2015. This in turn has attracted investment and helped spread adoption. But it has not reached its potential or fully captured the hearts and minds of the public. What future can we predict for renewable energy if significant innovation in the use of fossil fuels keeps pace with renewable technologies? Consider July 11, 2008. The price of oil hit $147 per barrel. As many worried about the impact of high oil prices on economic growth; others quietly celebrated the creation of an opportunity. Now was the time for renewables—solar, wind, biomass—to significantly shift our energy portfolio. Investment in green technology surged. Numerous renewable energy start-ups emerged, and, in the United States alone, investments in green tech start-ups reached a high of more than $7 billion in 2008.

Fast forward five years. The price of oil dropped to $50 per barrel. Innovation in the energy sector has flourished—just not in the way that technology optimists had predicted. Advances in hydraulic fracking and horizontal drilling had lowered the costs of extracting oil and gas from regions previously left fallow. In the United States, an energy renaissance was under way. It was looking like the country would achieve energy independence by 2017. By January 2015, the price of gasoline in the United States was under $2 per gallon. The price of natural gas had plummeted to $3 per million Btus (British thermal units). Despite gains in solar technology, energy produced by natural gas power plants continued to be more cost effective. Projections released in the 2015 US Energy Information Administration (EIA) Annual Energy Outlook show the cost of electricity produced at a conventional combined-cycle natural gas plant ($/MWh [megawatt-hour])—put into service by 2020—will be on average 35 percent lower than that produced at a utility-scale solar photovoltaic (PV) installation (65 percent without tax credits). Venture capital investment has consistently dropped since 2008, down to $2 billion in the United States by 2014.

What went wrong (or right, depending on your perspective)? We argue that the success of an innovation is ultimately judged by the value it creates for some end user. Investment and adoption in renewable energy depend on a myriad of factors, including advancements in competing, mainstay technologies, specifically natural gas and oil. That brings us back to markets. Love them or hate them, markets are the way that most innovations express their value. As every entrepreneur knows, a new product or service is judged by the willingness of others to pay for her goods at a price that exceeds the entrepreneur’s cost to produce them. Thinking about it this way casts innovation in a different light. The innovation imperative is to drive up the efficiency and drive down the cost of renewable energy to compete with fossil fuels. This goal can be achieved by improving the underlying technology—such as PV cells—or by innovating around any number of complementary technologies such as energy storage solutions (batteries), electrical distribution (smart grid technology), or business models (financing for residential adopters of solar panels).

The same innovation imperative exists for numerous other “sustainable” technologies: energy-efficient computing and electronics, low- or no-emission vehicles, green buildings and supplies. We define sustainable technologies as those products, services, business models, and production processes that reduce the environmental impact of these goods relative to other existing technologies. A sustainable technology in and of itself does not guarantee sustainability; rather, it promises to reduce the unsustainability of existing technologies. By continuously innovating new sustainable technologies, however, we can reduce unsustainable practices such as natural resource depletion and environmental degradation and increase the prospects for future generations to flourish….

Our Argument

Value-laden pleas about what businesses should or could do cannot help us understand what they will do. Similarly, blind faith that markets will “figure things out” ignores the broader institutional context and the imperfections of markets. Economists are often cited for their advocacy of free markets, but they have also long pointed out the potential for market failures. Pollution is a classic example of one such failure, what is referred to as a negative externality—where individual efforts create a negative by-product that causes many to suffer. Many of our environmental resources are common pool resources—goods for which one individual’s consumption reduces the availability to others, while the collective finds it difficult to exclude individuals from the pool or users or reduce consumption. Fisheries and shared rivers are common examples.

Ultimately, the extent to which businesses will innovate disruptive, sustainable technologies is determined by a complex interplay between markets and various institutional actors: innovators who champion new sustainable technologies, investors who see market opportunities in these sustainable technologies, executives who steer large organizations toward profitable and sustainable opportunities, customers who are willing to pay for these sustainable technologies, activists who pressure businesses to invest in green innovation, and governments who incentivize new sustainable technologies through regulation, taxes, and other policy levers. Each of these players influences the degree to which businesses invest in and develop sustainable technologies.

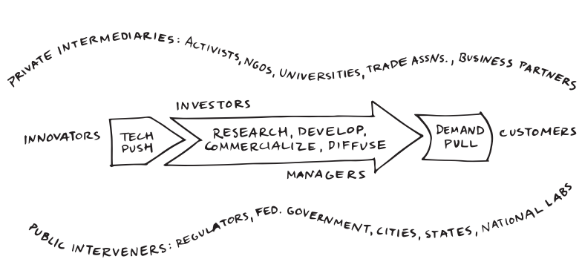

We propose a model of innovation as a system (see Figure 1). At the core is the process of innovation; the steps by which a concept is advanced into a viable product or service that disrupts existing markets or creates new markets. There are many ways of characterizing this process, but we suggest a simple four-step process from research to development to commercialization to scaling and diffusion. Each step is part of a critical path toward disruption. Not every concept will eventually scale and diffuse. In fact, most will not. The innovation process is as much a process by which concepts and technologies are winnowed with a few winners emerging in the end. Innovation is sometimes characterized as a funnel where thousands, if not millions, of ideas enter with only a handful exiting the funnel as disruptive technologies in the end.

Buffering the innovation process are two attractors: factors that help motivate action in the process. One attractor is the demand side of innovation. The demand side, or “demand pull,” refers to the market incentives to innovate created by the demand for goods and technology. In other words, demand pulls the technology through the innovation process. For example, consumers can create demand pull by desiring environmentally friendly products and services. Or government can create demand pull for sustainable goods through taxes or subsidies. Or other businesses can create demand pull by demanding improvements from their suppliers, perhaps to mitigate their own risks and to avoid the ire of environmental activists.

The second attractor is the supply side of innovation, or what is often referred to as “technology push.” Technology push refers to the support that is needed to drive innovation. What if innovation is not a simple Pavlovian response to a market stimulus but emerges from the genius of the innovator? This is the heart of the idea of technology push: scientists, engineers, and designers pushing the boundaries of technology and creating new goods and services that transform markets. Innovators require capital to invest in research and development and to help bring their products and services to market. Innovation arises out of a rich tapestry— what is often referred to as the innovation or entrepreneurial ecosystem. Technology push includes those resources that make up the innovation ecosystem that supports the innovation process.

Scholars have long debated the relative importance of technology push versus demand pull in driving innovation. Not surprisingly, the evidence suggests that both are critical. A broad blossoming of new technology incubators and venture funds directed to sustainable technologies will have limited impact if those technologies do not ultimately create value that is demanded in the marketplace. Similarly, the creation of market incentives—say, the creation of a carbon tax—will not lead to fundamental disruption unless there is an underlying support system to create the conditions under which innovation can flourish. Both technology push and demand pull are needed.

Surrounding our attractors are a broad set of public interveners and private intermediaries that impact the degree to which technology push and demand pull drive the innovation process. Markets are driven by a number of actors, including innovators, entrepreneurs, established businesses, suppliers, employees, investors, and consumers. Furthermore, markets do not operate in isolation. They are embedded in a broad sociopolitical system that enables and constrains their functioning. Thus, activists and NGOs, regulators and policy makers, lobbyists and legislators, global trade organizations and industry trade associations, universities and national laboratories all play a role. In concert, these market and non-market players create the conditions under which innovations either flourish or languish.