(Image courtesy of Propel)

(Image courtesy of Propel)

Jonerrah Small, a mother of two from Brooklyn, N.Y., was tired of calling the number on the back of her electronic benefits transfer (EBT) card to check her food stamp balance every time she went to the grocery store. She didn’t want to punch in a long string of numbers on an automatic service line while also trying to keep an eye on her two young kids. So in 2016, she started using FreshEBT, a mobile app that allows users to check their food stamps and benefits balances online. The app is free and available in all 50 states for anyone with an EBT card.

The New York City-based software company Propel, which created FreshEBT, is dedicated to building products for low-income Americans, whom the tech industry often overlooks. “People tend to solve the problems that they understand—and that’s why there are so many companies out there helping you do your laundry, or helping you to purchase lunch, but not a lot of companies out there solving the actual day-to-day challenge of, for example, single mothers on food stamps,” says Propel founder and CEO Jimmy Chen, a Stanford University alum who previously worked at LinkedIn and Facebook.

Dan Nemec, an advisor to Propel and executive director at JPMorgan Chase & Co., worked on early implementations of EBT in the 1990s and remembers the social stigma that people faced when they had to pay with paper-based food stamps or government checks. One of the challenges “unique to the industry segment that Propel is addressing, especially to an emerging technology-based firm, is the slow pace of change in government services,” he says. Only about 1 percent of the 22 million Americans on food stamps right now use FreshEBT. But Chen is optimistic. “We have access to populations that are traditionally preyed upon by all sorts of different financial services and products,” he says. “And we see FreshEBT as a really exciting opportunity to introduce higher quality ones that actually can help them improve their finances.”

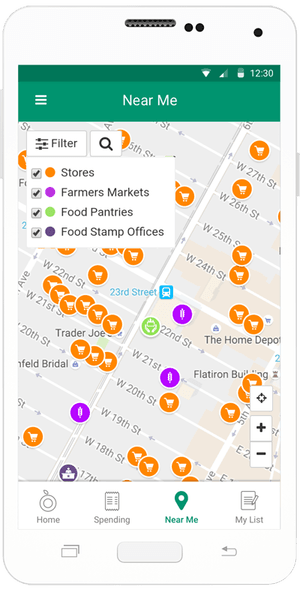

In addition to statement balance checks, FreshEBT offers visual aids—such as grocery lists and pie charts showing EBT transactions at different locations—and a location-based service that maps out nearby supermarkets, corner stores, and farmers’ markets that accept food stamps. The app’s grocery list allows users to enter a product’s name and price and then automatically updates the total balance.

“I like that it shows you the way you spent your money,” says Small, the mother of two. “I’m really good with budgeting. Usually, I take two, maybe three trips a month to get groceries. But this month, I went once—and I still have leftovers.”

The app offers a vital service for food stamp users, who have to pay the difference in cash if they overspend their EBT balance. But it’s also a great business opportunity for Propel, says Chen. People on EBT spend about $70 billion per year on groceries—11 percent of the American grocery industry’s $600 billion overall revenue. “We think that means that there’s a huge business upside in being able to advertise and promote things to this population,” Chen says. FreshEBT gains publicity and profits through partnerships with stores nationwide. And app users in certain participating stores also gain access to special deals and coupons, an offering that Propel plans to continue expanding.

The FreshEBT app also features a weekly recipe from Leanne Brown’s cookbook Good and Cheap, written for people living on a food stamp budget. “I love the little recipes in there,” says Small, who uses the app at her local Foodtown store. “Like for tilapia.” But she wishes there were more recipes for users who don’t have access to a full kitchen and cooking equipment, such as people who live in temporary housing. She also says that occasionally the app has bugs that affect her spending. “Sometimes, it will say that there’s still money in my balance,” she notes. “But there’s not—and I don’t know until I try to pay for something.”

Ryan Falvey is the managing director of the Financial Solutions Lab at the Center for Financial Services Innovation, which invests in both Propel and several financial service startups that don’t have a specific focus on social impact. He hopes that Propel can serve as a model for both technology companies (which are usually less interested in social impact) and government agencies (which are often slow to embrace change). “I think founders like Jimmy [Chen] need to be taken seriously by conventional commercial investors,” he says. “This is a product that has an obvious need, strong growth, and huge potential—both economically and from a social impact side.”

Read more stories by Noël Duan.