(Photo by iStock/Mumemories)

(Photo by iStock/Mumemories)

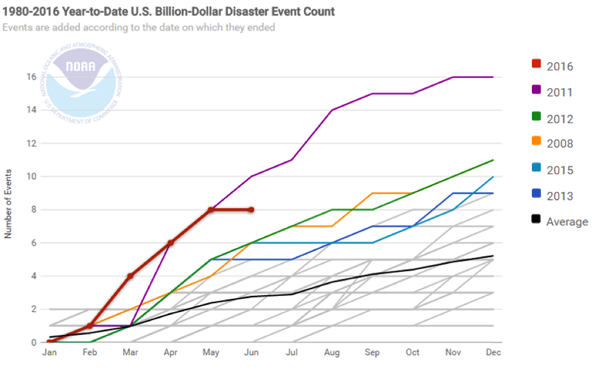

If you Google “cost + climate change,” you’ll get a range of estimates, all in the trillions. If you try searching for “how much private companies are investing in climate resilience,” you’ll get an even wider range of results. Meanwhile, Mother Nature is busy plotting the cost of inaction. The number of natural catastrophes worldwide—and the economic losses resulting from them, most of which aren’t insured—has increased significantly since the 1990s. During the previous 35 years, the average number of billion-dollar weather disasters in the United States was about five per year. In 2016, there were 15 weather and climate disaster events with losses exceeding $1 billion each in the United States alone.

Billion-dollar disaster events in the United States between 1980 and 2016. (Image courtesy of NOAA)

Billion-dollar disaster events in the United States between 1980 and 2016. (Image courtesy of NOAA)

Rising seas, more powerful storm surges, droughts, floods, and extreme heat all damage livelihoods, assets, and the economy—and they are expensive to fix. Investors and underwriters have taken notice and are increasingly demanding data on the climate risk of their assets. Last month, the world’s largest asset manager, BlackRock, listed climate risk as one of its top “engagement priorities.” Meanwhile, forward-thinking companies are keen to advance market reporting and disclosure mechanisms that will reward them for investing in assets and strategies that can weather a changing climate.

Building the X-ray vision investors require to see climate risk through the many layers of their holdings is hard work. In December 2016, the Task Force on Climate-Related Financial Disclosures (TCFD), an effort requested by the G20 Financial Stability Board Chair Mark Carney and led by Michael Bloomberg, issued a set of draft recommendations to serve as a prototype.

Though climate risk awareness began as a conversation about “divestment” and “stranded assets,” it has moved well beyond carbon emissions and fossil fuel exposure. As the concentration of greenhouse gases (GHGs) in the Earth’s atmosphere continues to rise, and as major and developing economies around the world begin to take steps to mitigate emissions, businesses and investors are confronting a suite of climate-related risks. TCFD frames these well as transition risks and physical risks.

Transition risks manifest as the global economy evolves toward a lower-carbon future. Transformational developments in technology, regulation, and markets will pose varying levels of financial and reputational risks for investors. Meanwhile, physical risks will result from severe weather events and longer-term shifts in climate patterns that cause direct damage to assets and can significantly disrupt supply chains.

Corporations are an important catalyst for scaling investment in climate resilience, which can encompass both climate mitigation and adaptation strategies. The most striking example can be found in the area of renewable energy procurement. A global initiative called RE100 represents a group of 88 companies—including Google— committed to 100 percent renewable energy, spurring meaningful market growth. According to the Business Renewables Center, corporate purchasing of wind and solar in the United States between 2010 and 2015 grew by more than 16 times, from less than 0.2 gigawatts (GW) to more than 3.2 GW. To put this surge of activity in context, the United States added 11.2 GW of utility-scale renewable generation capacity in 2015.

Google will reach its 100 percent renewable energy commitment in 2017 and is already the largest corporate purchaser of renewable energy in the world. In addition to this extensive mitigation work, Google has also been quietly building a robust climate resilience strategy. In doing so, it joins a group of major corporations that recognize the importance of incorporating climate risk into core business strategy.

For Google, the focus on resilience is born out of a culture of innovation—evolve or die—and commitment to long-term thinking. We began building a climate resilience strategy last year knowing that the well-being of our users/customers, shareholders, neighbors, and employees depends on their trust in the reliability and security of our infrastructure and products—and that the ability to thrive in a changing climate requires that we maintain the vitality of this relationship.

Climate change is real. We’re a global company, and our goal is to give everyone everywhere the tools and opportunities they need to play their own part in protecting the planet ... We get that this is a long-term project.—Google Environment Website

Our team decided to develop a set of Principles of Climate Resilience, much in the same way that Google’s founders developed the “Ten Things We Know to Be True” to guide the company’s decision-making as it grew. We started by looking at two frameworks. The first, San Francisco Estuary Institute’s Vision for a Resilient Silicon Valley Landscape, was sponsored by Google in 2015. Before its creation, there was no existing framework that addressed the unique ecological opportunities in Silicon Valley, where Google is growing its presence. The second framework was the Rockefeller Foundation’s City Resilience Index (CRI) which focuses on urban settings. While both of these frameworks speak to our values, neither directly applied to the broader climate resilience goals of Google, as a global organization with diverse business operations.

Ultimately, we convened a cross-functional team that represented three different parts of the business and arrived at the following principles, which will guide future decision-making on climate resilience:

- Setting and Context: The unique aspects of geographic location determine opportunities and constraints for addressing resilience.

- Scale: Resilience should be optimized at all scales (building, campus, district, region).

- Robust: Well-conceived, constructed, and managed systems improve climate resilience at different scales.

- Integrated: Linkages between distinct systems and infrastructure optimize outcomes for resilience.

- Redundant: Spare capacity promotes diversity and complexity, and accommodates disruption.

- Diverse and Complex: Richness and variety in the network of systems and infrastructure are critical for Google to thrive.

- People: The people who support, shape, and sustain Google are central to resilience strategy.

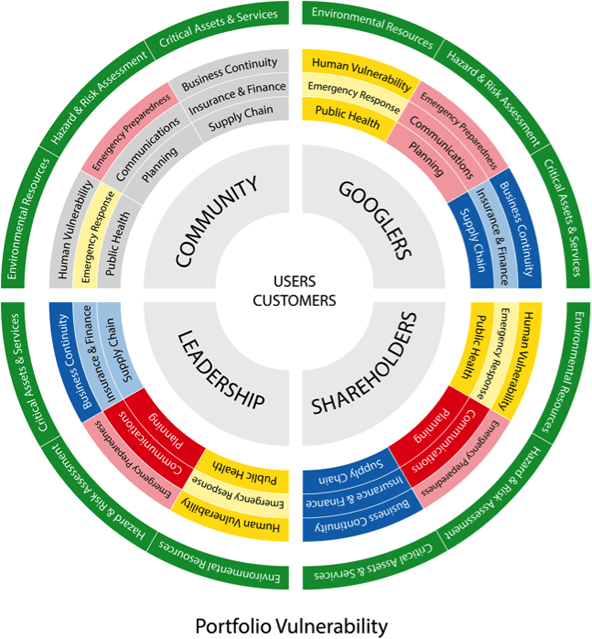

From there, we created a framework that prioritizes impacts to people (including communities, users, and Googlers) so that it represents the different aspects of climate resilience within Google, as well as the internal and external actors who either influence or are influenced by Google’s climate resilience decisions.

Google’s people-centered framework represents aspects of climate resilience within Google, and actors who either influence or are influenced by Google’s climate resilience decisions. (Image courtesy of Google)

Google’s people-centered framework represents aspects of climate resilience within Google, and actors who either influence or are influenced by Google’s climate resilience decisions. (Image courtesy of Google)

Equipped with these frameworks, Google is turning its attention to the question of how to connect climate resilience to the bottom line. More specifically, we are developing new tools to weigh the cost of inaction against the cost of investing in resilience.

Driven in part by the pivotal 2015 Risky Business report detailing the economic risks of climate change across specific business sectors and regions of the economy, leading companies in traditional sectors like agriculture, transportation, retail, and reinsurance have already begun to see dollar signs in climate resilience strategies. With relatively asset-light and resource-efficient business models, technology companies have to think more creatively about how they will thrive in a changing climate. And ultimately, for Google and others, investments in climate resilience must be tied to the financial health of the business.

According to the Federal Emergency Management Agency, $1 invested in building resilience and reducing exposure saves $4 in disaster recovery. Other research points to even greater pay-off: One study calculated that $1 in preparedness is worth $15 in disaster recovery efforts. While metrics like these exist for municipalities and government agencies, few tools and resources have been developed for private sector companies. As a result, corporations typically take a business-as-usual view of climate risk, which relies on short time horizons and strategies based on historical data rather than future projections.

Universities like Stanford can help catalyze corporate and investor response by filling important information gaps with accessible and actionable data. The Stanford Steyer-Taylor Center for Energy Policy and Finance is contributing to one such effort called the Asset-Level Data Initiative (ADI). Launched in partnership with the Sustainable Finance Program at the Smith School of Enterprise and Environment at Oxford University, CDP (formerly the Carbon Disclosure Project), 2D Investing Initiative, and the Stanford Global Projects Center, ADI’s mission is to make accurate, comparable, and comprehensive asset-level data tied to ownership publically available across important sectors and geographies. ADI is designed to act in coordination with existing organizations to drive use, improve access, and enhance the quality of asset-level data.

The time is ripe for companies to look beyond quarterly earnings and depreciation schedules, and into frameworks that are developed through public and private collaboration that quantify the benefit of corporate resilience. Particularly in the tech sector, such an effort will take leadership, coordination, and engagement.

In many ways, the Paris Agreement provides a roadmap. Companies must be able to run scenario analyses or put simply, they must ask, how does the business run with 2—or 3 or 4—degrees Celsius warming and along the various development paths to those outcomes? And what investments should they make now to withstand the transitional and physical risks of those scenarios? Google and others have begun to build the foundation for such an undertaking. Meanwhile, future generations are searching for the time in history when the current generation acted on resilience.

Read more stories by Kate Brandt, Kate Randolph & Alicia Seiger.