Much has been written about a perceived shortage of return-oriented capital available for impact investments. These articles (including the recent “Closing the Pioneer Gap”) generally lament that social returns pay lip service to financial expectations and that the risk appetite for investors is too limited to suit the “realities on the ground.” At the same time, the authors toe the line and recognize the benefit in supporting the need to apply market-based solutions for addressing poverty with the kind of scalable solutions that only business—and the capital structure it implies—can bring. The fact that these two positions are fundamentally contradictory is often lost in glossy arguments calling for blended returns, which can overweight difficult-to-measure social indices.

This does not have to be the case, and return-oriented impact investors need not reduce already low (relative to risk) financial expectations to promote increased social benefit in otherwise underserved markets. But they do need to be coaxed.

Thus, the key to bringing scalable solutions to underserved markets is not to beseech capital providers to unnaturally lower return expectations, but instead to help lower the risk profiles they rightly perceive as characteristic of informal markets. This places a high premium on fund managers and entrepreneurs who understand their respective markets and work to minimize the many types of business risks that young enterprises routinely face.

To broaden access to capital, first narrow the investment field.

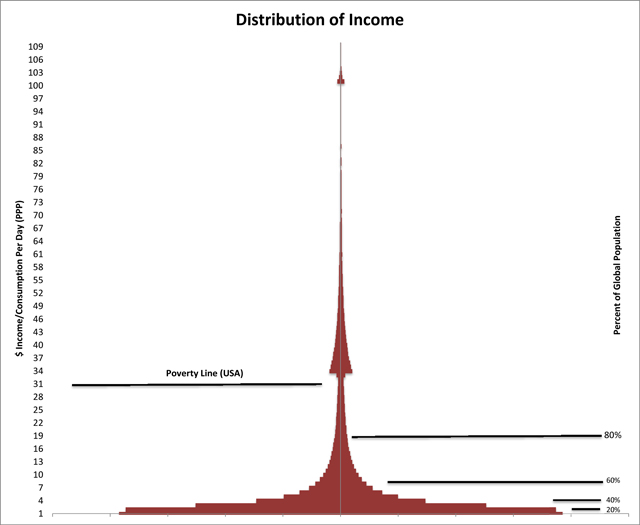

The wonderful thing about the impact investment space is that it is comfortable in any part of the so-called economic pyramid comprised of the roughly 7 billion people who inhabit the planet. The illustration below—created by a graduate student of mine, Abi Olivera—depicts this “pyramid”, and is based on household survey data from the World Bank (PPP adjusted). Let’s parse this pyramid, beginning at the bottom.

In an article published by the Harvard Business Review in 2011, “Segmenting the Bottom of the Pyramid,” the authors offer an important observation about the poorest 2.5 billion of the world’s population. At the very bottom, where 1 billion people live in extreme poverty (less than $1/day in purchasing power), there are no existing, practical functioning markets, and it’s not likely that there will be in the near future. Further up, the next 1.5 billion (up to about $3/day) are living and working with very informal markets at best. Lacking any real income, these two population segments—representing almost 40 percent of total world population—require massive assistance from governments and nonprofits for access to even the most basic services, including water, sanitation, and education.

Businesses that are capitalized to provide a return to shareholders cannot survive in these segments because—despite the “demand”—there is no way to bring “supply” without a massive intervention of subsidies. Here you need government, philanthropies, and NGOs doing the best they can to “push” services into desperate communities. This is important work, but it is also expensive, inherently unstable politically, and certainly not scalable economically. These efforts in aid and support may be humanitarian imperatives, but they cannot drive economic growth nor are they sufficient to help eradicate poverty. This is a useful distinction as far as it demarcates one boundary of the impact investing space, where there is virtually no constructive role for return-oriented capital unless it is heavily subsidized.

The upper boundary is less important to demarcate as return-oriented impact investing can play a role right up through the most developed economies where regional poverty levels are persistently difficult to eradicate. But for our argument, let’s draw a line under the top 20 percent of income earners (1.5 billion) who make on average more than $16/day (still below relative poverty lines in the United States). Arguably, the population above this line already lives in a society with highly functional, if not always efficient, markets. By the very nature of national wealth, the poorer members of this segment are also highly underwritten by government support programs. While return-oriented impact investors can find many opportunities in this segment (such as social impact bonds and CDFIs), here we restrict ourselves to developing economies.

In-between these boundaries, there is a middle population—3 billion people—with tremendous investment opportunity for return-oriented impact investors. Above the $3/day level, formal markets begin to coexist with informal ones, and true businesses emerge. Here, adults have some job skills. As you move up to the income scale, this only gets better—particularly when you consider that the working class has a very good sightline to the advantages of economic wealth. Particularly in cities, people across income levels interact with one another on a daily basis.

Here is where “financial-first” impact investors have the greatest opportunity to earn a return on deployed capital while building financially sustainable businesses to pull up under-represented markets. Some will argue that focus on this segment excludes the most impoverished and that return-oriented emerging market investors already dominate this space. This is partially true, but by no means exclusionary when it comes to opportunities to provide enhanced social benefit to selected communities within this income band. In future articles, I will address these concerns with explicit examples of successful investments that are specifically designed to strengthen disadvantaged communities without sacrificing return expectations.

Read more stories by Bo Hopkins & Abi Olvera.