(Photo by iStock/BjelicaS)

(Photo by iStock/BjelicaS)

Impact accounting is the heir apparent to ESG (environmental, social, governance) accounting and investing. Where ESG investing emphasizes risks to the firm, impact accounting measures how corporate actions help or harm people and the planet. Its advocates predict impact accounting will engender a more transparent, responsible, and sustainable capitalism. Sir Ronald Cohen (a financier and leading advocate of impact accounting) and Professor George Serafeim (head of Harvard's Impact Weighted Accounts Initiative) claim it will "redefine success, so that its measure is not just money, but the positive impact we make during our lives."

Impact accounting has attracted influential advocates. IMF Managing Director Kristalina Georgieva describes it as "a blueprint for a hope-filled future," while former SEC Commissioner Allison Herren Lee contends it could "ensure that those who want to make an impact will make an impact where it matters most." Leading corporations have begun adopting impact accounting frameworks: BlackRock and Eisai have pilot-tested methodologies developed at Harvard University, while Kering—the parent company of Gucci—has created its own proprietary system for dollarizing environmental impact.

But impact accounting has a dark side that makes its use dangerous. In a previous SSIR article, "Heroic Accounting," we reviewed the potential for miscalculation and misuse of impact accounting measures. We also highlighted concerns about the feasibility and the perils of centralized, subjective pricing of externalities.

There is another important problem we overlooked in that review: Impact accounting has an equity problem, because practical means for calculating impacts discriminate against poor people. This flaw is challenging to correct because it emanates from impact accounting's core premise: that social and environmental effects can and should be priced and compared in global monetary terms. One recent example illustrates this defect in particularly stark terms.

The Dark Side of Impact Accounting

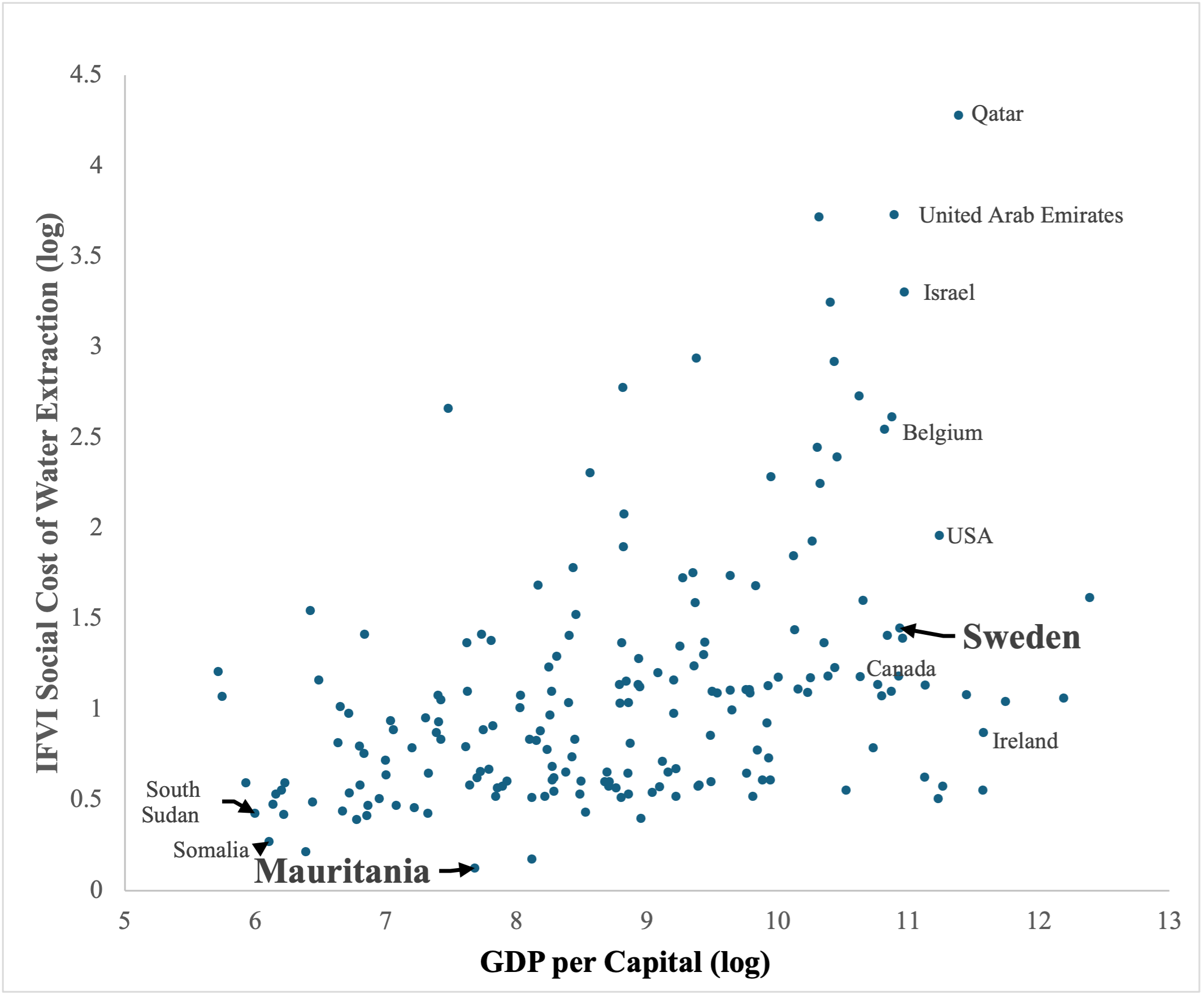

Evidence of the discriminatory tendencies inherent in impact accounting appears in a recent report by the International Foundation for Valuing Impacts (IFVI)—an organization co-founded by Sir Ronald Cohen and Tracy Palandjian (Co-founder and CEO of Social Finance). The report estimates the social cost of consuming fresh water—a resource of growing global concern—for each country. Strikingly, the IFVI assigns the lowest social cost to Mauritania, a desert nation identified by the World Resources Institute (WRI) as facing an "extremely high" risk of future water scarcity. According to the IFVI, consuming a cubic meter of groundwater in Mauritania causes only $0.13 in social harm. In contrast, Sweden—rated by the WRI as having a "low" water risk—is estimated to suffer $3.25 in social harm per cubic meter of groundwater consumed, 25 times the estimate for Mauritania.

These counterintuitive estimates are part of a general trend. The IFVI estimates a low cost of water consumption for other water-scarce nations, including Somalia ($0.27/m³) and South Sudan ($0.53/m³), but calculates a much higher social cost in some countries with abundant water resources. Even rain-soaked Ireland is assigned a higher social cost of water consumption ($0.74 /m3) than Mauritania, Somalia, or South Sudan.

Why does the IFVI assess Mauritania, Somalia, and South Sudan as places where consuming fresh water causes minimal social harm? The answer appears to lie in their poverty. In these nations, water is primarily used to produce basic goods for local consumption, which are then sold at low prices. The IFVI's methodology assumes that low prices reflect low social value, and consequently, it concludes that little harm is caused by sacrificing this production to divert water to other uses. By contrast, in wealthy countries like Sweden and Ireland, water is often used to produce higher-priced goods, including luxury items destined for global markets. The higher market prices of these goods are interpreted by the IFVI as indicators of higher social value, leading to greater estimated harm from water consumption. As shown in Figure 1, all countries assigned low social costs for water use by the IFVI are among the world's poorest, while rich countries—even those with abundant water resources, such as Sweden, Ireland, and Canada—are assigned significantly higher costs.

Figure 1: IFVI Estimate of Social Cost of Water Consumption and GDP per Capita

Figure 1: IFVI Estimate of Social Cost of Water Consumption and GDP per Capita

The IFVI's discriminatory estimates are not caused by a bug or error; they are an inevitable consequence of impact accounting's reason for being—the monetization of social impacts expressed in terms of a global unit of exchange. Monetization makes risky assumptions about the relationship between social value and its monetary expression—price. As scholars Garry Jacobs and Ivo Šlaus (2010) warned, "The temptation to measure all value in terms of price plays havoc with commonsense, reason, and human values."

In the case of impact accounting, this temptation results in systematic bias against poor people. In Mauritania, consuming water displaces activities such as subsistence agriculture, which the IFVI methodology interprets as causing minimal social harm, even though these activities are essential for survival. Conversely, in Sweden, water extraction displaces high-priced uses like decorative landscaping and is thus mistakenly assigned higher social value despite its lower importance. As a result, impact accounting risks reinforcing global inequalities under the guise of objectivity.

Why Impact Accounting Discriminates Against Poor People

Sir Ronald Cohen argues "We have to be able to measure a company's performance in delivering impacts as well as profits." But how should impact be measured? In financial accounting, price serves as a valid proxy: Managers aim to minimize the prices paid to suppliers and maximize the prices received from customers. Profit, then, reflects how effectively a firm achieves these goals. The same logic does not hold when measuring impact. Market prices do not reliably capture social and environmental outcomes and relying on price as a stand-in for value can lead to severe distortions.

Consider a manager overseeing identical facilities in Sweden and Mauritania who must decide where to invest to reduce the social impact of lost work. The manager's employees require proficiency in mathematics—and thus earn wages comparable to local math teachers: approximately $57,600 per year in Sweden and $5,000 in Mauritania. Following the IFVI's approach, the social value of lost work is calculated as the product of wage and time, and by this logic, losing a Swedish worker imposes more than ten times the social harm of losing a Mauritanian one. Consequently, to reduce the firm's measured impact the manager should invest much more money to reduce lost work in Sweden than in Mauritania. But this conclusion is irrational. Higher wages in Sweden reflect the country's robust institutions and strong economy, not a greater intrinsic value of worker labor. In contrast, Mauritania's low wages result in large part from weak governance and systemic corruption, which suppresses economic opportunity and distorts labor markets. A 2023 report estimates that at least 3 percent of Mauritanians are paid nothing at all: They are enslaved. By the IFVI's method, their work provides no social value!

The connection between good government and economic development is well established in the economics literature. "Inclusive political institutions that distribute power broadly in society and are accompanied by inclusive economic institutions create the incentives and opportunities that make a nation prosperous," write Nobel Laureates Daron Acemoglu and James Robinson in their 2012 book, Why Nations Fail. "Institutions that lack inclusivity—where political and economic power are concentrated—tend to reproduce themselves, creating a vicious circle of deprivation and underdevelopment." Accordingly, it is not a lack of social impact that causes a Mauritanian worker to receive a salary one-tenth the size of his Swedish counterpart; it is a consequence of his working in Mauritania.

Proponents of impact accounting shrug their shoulders at such concerns and respond that any accounting of social costs, even if done inaccurately, is better than no accounting at all. For example, Sir Ronald Cohen writes, "Until now, the prevailing view has been that impact cannot be measured reliably enough to be truly useful, however, in John Maynard Keynes's words, 'It is better to be roughly right than precisely wrong.'"

Unfortunately, inaccurate information can be worse than no information at all. Impact information that directs harm to the poor and dispossessed will cause a decline in social welfare, not an increase, because income has a declining marginal influence on welfare. Depriving $1000 in income to a person in Mauritania, where the average income is $2200, may cause them to have trouble surviving. Deprive that same amount to a person in Sweden, where the average income is 22 times higher, and they may not even notice.

If inaccurate information about impacts causes increased harm to poor people, social welfare will decrease. More information will not be better than no information at all.

Can Impact Accounting Be Corrected to Prevent Discrimination Against Poor People?

It might seem that the problem outlined above could be solved by adjusting observed prices or by using other methods to calculate impact. But such solutions are extraordinarily difficult to implement. For example, to compare the Mauritanian and Swedish teachers accurately, one would have to calculate the Mauritanian's wage if the country were well governed and the economy booming. This requires constructing an economic model of the national economy and then simulating how it would function under better governance. Such calculations remain at the frontier of economic theory. Even the most advanced models reduce complex economies to simplified, stick-figure representations of activity. They also require extensive data and research to calibrate and are often opaque in their assumptions and outputs. Ongoing debates surrounding models of the social cost of carbon illustrate just how contested and fragile these estimates can be. Accurately determining the "true" price of every resource in every country is, in practice, impossible.

What about simply weighting impacts in poor countries to match those in wealthy ones? In principle, this could work—but how should the weights be determined? One alternative is to use purchasing power parity (PPP)—a method of determining the buying power in local currencies for a basket of goods. It is thought to better capture cost-of-living differences than exchange rates. However, switching to PPP does not fully solve the problem. For example, it still leaves us with the conclusion that Swedish workers provide three times the social value of their Mauritanian counterparts, even if employed in the same job. The creators of the PPP system—the International Comparison Program—caution against using it to compare prices at the unit or industry level across countries because the appropriate valuation factor should vary by product and context. But calculating such variable factors would require building and validating comprehensive models of each national economy, and as with the previous approach, it would be prohibitively difficult to implement such a system.

Limiting the scope of use for impact accounting seems to be the best option. For example, impact accounting might allow for comparisons of the impacts within the same governing institution, such as the effects of extracting water in different parts of the same U.S. state. Alternatively, impact accounting could concentrate on genuinely global effects—those that transcend national boundaries—such as the environmental impact of corporate greenhouse gas emissions or global carbon sinks, such as forests and oceanic phytoplankton.

Conclusion

We hope our arguments will lead to significant changes in how impact is measured, but that is beyond our control. We expect the proponents of impact accounting to continue to promote it as the heir apparent to ESG. If they are successful, managers and investors may soon confront impact accounting measures. Some guidance in their use is in order:

1. Beware of claims to accuracy. Impact accounting measures present as precise and interpretable dollar values, but this is an illusion. They rest on layers and layers of approximations and assumptions. Understanding those layers is crucial.

2. Avoid cross-country comparisons. Using impact accounts to compare firms across borders—especially between rich and poor nations—risks serious misrepresentation. Impact measures are likely to discount harm to poor people.

3. Check against common sense. If impact accounting tells you water consumption is less harmful where water is scarce, ask why. Check against first principles. Scarcity should increase value, not reduce it.

4. Recognize that impact accounting may be just the latest idea for an easy fix to social and environmental problems. Over the past 40 years, many solutions have been proposed for leveraging the power of business to advance sustainability. All have come and gone, all but one: strengthened institutions.

5. Strengthen institutions. As Acemoglu and Johnston have shown, social outcomes are better where institutions are stronger. We don't need Nobel Laureates to tell us, we know that from experience. Controlling institutions have made our air and water cleaner, our cars safer, our resources better protected, and our living standard higher. Such institutions are constantly under attack, yet they remain the best way to improve our planet. Impact accounting will likely come and go, but the effect of our institutions will remain. So, strengthen them, be it a social club, local government, national system, or international organization. Doing that will have a real impact.

Read more stories by Andrew A. King, Ken Pucker & Jesse Colman.