Impact investing is on the ascendency, with more than $60 billion in assets under management and the potential for that number to grow quickly into the trillions. At the same time, income inequality is increasing in the United States and, as a recent Pew Research Center poll that examines “Views of Race and Inequality” (February 29 to May 8, 2016) attests, there remain striking differences in Americans’ perception of economic opportunity depending on one’s race or ethnicity. In this context, some might argue that it is impossible for the impact investing field to be a part of the solution to addressing inequality. One could even argue that, as an instrument of capitalism, impact investing is bound to perpetuate inequality,

Depending on what happens in the next few years—a critical time in the evolution of impact investing—I believe there is great potential for impact investing to alleviate the huge disparities currently evident in our economic system. But for that to happen, investors need to make sure their investments are deliberately structured to: ensure fair access to livelihood, education, and resources; compel the full participation of citizens in the target community’s political and cultural life; and foster self-determination in the community to meet fundamental needs and sustain progress.

To invest in this way, investors need to commit to overcoming entrenched barriers and practices that tend to result in increased financial equity but decreased social equity. These barriers include:

- A narrow understanding on the part of investors of the factors that influence systemic social and economic problems

- An unwillingness to reconsider the interplay between risk, return, and time horizon in an investment context

- An investor class that often assumes it knows what is best for the community rather than engaging the communities it purports to influence

Put differently, in a conventional context, investors base their strategies on a complex set of factors, including risk tolerance, the need for financial returns, and the timeframe in which they need to access returns (liquidity). Impact investors typically consider these same issues, as well as a set of desired social outputs, such as decreasing carbon emissions or creating new jobs. But impact investors who want to see socially equitable results need to take their analysis one step further and develop investment theses rooted in a comprehensive understanding of the causes of inequality. By doing so they can move from making transactional investments that result in specific outputs to developing transformational impact strategies that effect change on a systemic level.

Clearly, this is easier said than done. But some in the impact investing field—including several philanthropies—are already doing it, and we think the time has come to build on that work. Our research, which included interviews with dozens of individual investors, investment advisors, foundation representatives, and other impact investing experts, illuminated six practices we believe other investors can use to great effect to make more socially equitable investments:

- Reevaluate expectations for comparable levels of risk and return, and the time horizon for individual investments, regardless of social impact goals

- Align philanthropic capital with for-profit capital so that philanthropy can underwrite deals with greater financial risk, a longer time horizon, and potentially lower returns

- Share more risk with those who will benefit from the investments

- Consider a longer investment time horizon and lower liquidity expectations

- Develop investment theses with social equity as the main driver

- Engage beneficiaries in the investment process

The last point warrants some extra attention, but ultimately, it is straightforward: To understand, comprehensively, the ability of financial capital to address the kinds of important issues that affect any given community, an impact investor needs to understand the full scope of their investments’ impact. This is difficult to do without consulting the people most affected by the investments. And yet, investors are too often content to read reports or do Internet searches to inform their understanding of an issue. They often don’t take time to confer with potential investees before they make investments, and they very rarely engage in meaningful dialogue with investees to assess the ongoing impact of their investments, much less to inform or share in decision-making.

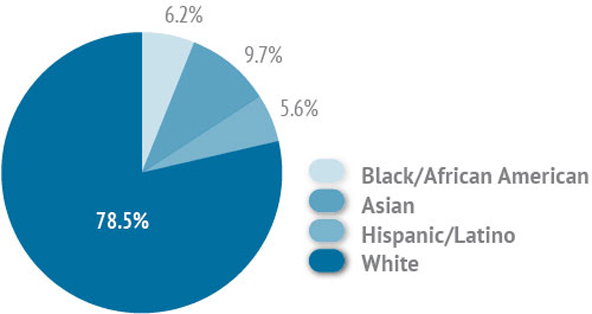

Moreover, investors and their advisors (like everyone else) have implicit biases, and thus make assumptions about people and communities they don’t know or understand. When you consider that 79 percent of employees in the financial investments industry are white and 65 percent are male, while many recipients of impact investments are low-income women and communities of color, it becomes abundantly clear why such biases might be problematic.

The race and ethnicity of employees in the financial investments industry

(Image courtesy of Bureau of Labor Statistics 2015)

The race and ethnicity of employees in the financial investments industry

(Image courtesy of Bureau of Labor Statistics 2015)

Impact investors can ensure that their investment strategies reflect and address the true issues and opportunities of the communities they’re trying to help. But until they make it their priority to do so—and until they underwrite some of the predevelopment costs that come with understanding the full impact of each product they support—the impact-investing field will continue to risk leaving opportunities for increased social equity on the table, even as financial equity continues to grow.

Read more stories by Katherine Pease.