(Photo by iStock/wildpixel)

(Photo by iStock/wildpixel)

We are at a moment where philanthropy needs to rethink its compact with society, its role in solving public problems, and its pathways to funding large-scale change. However, as trustees deliberate how to meet the biggest challenges of the moment, one issue they can take off the table is whether founding intents should constrain their conscience. Our research shows that foundation boards have room to maneuver, perhaps more than they realize.

In a study we’ve made of the articles of incorporation and bylaws of the top 50 private foundations in the U.S., funded by Lodestar Foundation, we found no indication that founding intent, nor endowment recovery, prevented or constrained trustees from leveraging endowment dollars when they felt that circumstances and mission merited it. We even found a surprising amount of fluidity in amending intent, where trustees felt compelled to do so. And perpetuity foundations like Carnegie Corporation, James Irvine, and Annie E. Casey (AEC) are paving the way to changing the everyday payout norm: all three have for years targeted payouts greater than the IRS-required minimum of 5 percent of investment assets, with AEC paying out from 6.6-to-10.5 percent per annum for the past decade.

Founding Intent as Moveable Feast

Twenty-seven of the top 50 foundations were incorporated in perpetuity, with combined endowments of $93 billion in 2018. The other 23— $159 billion in investable assets (about 30 percent from The Bill and Melinda Gates Foundation)—either don’t mention perpetuity in their Articles of Incorporation or Bylaws, provide for dissolution at an unspecified date, or specify they will spend down within a given timeframe. However, we found precedents to indicate that any foundation—perpetuity or no—could decide as a board to increase payouts and/or alter their founding intent to spend down, given the will of trustees, time, and persuasion of their state Attorney General (AG) where incorporated. And if the founding donor is still living, the conversion process can be very swift: three months after incorporating Bloomberg Family Foundation, for example, Michael Bloomberg amended the intent from perpetuity to spend down and then amended the terms of spending down nine years later.

If the donor has passed and family control is diluted it can take longer. “Things get complicated,” as Michael Cooney, head of law firm Nixon Peabody’s nonprofit and foundation practice, told us in an interview. Even if trustees make a strong case for amending intent in keeping with contemporary need, the AG can force the decision before a judge. “That court proceeding could take six months to a year, often depending on the dedication of resources from the AG,” said Cooney.

The Houston Endowment, for example (No. 46 by size in 2018), pivoted from spend down to perpetuity, 13 years after its founder’s death. Incorporated by Texas construction magnate Jesse Jones in 1937 with a mandate for trustees to “carry out the activities of the corporation without limitation to the amount distributed,” Jones’ initial founding articles foresaw spending down in 50 years. Jones and his wife established the endowment out of the Great Depression, and may well have thought that after building up Houston arts, hospitals, education, and civic institutions their work would be done. However, after the Tax Reform Act of 1969, trustees converted extensive real estate and business assets nested in the endowment into investable assets and in 1971 amended intent to perpetuity.

Endowment Recovery Not Linked to Higher Payouts

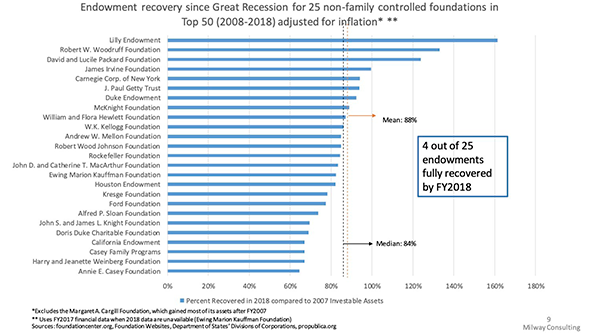

To assess the relationship between endowment recovery and risk-taking, we looked at major pandemic recovery commitments vs. foundations’ endowment recovery from the Great Recession of 2008-09 (calculating in 2007 dollars, removing founder or founder-family controlled foundations from the list to focus on those guided primarily by founding documents). Only four endowments were fully recovered by 2018: Irvine (perpetuity), David and Lucile Packard Foundation (non-perpetuity), Robert W. Woodruff Foundation (perpetuity), and Lilly Endowment (non-perpetuity). Among the 25 foundations without a living founder/founder’s family, the spread of endowment recovery ranged nearly 100 percentage points, from an inflation-adjusted 64 percent (AEC, incorporated in perpetuity) to 161 percent (Lilly, whose articles empower the board to give with “uncontrolled discretion, all or any part of the corporation's income as well as all or any part of the corporation's corpus or principal assets”).

To roughly estimate endowment recovery beyond publicly available financials, we projected rates through 2020 in 2007 dollars, pegged to the S&P’s trajectory of the past two years through June, assuming foundations maintained stable investment strategies (which, of course, not all did). The results forecast only seven endowments recovered by 2020. However, neither recovered nor enlarged endowments, be they founded in perpetuity or not, were most aggressive in COVID-era decisions to increase payouts.

Instead, on June 11, five foundations not projected to be recovered from their pre-recession high-water marks (Ford Foundation, John D. and Catherine T. MacArthur Foundation, Doris Duke Charitable Foundation, W.K. Kellogg Foundation, and Andrew W. Mellon Foundation) announced they each would issue a bond to increase their collective grant-making more than $1.7 billion over the coming two years in response to COVID-19. Last month, Rockefeller Foundation, also projected not to have recovered, announced it would make $1 billion of grants to ensure a “green and inclusive recovery” from COVID-19, drawing on resources from its endowment and a bond offering. Three of these foundations—Ford, Doris Duke, and Kellogg—were founded explicitly in perpetuity. Founding intent notwithstanding, their boards of trustees were able to justify aggressive, financial decisions in keeping with the times and their collective conscience.

Opportunities for Increasing Payouts

In all, 34 of the Top 50 foundations in the U.S. (73 percent by assets) have either living donors, are family controlled, or are not founded explicitly in perpetuity. It follows that their boards could decide to multiply payouts for crisis response, within institutional guidelines for prudent spending, either without a formal process to amend foundation intent, or with a fairly rapid one.

The decisions by trustees of MacArthur, Mellon, and Rockefeller foundations to issue bonds to fund massive COVID-19 response funds are of this kind: their articles of incorporation do not specify perpetuity. Gates, explicitly incorporated to spend down, also has far surpassed the 5 percent minimum, adding multiple big-bet grants since pandemic onset to fund COVID-19 testing, treatment, and vaccine development. But boards of grantmakers founded in perpetuity—Ford, Doris Duke, Kellogg—are also making this decision. These boards count response to deep crisis as mission imperative, and will look to endowment growth to cover the cost of debt.

“We believe the unique urgency of this crisis justifies foundation trustees’ deciding to increase spending,” said Ford executive vice president Hilary Pennington, “Even if it might mean reducing the long-term spending power of their endowment. Many perpetual foundations are already willing to take that risk, even including many that have not yet regained their pre-2008 endowment values. We believe others should consider it as well, regardless of their perpetual status.”

In another camp, foundation trustees assert that with thoughtful math and wise investments (vs. taking on debt), they can increase payouts near term and recover within a decade or two. This is the bet that nearly 300 smaller, private foundation and donor-advised fund holders and advocacy groups are making in calling Congress to mandate that philanthropy increase payouts to 10 percent for three years as an Emergency Charity Stimulus (ECS). An Institute for Policy Studies briefing paper estimates that the ECS would generate an additional $189 billion in foundation grants to nonprofits, plus $11 billion from donor-advised fund holders for a total of $200 billion. Meanwhile, another foundation initiative, the Crisis Charitable Commitment, calls for payout boosts by asset volume this year, starting with 6 percent payout on the first $50 million. And last week powerful funder voices coalesced around the Initiative to Accelerate Charitable Giving, calling Congress to reforms that would ensure, among other things, that foundations aren’t penalized for payout increases.

While such giving won't substitute for a government stimulus in the trillions, Scott Wallace of the Wallace Global Fund, a spearhead of the ECS petition, cited the benefit to taxpayers of leading the stimulus with money already set aside for charitable purposes. "My reassurance for foundations worried about perpetuity is that it's possible to recapture growth with a 5 percent payout when the S&P 500 has grown at 7.5 percent over its entire history," said Wallace.

A 2018 simulation of a spectrum of foundation payouts over years including economic downturn supports this notion. It concluded that private foundations could sustain themselves with a 7 percent payout during bounded, recessionary times. The study, by Lilly Family School of Philanthropy professor Patrick Rooney et al, with samples of 50,000 for each rate tested, further found that raising payouts as high as 9 percent over the next 100 years would shrink assets over time, but not risk foundation closure.

Challenges to Increasing Payouts

Despite compelling arguments for increasing payouts near term and hope to recover, the historically slow pace of recovery does create a challenge for foundations debating higher payouts versus stewarding purpose. Indeed, 21 of the 25 endowments we studied had not recovered by 2018 from losses in 2009, and 18 were projected to lag through 2020. Some still recovering, like the Houston Endowment, focus on perpetually supporting public institutions and well-being in a specific city. Others, like the J.P. Getty Trust, were founded to operate national institutions, i.e. The J.P. Getty Museum and related art institutes, in perpetuity.

One perpetuity foundation, the William and Flora Hewlett Foundation, with a focus on long-term issues like climate change, had recovered 87 percent of investable assets by 2018 from losses incurred in the Great Recession. Its president, Larry Kramer, stated in a letter to grantees in March 2020 that in response to COVID-19, Hewlett would maintain budgeted grants, despite a drop at the time in its endowment, but not increase payouts, in order to ensure resources for long term goals.

The Council on Foundations echoed Kramer’s concerns, but also signed, with eight other philanthropic support organizations, an open statement encouraging increased giving by all funders. CoF’s vice-president of government affairs and strategic communications, David Kass, told us that some of CoF’s 749 foundation members were increasing payouts or shifting them to COVID-19 response, but CoF would not support the ECS proposal in front of Congress, saying “If you require this kind of change, what happens for the next crisis?”

There are structural issues, too, that weaken arguments for boosting payouts. One, not currently raised in the payout debate before Congress, is finding a mechanism to equitably distribute billions of dollars of additional grants should the ECS pass.

The struggles of nonprofits led by people of color and serving vulnerable communities to obtain government stimulus funds through the Payroll Protection Plan (PPP) indicate that creating equitable access to increased resources may be the biggest challenge. (And PPP loans had just one set of guidelines, one funder, and one genre of distribution channel—banks). Beyond increasing payouts, there would need to be serious thought and discussion related to how nonprofits most in need could navigate grant applications for resources unlocked by hundreds of grantmakers. One channel to consider would be Community Foundation-based COVID Response funds, now in place across all 50 states.

A second, structural issue, addressed by the Initiative to Accelerate Charitable Giving, lies in U.S. fiscal policy, which docks foundations for increasing payouts for short periods. Summarized Rooney of the Lilly Family School, “The excise tax as currently structured penalizes foundations for paying out more than the minimum rates of 5 percent in a time of crisis, by adding taxes if they return to their prior levels later. I think it’s one of the biggest blockages for supplemental payout rates.” In their study, Rooney et al propose alternatives, such as an excise tax only if the foundation does not pay out at least five percent in any given year. The Initiative before Congress proposes exempting the tax altogether for foundation payouts topping 7 percent of assets or spending down in 25 years or less.

Last month, the Hewlett Listening Post looked at research on the rise of new philanthropic norms and vehicles out of The Great Depression, often in partnership with government. Almost a century later, philanthropy faces another such inflection point. Big bet grant-making is innovating, from investment platforms like Blue Meridian Partners, to LLCs like the Chan-Zuckerberg Initiative, and mega giving out of donor-advised funds. One tribute boards of private foundations can pay their founders is to revisit their purpose, rethink their compact with government and society, and ask themselves where paying out more, sooner, may better solve, versus merely serve, the problems at hand.

(The authors thank Alison Powell, Ellie Buteau, Fay Twersky, Hilary Pennington, Jerry Hirsh, Lois Savage, and Patrick Rooney for their input.)

Read more stories by Katie Smith Milway & William Galligan.