(Illustration by David Herbick)

(Illustration by David Herbick)

Over the past twenty-five years the composition of the boards at some of America’s most important nonprofit organizations has dramatically changed. Without much notice, a legion of Wall Street executives (investment bankers, hedge fund managers, and others) has taken a growing number of seats in nonprofit boardrooms. Not only that, they hold a disproportionate share of the leadership positions on these boards.

One of the obvious reasons for this shift is undoubtedly the pressure that nonprofit organizations are under to raise more private funds. After all, given the significant growth in personal wealth generated by those working in high finance, it shouldn’t be too surprising to find more of them on nonprofit boards. A more subtle reason for the growth of financiers on nonprofit boards is likely the growing popularity of using business approaches (and talent) to run nonprofit organizations.

Since 2008, when Matthew Bishop and Michael Green popularized the term “philanthrocapitalism” to describe a new trend of donors seeking to conflate business aims with charitable endeavors,1 the nonprofit sector has engaged in active interrogation and discussion about the trend and its effect on public charities.2 Scholars and practitioners have documented various pressures placed on nonprofit organizations by donors and private foundations to adopt business approaches.

Although some of the pressure to adopt business approaches has come from external forces, it may also be true that the concepts and norms of philanthrocapitalism are also now carried into nonprofit organizations by the directors of public charities themselves. Perhaps a new fault line to consider is the very makeup of the governing boards of nonprofit institutions.

To understand the ways in which the composition of nonprofit boards has evolved in recent years, my research team and I examined the biographies of governing directors in 1989 and 2014 of three sets of nonprofit organizations: major private research universities, elite small liberal arts colleges, and prominent New York City cultural and health institutions. The most striking finding was the sizable presence and growth on charitable boards of those whose primary professional background and skill set were drawn from the financial services industry. The tally indicates that the percentage of people from finance on the boards virtually doubled at all three types of nonprofits between 1989 and 2014.

More striking, the data reveal that finance professionals hold an even greater percentage of nonprofit board leadership positions (i.e., board chair, vice chair, or their equivalent). In the case of liberal arts colleges and New York City nonprofits, financiers make up 44 percent of board leadership positions, and in the case of private universities they hold 56 percent of leadership slots.

Of course the social sector, especially the largest and most powerful nonprofit organizations such as those represented by the three types of institutions studied, has long populated its boards with men and women of wealth and professional backgrounds tied to the corporate world. Indeed, it is not unusual for many (although not all) of such members to have the capacity to contribute substantial resources, especially those from business and industry. What’s new is the increased concentration of directors drawn from one narrow sector of business and industry: finance.

This quiet yet dramatic self-transformation of the nonprofit boardroom has come about with little notice and discussion. To understand fully these trends and the impact, the nonprofit sector should ask itself some tough questions: What is sparking these changes in board composition? What values are being represented and promoted? What are the consequences for organizations and the people they serve? How might they affect the quality of board governance? How might the sector respond?

This article begins to shed light on the increasing influence of the finance industry on nonprofit boards. In addition to examining the data, it explores some of the explanations and consequences of these prevailing governance composition choices—and they are choices—that deserve attention and reflection from nonprofit leaders, trustees, and constituents.

Financial Executives Gain Power

When people examine nonprofit boards, most of the focus is on governance practice issues such as size, structure, meeting frequency, and term length. Less attention, however, has been paid to fundamental issues of board composition and demography. And when people do examine these issues, they tend to focus on the gender and racial makeup of boards. Very little attention is paid to what industry board members hail from or whether there is enough job-related diversity. These questions are particularly relevant at a time when “some people believe that public governance is overly affected by corporate interests.”3

Finance is a vital part of the US economy, but the sector is actually quite modest in size. In 2012, finance and insurance represented 7.9 percent of US gross domestic product, and according to the US Bureau of Labor Statistics, the financial services industry employs just 6 percent of the private non-farm workforce. If nonprofit boards were composed of a representative group of people from society, one would expect trustees with a finance background to represent roughly 6 to 8 percent of board members.

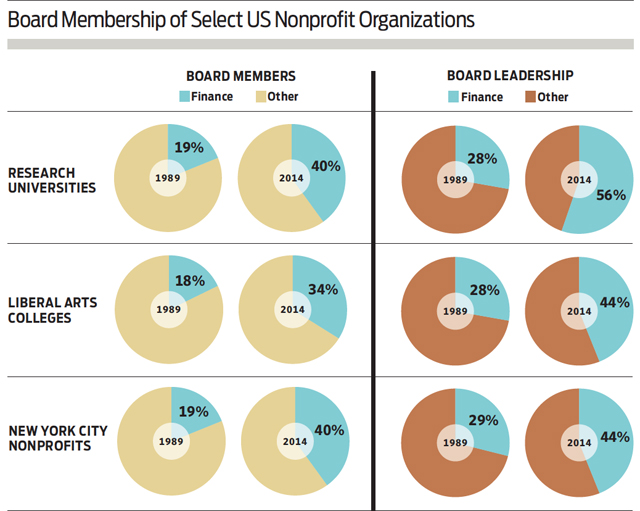

Instead, according to our research, trustees with professional backgrounds and skills primarily from the financial services industry represent about four times that number at major private research universities, liberal arts colleges, and New York City-based nonprofits. (See “Board Membership of Select US Nonprofit Organizations” below.)

Research universities | Our research found that in 2014, 40 percent of directors at major US private research universities had a substantial professional career in finance. This represents a dramatic increase from 1989, when trustees with a finance background represented 19 percent. Even more alarmingly, directors with a finance background represented a majority, 56 percent, of board leadership positions in 2014, up from 26 percent in 1989.

To arrive at these figures we reviewed the biographies of more than 1,700 members of the governing boards (not including emeriti or honorary members) in 1989 and 2014 of 23 of the nation’s leading private research universities: Boston College, Brandeis University, Brown University, California Institute of Technology, Columbia University, Cornell University, Dartmouth College, Duke University, Emory University, Georgetown University, Harvard University, Johns Hopkins University, Massachusetts Institute of Technology, New York University, Northwestern University, Princeton University, Rice University, Stanford University, University of Chicago, University of Pennsylvania, Vanderbilt University, Washington University in St. Louis, and Yale University.

Board members whose biographical backgrounds could not be found and those whose professional biographies revealed no discernible professional career but who were married to someone in financial services were not included in the data. (This was also the case for liberal arts colleges and New York City nonprofits.) If spouses of people whose wealth was drawn from the financial services industry were included, the number of finance-related board membership slots at these nonprofits would all be even higher.

Liberal arts colleges | Finance executives are also well represented on the boards of leading US liberal arts colleges. In 2014, 34 percent of board members came from the finance industry, almost twice as many as in 1989, when they accounted for 18 percent of board members. When we look at board leadership, the percentage of finance professionals holding those positions at liberal arts colleges rises to 44 percent, up from 28 percent in 1989. The percentage of directors from the finance industry at liberal arts colleges is smaller than at research universities, but the number is still quite large in comparison to their numbers in the overall workforce or the economy.

Following the same procedures used with the private research universities, we reviewed more than 1,750 biographies of the governing board members of 29 liberal arts colleges in 1989 and 2014: Amherst College, Barnard College, Bates College, Bowdoin College, Bryn Mawr College, Bucknell University, Carleton College, Claremont McKenna College, Colby College, Colgate University, Colorado College, Davidson College, Grinnell College, Hamilton College, Haverford College, Kenyon College, Lafayette College, Macalester College, Middlebury College, Mount Holyoke College, Oberlin College, Pomona College, Smith College, Swarthmore College, Trinity College (Connecticut), Vassar College, Wellesley College, Wesleyan University, and Williams College.

New York City nonprofits | To see whether these board composition practices were limited to higher education, we examined a third set of select nonprofit organizations made up of high-profile New York City-based nonprofit institutions, primarily, but not exclusively, in the arts, cultural, and health care sectors. The findings were startlingly consistent with those of the research universities and liberal arts colleges. People from the finance industry accounted for 40 percent of board seats at select New York City nonprofits, more than double the number, 19 percent, in 1989. Finance executives held 44 percent of the leadership posts at these nonprofits in 2014, up from 29 percent in 1989.

Many of these high profile organizations are among the most well-endowed and most successful fundraisers in the social sector, making them worthy of study. In fact, 11 of the 15 organizations were included in the Philanthropy 400, compiled annually by the Chronicle of Philanthropy and listing public charities that have raised the most money from private sources. Of course, in choosing organizations based in New York City—the heart of financial services in the United States—we are focusing on a specialized segment of the nonprofit sector, but neither the changes between 1989 and 2014 nor the overrepresentation in board leadership is explained by a proximity to Wall Street.

Using the same biographical analysis methods as with universities and liberal arts colleges, we analyzed more than 1,050 trustees at 15 prominent New York City-based institutions. These are some of the most sought after and prestigious board positions in the United States: American Museum of Natural History, Carnegie Hall Corporation, Central Park Conservancy, Frick Collection, Lincoln Center for the Performing Arts, Memorial Sloan Kettering Cancer Center*, Metropolitan Museum of Art, Metropolitan Opera Association, Museum of Modern Art, New York Community Trust, New York Public Library, New York-Presbyterian Hospital, Whitney Museum of American Art, WNET/Thirteen, and the Young Men’s & Young Women’s Hebrew Association, a.k.a. 92nd Street Y. (*1989 board composition data was not available for Sloan Kettering.)

Why Nonprofits Favor Financiers

Because board composition and board leadership decisions often occur behind closed doors through opaque processes, each individual selection may seem sui generis. But the data suggest trends and shifts that are remarkably similar across all three types of nonprofits that we studied. How do we explain this development? The most obvious answer is that nonprofit organizations are simply following the money. Driven by the heightened pressure and expectations to raise ever larger sums, nonprofit boards and managers are selecting new board members with an eye toward those with the greatest capacity for making “transformative gifts.”

In today’s economy, superstar money managers certainly outstrip the earning power of most others. For example, in 2010, in total the top 25 hedge fund managers earned nearly four times as much as the 500 chief executive officers of the Standard and Poor’s 500 companies, and the average top 25 hedge fund manager took home nearly 178 times as much as the average law partner of a top 50 law firm.4

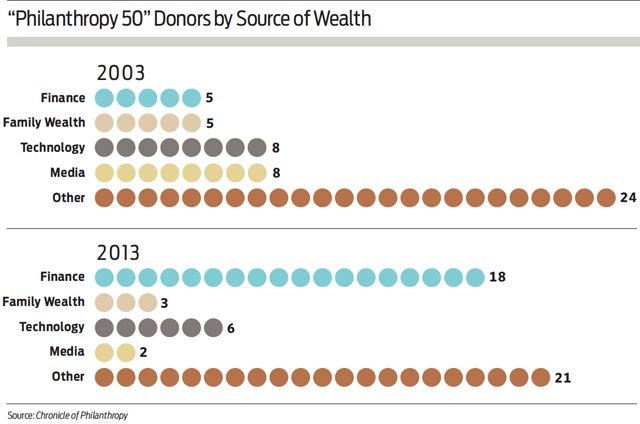

Moreover, a disproportionate number of the largest charitable gifts in recent years have come from people in the finance profession, a point almost certainly understood and internalized by sophisticated organizations with ambitious fundraising goals. Between 2003 and 2013, the percentage of the 50 largest US donors whose source of wealth was finance soared from 10 percent to 36 percent. (See “‘Philanthropy 50’ Donors by Source of Wealth” below.)

(Source: Chronicle of Philanthropy)

(Source: Chronicle of Philanthropy)

Well-endowed nonprofit organizations, with millions or even billions of dollars under management, may also have an incentive to bring increasing numbers of finance professionals onto their boards to help oversee their complex portfolios and, perhaps more important, to provide access and connections to sophisticated investments. In Capital in the Twenty-First Century, Thomas Piketty’s meditation on wealth and income distribution, the author makes an argument—succinctly summarized by economist Paul Krugman—that “it’s generally more valuable to have the right parents (or to marry into having the right in-laws) than to have the right job.”5 To borrow from Piketty, for the wealthiest nonprofit institutions it may be more valuable to have access to the right investment advisors and vehicles than to have the right income stream. Even in a time of astounding fundraising, outstanding investment performance has the potential to reap substantial rewards.

Consider Amherst College. In 2001, as it neared the conclusion of a seven-year effort to raise $200 million in its then-record-setting capital campaign, the endowment performance for that single year generated returns in excess of $200 million. (In 2013, Amherst celebrated the conclusion of another capital campaign, which raised $502 million—$77 million above its goal—increasing its total endowment to more than $1.82 billion, a bit more than $1 million per student.)

How Financiers Are Changing Nonprofits

As financiers come to dominate the boards of leading nonprofits, it is not surprising that their approaches and priorities have made their way, very explicitly and fundamentally, into the governance of the nonprofit sector. Practices such as data-driven decision-making, an emphasis on metrics, prioritizing impact and competition, managing with three- to five-year horizons and plans, and advocating executive-style leadership and compensation have all become an essential part of the nonprofit lexicon.

Nonprofit leaders regularly hear about these finance practices from board members and donors whose native habitat is the financial services world. Moreover, nonprofit managers have come to accept them as reasonable principles upon which donors base their giving. More often than not, organizations are also expected to incorporate these principles in the management of the not-for-profit enterprises for which managers and boards share responsibility.

Although many of these business approaches may strengthen nonprofit capacity, we should also be mindful of the ways in which these same tools can morph into pathologies, ignore the costs or trade-offs associated with extending business thinking to the charitable sector, or distort organizational priorities. Numerous critics have written thoughtfully about the ways in which market-based thinking and approaches applied to the nonprofit sector provide false promise, with the potential to dilute charitable values, undermine long-term mission focus, incentivize small, incremental goals, and threaten shared governance and other forms of participatory problem-solving.

Beyond leading to the borrowing of financial concepts and tools in the boardroom, the rise in the number of nonprofit directors with ties to finance may also contribute to deeper changes in the underlying institutional values and motivations, a trend that economic sociologists refer to as the financialization of the nonprofit sector.

Financialization describes a spread of financial logics, influence, and strategies into new fields and organizations in ways that transform the culture, policies, and values of institutions.6 Indeed, wealthy nonprofits—like colleges, universities, and museums—have long engaged with financial markets as endowment investors, but the scope and scale of today’s nonprofit borrowing, aggressive debt financing, securitization transactions, and complex real estate transactions is unprecedented. Such shifts may affect the organization’s strategic direction and orientation in a number of ways, including directing board and management attention to debt service, incentivizing organizations to invest resources on activities that return higher profit margins to cover debt service, elevating the centrality and importance of financial managers in strategic planning and decision-making, and increasing the need for and power of senior staff well versed in complex financial instruments.

To be sure, the growing presence of finance executives on nonprofit boards may not be the only reason for the growing presence of business tools and practices in the nonprofit sector. Certain private foundations and other funders are surely contributing to the pressure on nonprofits to adopt these practices. Many nonprofit consultants promote these ideas. Nonprofit management programs in colleges and universities contribute to the promotion of business approaches. And publications, including this one (Stanford Social Innovation Review), have also played a role. But the growing presence of financiers on the boards of nonprofits is certainly one of the most important reasons for this trend.

Why Board Diversity Matters

Another significant impact from having so many people from finance on the boards of nonprofits is that it crowds out people from other parts of society and reduces board diversity, an important element of governance. Traditional narratives about board governance, especially nonprofit governance, almost take for granted the desirability of having a considerable degree of diversity among board members. To the extent that board members have a mix of educational, cultural, functional, and industry backgrounds, they are more likely to exhibit useful differences in the ways that they perceive, process, and respond to issues they might confront on the board. Diversity of this sort clearly enhances the presence of functional area knowledge and the skills of the board.

One of the reasons diversity is important is that it can produce what social psychologists call “cognitive conflict”—task-oriented differences in judgment among group members that emerge when they are faced with interdependent and complex decision-making. It is the clash of perspectives and the expression of dissenting views that help uncover underlying assumptions, change outlooks, and stimulate conversations around topics.

Since cognitive conflict involves the use of “critical and investigative interaction processes,” it can enhance a board’s performance in dealing with complex and ambiguous matters. These differences can broaden a strategic perspective by forcing more discussion, explanation, justification, and possibly modification of positions on important issues and encouraging consideration of alternative views and courses of action.7 Because these benefits come from diversity, when the number of directors from a single industry reaches rates as high as 40 percent, boards are likely to have less cognitive conflict and therefore less effective group decision-making.

Another drawback of having so many board members from finance is that it increases the likelihood that the financiers will turn to financial jargon when communicating. This may prove frustrating to other board members, making them less inclined to offer information or opinions that highlight their expertise or perspective. It may also create “in-group” and “out-group” divisions on the board that divide the collective body rather than bring the members together for effective work. All of this can lead to the uncritical adoption of financial concepts, approaches, and values at the nonprofit.

Moreover, the benefits of collective decision-making embodied by the synergistic combination of diverse talents and strengths represented by a board8 can be undermined if professionals from one industry become predominant, potentially leading to groupthink. The social phenomenon of groupthink occurs when cohesiveness and a sense of social belonging (i.e., a clubby camaraderie) lead otherwise independent and well-meaning individuals to prioritize unanimity, loyalty, and peer approval over considered reflection. Indeed, these are most often subconscious actions.9 As Benjamin N. Cardozo School of Law Professor Melanie Leslie argues, “nonprofit boards are extraordinarily vulnerable to ‘groupthink.’… Board members’ preferences for consensus, approval, and group solidarity can intensify the effect of pre-existing biases that impede rational decision-making, such as confirmation bias, in-group bias, and overconfidence in one’s ability to act fairly.”10

Those concerned about the racial and gender demographics of nonprofit boards should also be alarmed that close to 40 percent of board seats (and an even higher percentage of board leadership positions) are allocated to people from an industry that is not particularly diverse. According to the US Equal Opportunity Commission, in 2012 women made up 40 percent of all employees but just 17.8 percent of executive and senior level managers in positions in the “securities, commodity contracts, and other financial investments and related activities” category.11 (In the subcategory of investment banking, the numbers dropped further to 34.7 percent and 15.6 percent.12)

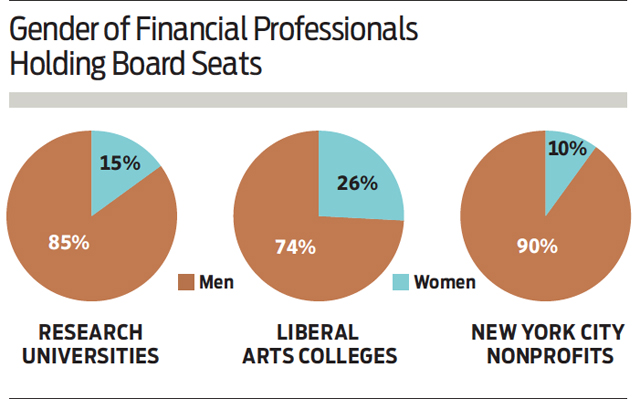

For racial minorities, the numbers in the finance category are similarly paltry, with blacks holding just 1.4 percent of executive positions and Hispanics holding only 2.3 percent.13 This smaller representation of women and racial minorities in finance has a similar impact on nonprofit board representation. Men hold the overwhelming majority of the nonprofit board seats held by the finance professionals. (See “Gender of Financial Professionals Holding Board Seats” below.) Definitive information about the racial identity of trustees could not be determined from the biographical research, but it is likely that blacks and Hispanics make up a small percentage of the finance executives sitting on the nonprofit boards.

In the case of colleges and universities, in particular, racial and gender diversity are essential if board policies are to be perceived as legitimate and receive backing from the institution’s varied constituencies. For instance, decisions related to sexual assault policies, tenure procedures, and work-family balance policies, among other issues, would benefit greatly from having both men and women on the boards of affected institutions. Similarly, debates about admissions policies, free speech and harassment, and financial aid policies will be enhanced and more credible with the meaningful contributions of trustees of color.

Of course, having a diverse group of decision-makers is necessary, but not sufficient, to guarantee quality decision-making. In addition to identity-based representation, the best boards should also take care that there is ample inclusion and weighty voices of those with substantive commitments to equity and diversity issues to ensure that those values are woven into the guts of the institution. But no matter the type of organization, board demography (“who we are”) communicates powerfully to constituents, staff members, partners, and vendors about institutional priorities, values, and commitments.14

Accordingly, gender and racial parity on nonprofit boards becomes exceedingly challenging when a significant portion of directors is drawn from the finance industry. In theory, organizations can use the remaining board seats to attempt to achieve their diversity goals, but a tension surely arises from this approach. With approximately two of five seats taken by finance professionals and, if this trend continues unabated, perhaps soon reaching one of two seats, then the game of musical chairs and competing priorities will only intensify. Furthermore, such a system places substantial burdens on the other professions and industries from which directors might be drawn (e.g., accounting, advertising, agriculture, consulting, consumer products, education, energy, health care, legal, manufacturing, marketing, media, nonprofit, operations, retail, and technology) to provide diverse directors in a way that effectively gives the finance industry a pass.

Perhaps even more significant, the data show that finance professionals are more likely than their peers to be in board leadership positions. In each of the three types of nonprofits we studied, the percentage of finance professionals in leadership positions grew during the twenty five-year period, in some cases substantially This pronounced discrepancy raises further questions about how we make sure diverse voices are at the table and involved in decisions at the board leadership level. Because nonprofit boards are often much larger than the typical corporate boards, the chairs and vice chairs can influence especially important decisions, such as setting board agendas, making board assignments and committee placements, meeting frequently with key staff, and reviewing the executive director’s performance. On many boards, nonprofit boards especially, the difficult decisions—the ones that lead to the greatest institutional change—are often heavily debated and influenced by board leadership.

The Future of Nonprofit Boards

Individual finance professionals do bring skills, wisdom, and other positive attributes to nonprofit boards. Wall Street executives have had storied careers in volunteer nonprofit board governance. Take John C. Whitehead, for example. During his career the former co-chairman and senior partner of the investment banking firm Goldman Sachs & Co. chaired the boards of more than eight major nonprofit organizations, including the Brookings Institution and the International Rescue Committee, and he sat on the boards of nearly a dozen more, including the J. Paul Getty Trust and Nature Conservancy. Most boards would surely benefit from having a modern-day John Whitehead on them. My concern, however, is that nonprofit organizations may suffer if their boards are dominated by members of any single narrow industry.

Boards and board governance are inevitably shaped by the identity and background of those who make up the boards themselves. Board members carry with them interests, priorities, mental maps, systems, expectations, and cultural norms undoubtedly shaped by their own experiences and professional backgrounds, all of which certainly affect the ways in which they carry out their duties. This is not to say that finance professionals care less (or more) about a nonprofit organization or its mission. Nor do I believe that all finance professionals think alike. But if boards are to operate as designed, and if they are to be maximally effective, then the composition of nonprofit boards must be more diverse and not dominated by financiers.

The concentration of nonprofit board power in the hands of finance professionals is quite striking. As we think about the sector in its entirety and who gets the opportunity to govern its most prominent organizations, these data reveal a great deal about where priorities have been placed and perhaps even why some critics—including nonprofits themselves—believe nonprofits are inappropriately appropriating business practices and models. For the sake of fundraising and achieving important financial goals, finance professionals are quietly accumulating unprecedented power in nonprofit boards. Fundraising and the ability to secure resources will always be critical board priorities, but nonprofits should be wary not to be led down a path where those priorities distort or limit nonprofit governance.

So what could be done to mitigate the extreme concentration of financiers on nonprofit boards? The first step is that nonprofits should begin to give far more consideration to industry diversity and representation as they recruit new board members. The effectiveness of any board recruitment and selection process, however, depends on the people overseeing the process. Those gatekeepers—nomination and governance committees, chief executives, advancement staff, and board members—always need to be aware not only of each individual member selection but also of the effects of high concentrations of professionals from a single industry.

When selecting board members, nonprofit organizations should not be unduly focused on recruiting people from the finance industry just because they may have the ability to contribute money. Setting up the organization for good governance must matter too. It is important not to undervalue contributions of those who might contribute to the mission in a myriad of other ways. Organizational leaders, from both senior staff and board levels, need a suspicious and watchful eye on the development pressures that contribute to board membership and board leadership decisions that further exacerbate this phenomenon. Industry diversity (along with gender and racial diversity) needs to become an important and real part of more boardroom conversations. How boards behave, the work they take on, the decisions they make, and the manner in which they interact with one another and management is a function of who is on the board. Everyone who cares about the fate of nonprofit organizations has a stake in this issue.

For those who do not believe the status quo presents a problem, a reasonable question to consider is this: Where is the reasonable line? If 40 percent from the finance industry is acceptable, what about 50 percent? 60 percent? Is there a tipping point?

In the long term, creating a more balanced board will require difficult and sensitive conversations for the nonprofit sector. Nonprofit organizations and their leaders, incentivized to follow the money, have been largely silent about this dramatic shift. But questions of governance effectiveness and access to leadership are too important to sweep under the rug. Is this the system we want? Are these sets of practices likely to bring about the social change we desire and envision? Do they appropriately tell the story about “who we are” and “who we want to be”? These questions and their answers may be uncomfortable. But if governance is leadership, all those associated with the nonprofit sector will need to participate in the discussion and solution.

Read more stories by Garry W. Jenkins.