(Photo by iStock, beaker, money; photo illustration by David Herbick)

(Photo by iStock, beaker, money; photo illustration by David Herbick)

The power of science to change the world should be self-evident. Consider the immeasurable impact that science and engineering innovation had on social conditions during the 20th century. The first half of the century produced the assembly line, the airplane, penicillin, and a vaccine for tuberculosis; the second half brought the eradication of polio and smallpox. Scientists harnessed the power of the sun with photo voltaic cells, invented the birth control pill, and sequenced the human genome. Work done in research laboratories sparked a Green Revolution: In the 1960s, rice yields in India were about two tons per hectare; by the mid-1990s, they had risen to six. In the 1970s, rice cost about $550 a ton; in 2001, it cost less than $200. By June 2012, more than one-third of all people on earth had used the Internet—a system built on the backbone of science and engineering research conducted in the 1960s.1 In each of these cases, the results of scientific discovery yielded both public goods and private fortunes.

Today, research discoveries languish in ivory towers for lack of entities that are willing, able, and properly structured to invest the capital necessary to build lasting organizations that can move those discoveries from the lab to the field.2 People in the university community lament the growing “idea-to-impact gap” (sometimes known as the “valley of death”).3 Because of this gap, corporate leaders find few promising innovation-driven companies to acquire. Government agencies in scientifically advanced nations cite this gap as a rationale for allocating taxpayer funds to domestic commercialization efforts.4

Conventional wisdom holds that venture capital can fill this gap. But the venture asset class has come to focus on developing varieties of consumer-oriented digital innovation over short time periods. It’s optimized to support Instagram, not impact. And its investment criteria are very narrow: nothing too long-term, nothing too expensive, and nothing that involves too much technology or market risk. In “What Happened to the Future?”—a manifesto issued by the Founders Fund, a Silicon Valley-based investment firm—the author notes, “In the late 1990s, … venture investing shifted away from funding transformational companies and toward companies that solved incremental problems or even fake problems.… VC has ceased to be the funder of the future, and instead become a funder of features, widgets, irrelevances.”5

Over the past three years, we have explored the role that impact investment by philanthropists can play in funding science. Philanthropists, we have found, are overlooking the middle ground that lies between their grantmaking to universities and their investment in venture funds. This middle ground is precisely where exciting and potentially life-changing technologies can thrive. Instead of focusing on ways to “fix” venture capital, we argue that the philanthropy and impact investment communities can join to create new vehicles that support the creation, translation, and deployment of socially beneficial innovations.

In this article, we outline the parallel histories of science philanthropy and venture investing. That dual history, in our view, has culminated in a bifurcated financial system and has contributed to the idea-to-impact gap. We also propose a solution to that problem: philanthropic investment, or the use of grantmaking to fund early-stage technology ventures that hold the promise of achieving significant impact at a large scale.

The Bifurcation of Science Funding

Why, in our own era, has it become so challenging to fund the commercial development of transformative scientific discoveries? To answer this question, it is useful to observe the history of investment in science for social and economic purposes.

The story of financial support for science research and commercialization in the United States is one of increasing bifurcation. In the beginning, those who conducted scientific work also funded it. In the early 19th century, gentleman scholars like Thomas Jefferson worked at science as they worked at politics, literature, and farming; it was, in short, an important part of being a gentleman. By the middle of the century, however, science had emerged as a matter for specialists. This transformation had implications for funding: Scientists now focused on securing external patronage for their research.6

Foundation support | After 1880, philanthropists began to organize their efforts formally, and they introduced a greater degree of regularity into science funding, particularly by helping to establish the new research-oriented universities that emerged during that period. Philanthropic foundations hired professional staff members to engage with the scientific community, and they commanded the resources necessary to support an increasingly complicated and expensive search for knowledge.7

In the period after World War I, the visibility and prestige of science reached new heights. Foundations invested $100 million in science between the two world wars. Between 1918 and 1925, for example, the General Education Board (established by John D. Rockefeller in 1903) invested $20 million in astronomy, physics, chemistry, and biology. Similarly, the Carnegie Corporation and the Rockefeller Foundation each gave approximately $8 million to the National Research Council, which served as a trade association for science. The council developed markets for PhDs in industry, created communication networks, and encouraged cooperative research projects.8 By 1925, at least a dozen large foundations sponsored research on a large scale.9

In part because of changes in tax policy, charitable donations of all kinds—including donations to support science and engineering—increased steadily throughout the 20th century. In 1955, annual giving from individuals, foundations, and corporations totaled $7.7 billion. By 1998, annual giving had risen to $175 billion.10 Scientific discovery, engineering, and medicine have always received significant funding from individual givers. Today, philanthropic contributions account for almost 30 percent of US universities’ funding for research expenditures.11

Venture capital | In parallel with the expansion of philanthropy to support fundamental discovery in universities, wealthy individuals were pioneering the use of for-profit investment vehicles to fund entrepreneurial start-ups—a practice known today as venture capital.

Consider the case of Venrock, an early-stage venture capital firm that originated as an investment arm of the Rockefeller family. In 1938, members of the family invested in Eastern Air Lines, then headed by CEO (and former World War I flying ace) Eddie Rickenbacker. To make that investment, Laurance Rockefeller, a grandson of Standard Oil magnate John D. Rockefeller and an aviation enthusiast, pooled his money with personal checks from five siblings. In the years that followed, the Rockefeller group backed dozens more early-stage companies, and nearly all of them were science- and engineering-driven enterprises in fields such as aviation (McDonnell Aircraft), imaging (Itek), rocketry (eReaction Motors), analytical instruments (Thermo Electron), and power (United Nuclear). In 1946, the Rockefeller family formalized its ad hoc investing activity into a fund called Rockefeller Brothers Inc.

Other wealthy families followed a similar pattern in their investment activity. In 1911, for example, Carnegie Steel cofounder Henry Phipps formed Bessemer Securities. In the 1930s, the financier John Hay Whitney began investing in high-tech start-ups such as Pioneer Pictures and Technicolor Corporation. These investors were amateurs, but they blazed a trail for the venture capital asset class as a whole.

In the late 1960s, the Rockefellers brought in outside managers to professionalize the firm’s venture investment activity and dubbed the new entity Venrock. These managers continued to invest family money on an “evergreen” basis (that is, by re-investing proceeds with no fixed date of liquidation), and the firm continued to focus on science- and engineering-driven enterprises, both in established industries such as electronics and computing (Intel, Apple, and 3Com) and in other categories marked by rapid technological change—in particular, health care.

In the meantime, a new breed of venture capital partnerships emerged. Partners in these firms didn’t invest their own cash, but rather drew their funding from foundations, trusts, pension funds, and other third-party investors. American Research and Development (ARD), founded in 1946, was the most influential of these firms. ARD alumni founded other East Coast VC firms, among them Greylock, Morgan Holland Ventures, and Fidelity Ventures. Similar operations sprang up on the West Coast—among them Draper and Johnson Investment Company, Sutter Hill Ventures, Kleiner Perkins Caufield and Byers, and Sequoia Capital. What distinguished these newcomers was a financing model that matched the needs of thirdparty capital providers: Instead of developing “evergreen” funds, these firms offered “closed-end” funds. Typically, those funds have a nominal 10-year lifetime that requires portfolio companies to go from initial investment to acquisition or IPO within a decade.

The rise of the Internet in the 1990s saw two changes in the venture asset class. First, the amount of money invested in venture funds grew dramatically, from $8 billion in 1995 to $105 billion in 2000, at the height of the Internet bubble. (More recently, that figure has stabilized at $25 billion to $30 billion per year). Second, the investment focus of VCs shifted toward software and Internet companies that require less capital to scale up and produce faster returns than science-driven companies. In other words, businesses like Groupon, Twitter, and Instagram stole the limelight from businesses like Intel, Genentech, and 3Com.

Inside the Idea-to-Impact Gap

By the early 21st century, the separation of capital along the idea-to-impact continuum was complete. Today, the process of funding science operates within established legal boundaries that delineate how investors interact with nonprofit and for-profit organizations. Nonprofit institutions (including universities) receive grants from government agencies, corporate donations, and private philanthropy to conduct basic science and engineering research. When that research yields ideas (and intellectual property) with commercial potential, for-profit entities step in to license those ideas and to translate them into marketable products. This bifurcated system isn’t equipped to support innovations that have a long time horizon for development.

The energy sector offers a prime example of a technology field that suffers from a lack of early-stage investment. Energy is one of the world’s most important industries, accounting for 10 percent of global GDP. (By comparison, only about 3 percent of global GDP derives from commerce on the Internet.) Yet energy has historically accounted for only 1 percent to 2 percent of venture capital investment. A burst of VC investment entered the energy field in the second half of the 2000s, when fossil-fuel prices soared, but by 2013 investment had plummeted back to historical levels.

When we look back at earlier radical energy innovations that reached broad deployment, we see that the funding sources that enabled their development are essentially gone. Nuclear fission originated with the Manhattan Project, an unprecedented mobilization of public money; no comparable stream of government funding exists today. Photovoltaic cells emerged from AT&T Bell Laboratories, a corporate R&D institution; Bell Labs—and similar entities like Xerox PARC—are now just shadows of their former selves.

Recent efforts to reverse this trend have gone only so far. Since 2009, the US Advanced Research Projects Agency-Energy (ARPA-E) has spent more than $800 million to fund more than 350 breakthrough energy technology projects. ARPA-E focuses its grantmaking explicitly on projects with commercial potential. Even so, only a handful of its awardees have been able to raise institutional risk capital to supplement their ARPA-E funding.

Most explanations of the science funding gap fail to recognize that the shortfall has two causes: First, compared with software investments, many science-driven investments have a relatively unappealing risk-return profile. Second, and equally important, the financial interests of investors who participate in the innovation process are often not in alignment with the social goals of scientist-entrepreneurs. One venture capitalist, speaking in 2013 at an American Academy of Arts and Sciences roundtable on energy finance, put it this way: “I will not invest because of climate change. My limited partners expect financial returns within a certain timeframe.”

For-profit investment vehicles for early-stage companies fail to account for investors’ charitable objectives or the potential social returns of such innovations. Conversely, tax-shielded charitable funds are rarely used to support for-profit technology companies, even when those companies advance desirable social outcomes. In each case, neither purely philanthropic motives nor purely profit-based motives are sufficient to justify investment. As a result, capital to build companies in areas such as energy, water, and health care remains in short supply.

A New Role for Philanthropy

We believe that a solution to this problem lies in the emergence of a new breed of philanthropic investors—individuals and institutions that aim to bridge the divisions that mark the funding of science today.

Consider the Bill & Melinda Gates Foundation. Over the past half-decade, the Gates Foundation has deployed a considerable amount of capital to bridge the idea-to-impact gap within the health-care field. In 2011, for example, the foundation made a $10 million equity investment in Liquidia Technologies, a for-profit venture that develops and commercializes vaccines that prevent infectious diseases. The foundation made this transaction as a program-related investment (PRI); for financial and legal purposes, therefore, it counts as a grant. And in 2013, the foundation made a PRI in the Global Health Investment Fund (GHIF), a traditionally structured venture fund that supports medical research and development. That PRI took the form of a loan guarantee that allowed investors in GHIF to hedge as much as 60 percent of their invested capital, and it helped GHIF raise $108 million.

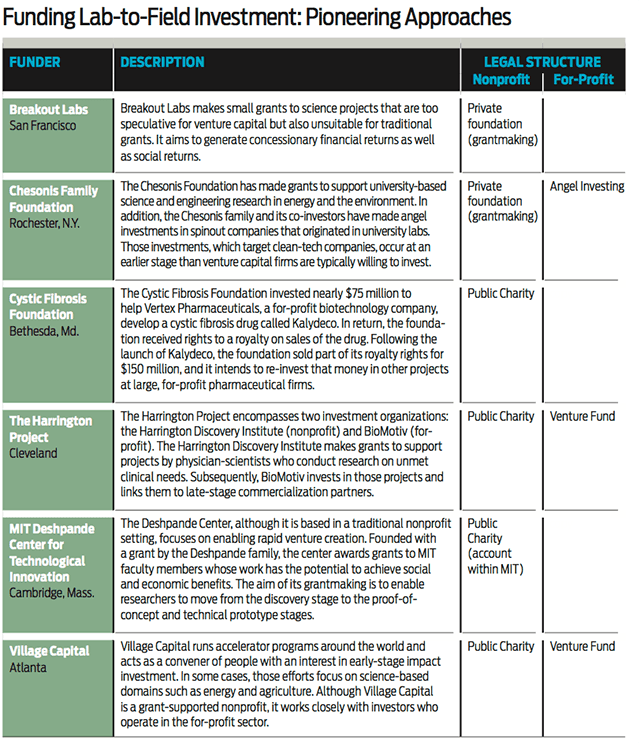

Following the lead of the Gates Foundation and other pioneering philanthropists, we advocate a model that occupies the space between research grants and for-profit risk capital. Of particular interest to us are impact investment approaches that blend philanthropic and financial perspectives. A handful of organizations are already blazing trails at the boundary between nonprofit and for-profit investment in science and engineering, and they are pursuing a wide variety of methods. (See “Funding Lab-to-Field Innovation: Pioneering Approaches” below.)

The model that we propose will be compelling to a wide range of philanthropic asset owners. Here, we will focus on charitable foundations. The US Internal Revenue Code requires each foundation to spend at least 5 percent of its assets annually on efforts to further one or more charitable purposes. (The advancement of science counts as one such purpose.) To fulfill the 5 percent mandate, foundations historically have made grants to public charities without an expectation of receiving a financial return. In 2011, grant disbursements from foundations totaled $47 billion.12

Today, however, foundations are increasingly forging impact investment strategies that involve deploying assets on both sides of their house—on the 5 percent side, where grantmaking takes place, and on the 95 percent side, where endowment managers work to preserve foundation capital.

On the endowment side, foundation leaders have begun to apply positive and negative screens to the investments they make. A recently launched movement called Divest-Invest Philanthropy, for example, highlights the power of large foundation endowments to shape social outcomes.13 Citing both ethical and financial reasons, the movement calls on foundations to divest their endowments of holdings in fossil-fuel companies. To date, the dialogue around this movement has focused on avoiding harmful investment activities (“divest”). But no less important, in our view, is the need to support helpful activities (“invest”).

The use of direct investment—often called Mission-Related Investments (MRI)—allows foundations to put the full weight of their assets toward the pursuit of philanthropic goals. (In 2011, the endowments of US foundations were collectively worth an estimated $600 billion.) With an MRI, a foundation uses endowment funds to support a business whose products or services align with the foundation’s mission. As a rule, MRIs promise a market-rate return and therefore meet “prudent investor” requirements. Endowment managers have a fiduciary duty to preserve capital over time, and the US tax code mandates that they refrain from making high-risk investments that might jeopardize the longevity of their foundation. As we have noted, however, many early-stage ventures in science and engineering cannot meet that standard. MRIs offer one tool for philanthropic investors to deploy, but they will not be sufficient to fill the idea-to-impact gap.

The Promise of Program-Related Investments

There is another side of impact investing that has greater potential to close the idea-to-impact gap in science and engineering. By its nature, that gap can be filled only by concessionary investment—by vehicles in which investors concede, or give up, something that they would otherwise expect in return for their money.14

Foundations can make such investments in the form of a PRI. With a PRI, a foundation channels grant funds (that is, money that comes from the “5 percent” side of its operations) to a for-profit company that does “program-related” work. Such work is program-related insofar as it advances a programmatic goal of the foundation. The US tax code requires a PRI to meet a two-part test: The investment must “significantly further” the charitable goals of a foundation, and it must be such that the foundation would not have made it “except for [its] relationship” to those goals.15

The concessionary nature of a PRI is not based solely on the magnitude of expected returns. A PRI-making foundation can make concessions according to various investment criteria—the timeline for drawing financial returns, for example, or the perceived market, technology, or regulatory risk of the investment in question. Although it has become the norm to structure a PRI as low-interest debt, doing so is not a requirement. In any event, the value proposition for philanthropists is clear: Making a grant in the form of a PRI gives a foundation a powerful tool for moving critical ideas out of the laboratory and into the commercial marketplace. Even though PRIs come out of grant coffers, they offer a foundation the possibility that it will recoup money that it can redistribute to other charitable causes.

Given this compelling proposition for grantmakers, it is surprising that the use of PRIs to bridge the idea-to-impact gap is not more common. According to the best available data, foundations made fewer than 5,000 PRIs between 1998 and 2010, and together those investments constituted less than 2 percent of total grantmaking. Among those PRIs, less than 1 percent—about 35 in all—went to grantees in science and engineering fields.16 Although few in number, most of those PRIs went to support technology as it moved from a lab environment to commercial development. These data lead us to two conclusions: First, PRIs do have the potential to bridge the idea-to-impact gap in science and engineering innovation. And second, there are high barriers that prevent asset holders from using PRIs in this way today.

Some of those barriers are philosophical. Many philanthropists express concern that PRI-making might cross well-defined boundaries and violate important institutional norms. Is it inappropriate to direct grant dollars away from traditional public charities and toward profit-seeking businesses? How can philanthropists and investors ensure that PRIs do not duplicate traditional, finance-first investment activities?

In addition, our research suggests that these barriers arise because of the historic separation of the social logic of philanthropy from the economic logic of endowment management. These two areas of practice are organizationally distinct within private foundations: The grantmaking side of a foundation aims to advance a charitable mission by funding programs, whereas the endowment side strives to preserve a corpus of assets. People on each side of the divide have their own affinity groups, their own governing bodies, and their own best practices.

Three barriers related to that separation are worth noting.

Mismatch of expertise | PRIs, by construction, require the expertise of both grantmakers and for-profit investors. But these groups do not have a common language or a common body of expertise. Sourcing deals, conducting due diligence, structuring investment terms, and making board-level strategic decisions for technology start-ups are not activities that grantmakers are trained to do. Money managers, for their part, have little expertise in analyzing the social impact of an investment or the concessionary nature of a financial vehicle. On the contrary, they are trained to focus on financial returns and to follow prudent investing practices.

Legal uncertainty | Another formidable barrier—one that is grounded both in regulatory reality and in the risk-averse culture of the legal community—involves the legal consequences of accepting investment risk. Attorneys are systemically inclined to discourage PRI-making in order to protect their clients, and few attorneys today have experience in advising clients on transactions of this kind.

Policy-driven inertia | Many foundation administrators shy away from making grants to recipients other than public charities. After the Tax Reform Act of 1969, which tightened the tax rules that apply to the philanthropic sector, US foundations began to avoid risktaking behavior and settled into a routine in which the easiest grant to make is a general-purpose grant to a public charity.17

Given the urgent nature of global problems like climate change, water scarcity, and poverty—and given the need for science- and technology-based solutions to those problems—we believe that taking action to break down these barriers is imperative.

An Agenda for Philanthropic Investment

The idea-to-impact gap should matter a great deal to the individuals, families, corporations, and foundations that have already invested in science, engineering, and medicine. It should matter to any investor who yearns for real-world results. And it should matter to the billions of people affected by a lack of electricity, an absence of clean water, a changing climate, an inefficient manufacturing sector, and the persistence of diseases like cancer and dementia.

As scientists, funders, and other stakeholders explore various forms of philanthropic investment, some parts of their journey will be straightforward. Within the university-philanthropy complex, structures already exist to find good ideas in university labs, to create entrepreneurial start-ups, and to partner with government agencies and large corporations in supporting those young companies.

But the work of expanding access to much-needed risk capital will be more complex. That is where pioneering needs to happen. Our hope is that leaders will emerge who have the courage to explore this new territory where impact investing overlaps with funding for science. Here, we offer an initial agenda for those leaders to follow.

- Entrepreneurs need to educate themselves about the decision-making processes and legal constraints that are unique to philanthropic asset owners. Appealing to that group of funders requires a different approach from the one that they use in pitching to traditional venture capital firms.

- Asset owners need to collaborate with each other in order to aggregate funds at a sufficient scale. Collaboration at this level is especially crucial in domains that have certain common elements: large charitable goals, a misalignment with the structure of traditional venture capital, and the potential for market adoption of commercial products. PRIME Coalition, an entity that we are helping to lead, is one such effort. It is a network of philanthropists who share an interest in market-based solutions to climate change. That model, we believe, holds promise not only in the climate field, but also in other areas that depend on advances in science and engineering.

- Scholars need to refine the vocabulary of impact investment so that investors and other stakeholders can untangle the various policy, tax, and accounting issues that affect this emerging field.18

- Investment managers need to be willing to move from one compensation structure (in which they receive management fees and carried interest) to another (in which they receive budget-based salaries and impact-based bonuses). Likewise, grantmakers need to be willing to pay top salaries for high-quality talent.

- Impact investment intermediaries need to acknowledge the importance of science and engineering. They need to build impact measurement regimes around projects that fall between the traditional categories of charity and investment. And they need to expand their focus from the deployment of proven technologies to the development of technologies that are unproven but highly promising.

In 2013, Sir Ronald Cohen and William A. Sahlman put forth a striking claim: “Social Impact Investing Will Be the New Venture Capital.” They called on impact investors to find the same courage that the early institutional backers of the venture capital industry displayed, and they offered a vision of how investors could enable progress on social issues while also delivering financial returns.19 Our proposal is a concrete response to that broad agenda. Also in 2013, Peter Buffett issued a bold call to his fellow philanthropists. He urged them to “[try] out concepts that shatter current structures and systems.”20 Although Buffett made no mention of science and engineering innovation, we believe that building a philanthropic bridge between the ivory tower and traditional capital markets would meet the standard that he set. In that spirit, we encourage philanthropists of all stripes to pioneer new forms of philanthropic investment—new approaches that support the kind of innovation that the world desperately needs.

Read more stories by Fiona Murray, Matthew Nordan & Sarah Kearney.