It’s well known that people living in poverty often lack access to safe, reliable ways to manage what little money they have. As a result, they face de facto exclusion from the financial system that the rest of us rely on.

Government reports by the Federal Deposit Insurance Corporation say that 8 percent of all US households do not have savings or checking accounts—that’s roughly 19 million Americans. Many workers cash paychecks, pay the rent, and put whatever they have left over in their pockets. Because they don’t save, they have little financial cushion if they face illnesses or other unexpected expenditures. Some give up minimum-wage jobs simply because they need their car to get to work, and they can’t afford repairs. This is particularly true in rural areas. The need for financial inclusion is clear, not just in the United States, but around the world.

Influencers worldwide, such as US Senator Elizabeth Warren, have started thinking about the issue in new ways. Warren’s support for the idea that post offices around the country offer check cashing, bill payment, and other financial services is just one example. Increasing the accessibility of services minimizes barriers that prevent the unbanked from using traditional savings methods.

Recently, we led an unusual philanthropic project called Gateway Financial Innovations for Savings (GAFIS). The four-year project (funded by the Bill & Melinda Gates Foundation, sponsored by Rockefeller Philanthropy Advisors, and managed by consulting firm Bankable Frontier Associates) worked with five leading banks in developing countries to help design and deliver new, inclusive savings products. The approach was straightforward: Research and implement new approaches to providing poor people with the financial tools they deserve. This philanthropic-public-private collaboration focused on sustainable financial inclusion—developing savings accounts that could accommodate the needs of the “unbanked” while also delivering a return that allowed banks to continue service. Collectively, the five banks (Bancolombia in Colombia, Bansefi in Mexico, Equity Bank of Kenya, ICICI Bank in India, and Standard Bank of South Africa) hold more than $250 billion in assets and serve more than 75 million customers.

The project lies at the intersection of two major disruptions gathering force in the global economy. First, the income gap between the rich and poor is widening. According to a recent estimate, less than 1 percent of the world’s population holds 41 percent of all wealth. Second, potent technological advances such as the widespread use of mobile phones and the drop in price point for such devices, indicate that the future of banking could revolve around cost-effective mobile applications. As telecommunications companies and banks compete to deliver financial services, these new platforms may capture a formally ignored market like the poor, specifically those living below the poverty line. Mobile applications create a simpler way to access bank accounts and make transactions in a faster, more convenient manner.

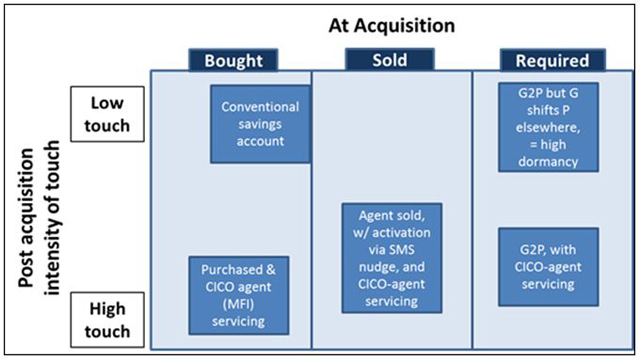

With traditional mass-market savings accounts, banks have given very little consideration to consumer engagement with previously unbanked clients after they open an account. This is, in large part, because it is difficult to contact unbanked clients in the mass-market segment—addresses are often inaccurate (and many clients don’t have one) and costs are high. The effect is that roughly half of basic bank accounts lie dormant.

Today, most poor people (90 percent of bank clients in GAFIS surveys in South Africa, Colombia, and Kenya) have access to a mobile phone with SMS messaging. As a result, some banks are using SMS messages and on-the-ground agents to catalyze initial deposits and build trust by confirming amounts (see below). The program’s bank partners realized that they needed to offer services that were accessible from traditional, basic cell phones in addition to smartphones.

Banks are using different touch points and methods to build trust with consumers. (Image courtesy of GAFIS Project Report, December 2013)

Banks are using different touch points and methods to build trust with consumers. (Image courtesy of GAFIS Project Report, December 2013)

Moreover, many mobile banking products are more additive in nature—that is, they supplement other banking channels such as ATMs, computer-accessed online banking, and conventional branches. In contrast, in many of the countries GAFIS studied, mobile banking is the primary channel or device and is intended for use in conjunction with bank agents. In many instances, there is no practical alternative: Conventional branches and ATMS are simply too far or too costly to visit, and many of these consumers do not have regular, reliable computer access. As a result, these mobile solutions have transformed the way low-income consumers save by providing them with primary access to banks.

The GAFIS banks now have a collective 25,000 agents working on the ground, compared to just 2,600 in 2010. In total, people opened more than four million new GAFIS-linked accounts over the course of program (2010-2013) and 900,000 of those demonstrated savings behavior. As a result of the combined effort of the five GAFIS banks, many new savers are active users. In the last year of the project, the number of inactive accounts has gone down by about a third. If this trend continues, it would suggest these innovations have the capacity to make lasting change.

Through GAFIS, we’ve learned that relatively small grants (less than $1 million per bank) can unlock resources from banks to support inclusion. Our work indicates that the use of SMS messaging and on-the-ground agents are transferable to poor communities around the world, and that these services financially viable for banks.

We hope that this project can serve as the foundation for donors and financial institutions, in the United States and other countries, to help low-income populations around them. For philanthropists, financial inclusion holds the promise of harnessing the power of the private sector and technology to help achieve social ends. It is both a business opportunity and a way to buffer inequality by bringing the reliability of low-cost, secure financial tools to people who have never had access to them. Philanthropic efforts to support financial inclusion can create more than bank accounts, and collaborations in this field can develop what should be a common right of humanity: the ability to participate in the economy using all financial tools available and do what most people do on a daily basis—manage their money for a better life.

Read more stories by Chris Page & David Porteous.