Every Wednesday at 8:30 am, the Big Society Capital investment committee gathers in our boardroom in London. Team members introduce each potential investment, presenting detailed financial modelling, a market assessment, a plan for measuring impact, and a summary of what our partners and stakeholders think. Despite this rich information, however, some questions remain unanswered, such as whether an investment that benefits more affluent people is worthwhile, or whether we want to back an organization that could achieve great social benefit but seems motivated primarily by financial gain.

In fact, analysis cannot answer these questions, because they are fundamentally about values and ethics. But we impact investors are often more comfortable talking about finance and systems than about values. In mid-July, more than 500 people from more than 40 countries gathered in Chicago for the Global Steering Group Impact Investment Summit. The energy and commitment were palpable, and my fellow delegates and I were inspired by extraordinary stories of the social change that impact investing can deliver. Sessions delved into topics such as financial models, system design, working with government, and influencing corporations. But attendees devoted much less time and intellectual effort to the ethics underpinning our work.

Philosophers have been wrestling with ways of thinking about values for thousands of years. I believe that this legacy of rigorous thought can help draw out and resolve some of tensions that underlie the difficult conversations we have in those Wednesday morning meetings.

Two of the longest-standing debates in ethics have direct relevance to impact investing. The first is the debate over the relative value of outcomes and purpose. Is the priority achieving the most good, or is it acting according to a good purpose? Both approaches have a long heritage in Western philosophy, and both also accord with common feelings about morality. Most people would agree, for example, that it would be better to give money to a charity that has clear evidence of its effectiveness than a charity that doesn’t, as the outcome of our giving matters as well as the act itself. But most would also agree that there is something more worthwhile about making someone better off through a conscious donation as opposed to that person finding some money we accidentally lost in the street.

Impact investing currently tries to straddle the importance of outcomes and purpose. Two of the main mantras for impact investors are “outcome measurement” and “intentionality.” We say it is very important to measure and prove outcomes; we also say the investor and investee should intend to achieve good things. But in practice these desires pull in different directions. For example, exacting measurement standards might be daunting for people with good intentions. Some of our impact investments are in small start-up enterprises, with highly motivated entrepreneurs. We are conscious that demanding detailed outcome measurement not only risks creating bureaucracy that distracts these enterprises from their mission, but also sends an (unintended) signal that we don’t trust their intentions. On the other hand, if we rely solely on the good intentions of the founders, how do we ensure the preservation of positive impact as an organization matures and potentially broadens or changes its leadership?

One way some impact investors like Big Society Capital try to solve the conflict is by asserting that aligning the intentions of investor and investee will necessarily result in good outcomes. However, that risks ducking the issue; it is clearly possible to create large amounts of social good through investments that have no intention beyond making money. Investing in successful pharmaceutical development is a good example. Most would agree this shouldn’t be considered impact investment—but why not?

One argument is that commercial investors will back viable companies that have no particular positive intention, so there is no role for impact funds. However, this view breaks down in a case where the company’s product has great potential for social good, even if that is not its primary intention and where the commercial case for the social use is poor, such as a pharmaceutical with an alternative use in developing countries. Investing only where there is intention to do good would rule out this kind of opportunity for impact. Alternatively, one could argue that in such cases the impact is “accidental,” and without the added element of good intentions there is little assurance that the investee will maintain its positive impact over time.

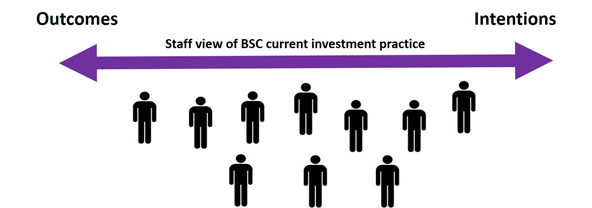

In practice, impact investors generally need to balance the importance of intention and outcomes. I asked staff at Big Society Capital to position our current investment practice along a spectrum from total focus on outcomes to total focus on intention: there was a very wide distribution with the mean roughly in the middle (see below).

The second debate concerns what are sometimes called “realist” and “anti-realist” ethics. Essentially, the realist position holds that ethical judgements reflect an objective reality (such as “murder is absolutely wrong”). The anti-realist view is that such judgements are statements of personal taste (“I find murder abhorrent”). Such a debate is particularly important for an organization like mine, which is attempting to build a market and infrastructure for impact investment. If we take an anti-realist view, then our role is to build a market that allows anyone to invest for impact according to their own definition of what impact is. The systems and funds we put in place would be neutral to actual outcomes. By contrast, if we adopt a realist view, we would set things up to drive investment toward particular kinds of benefit we hold are good.

To give a practical example: Big Society Capital has established a facility to underwrite the issuance of charity bonds in the United Kingdom. Any charity can issue bonds across a huge range of potential social impacts. We have had difficult conversations about what boundaries we should draw in our support for this market. Do we say that some potential benefits are not legitimate and so not eligible for our support? If we do, we need a justifiable account of the ethical principles that underpin such a judgement. If we do not, we are potentially supporting causes that many people, both internally and externally, will feel have limited social value.

All impact investment organizations make judgements all the time—whether something counts as impact, how to think about measurement, and so on. Many of these questions are not technical. Tensions arise and judgements feel tricky precisely because tools and systems do not get to the heart of the problem; these points ultimately connect to ethics and values. We should acknowledge that, be honest with each other when values come into play, and consider why that makes some discussions challenging. We can use the tools that philosophers have honed over the centuries to help us reach clarity and make the right decisions—whatever “right” might mean.

Read more stories by Stephen Muers.