As the White House convened a roundtable on impact investing last month, 20 corporations pledged to deploy $1.5 billion across the United States in the next six years. That’s almost the same amount of capital investors have put into impact enterprises in India cumulatively over the last 14 years. Globally, too, estimates of per annum impact investments stand in the ballpark of $10.6 billion.

While the Indian numbers may seem relatively low, they are a big step in the right direction for a country whose impact entrepreneurs have received widespread international interest for the replicability of their innovations across emerging markets.

From a trickle of $1.17 million in 2000 to investments of about $250 million per annum since 2011, there has been a major uptick in investments, taking the total to $1.6 billion spread over 220 for-profit impact enterprises.

The India story, therefore, is not about the quantum of impact investments, but about the evolution of the sector and the role of impact capital. Over 50 percent of the impact enterprises tracked in a study by Intellecap have taken off only post-2010. Access to capital remains their biggest challenge, and impact investors have emerged as an important source of finance for these enterprises. Since the emergence of the first Indian and foreign impact funds (such as Aavishkaar and Acumen) in the early 2000s, more than 50 impact funds have emerged. These investors have taken an interesting approach akin to venture capital, and the results have paved the way for mainstream capital in impact enterprises.

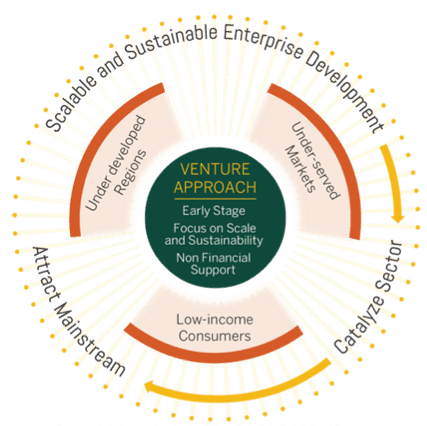

Dominant Investing Approach in India

Interestingly, the past few years have seen a greater consensus among impact investors in India on their investment approach. They emulate the approach of mainstream venture capital firms but extend it to investing in impact enterprises. This venture approach involves making investments at an early stage in for-profit enterprises that operate in underserved markets and critical needs sectors. It is characterized by:

- Early-stage investing and pioneer risk: 33 percent of all investment deals in impact enterprises since 2000 were at the seed stage, often in unproven business models, difficult geographies, or new markets.

- Scale and sustainability: 30 percent of enterprises with first-round funding received before 2011 have received at least two rounds of follow-on investments validating the investor’s faith in the firm’s scalability and financial viability.

- Non-financial support: Additional support for impact enterprises includes technical assistance facilities, capacity building, customer education, and driving behavior change.

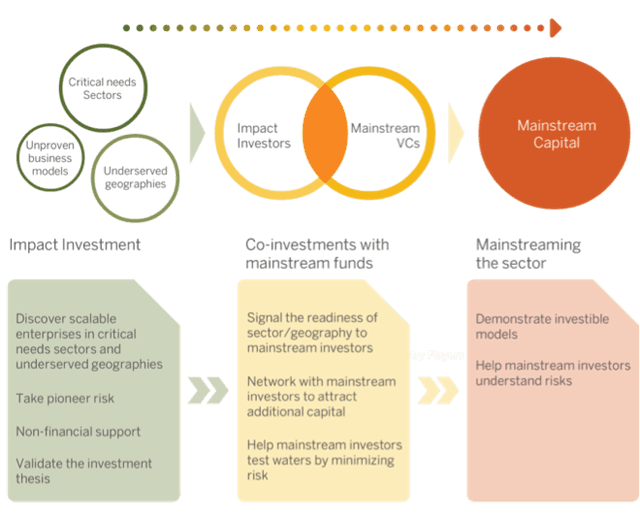

The Catalytic Role of Impact Capital

Impact investors are taking a venture capital approach by going beyond financial support to catalyze growth. (Illustration courtesy of Intellecap Analysis)

Impact investors are taking a venture capital approach by going beyond financial support to catalyze growth. (Illustration courtesy of Intellecap Analysis)

Impact investors in India play an important role in demystifying the business model risks of impact enterprises for mainstream investors. They signal enterprise and sector “investibility” through co-investments before fully exiting from them.

We think of the catalytic role played by impact funds as a three-phase process. Consider, for instance, microfinance institutions (MFIs), which were first off the block in the impact investing space. In the early 2000s, most first-round investments, with a few exceptions, were made by development finance institutions and MFI-focused impact funds that were willing to take significant risks in unproven business models. In recent years, however, a few mainstream venture capital and private equity investors have made sizable investments in the larger MFIs, indicating a greater understanding and acceptance of these business models. The MFI sector has been able to attract more than $458 million in cumulative investments from mainstream investors across all rounds over the past 14 years. Of this amount, mainstream investors invested around $225 million in follow-on investments in deal rounds that did not involve any impact investors.

(Illustration courtesy of Intellecap Analysis)

(Illustration courtesy of Intellecap Analysis)

Other impact sectors have yet to catch up with microfinance, having collectively raised only $449 million in mainstream capital since 2000. The financial inclusion and health care sectors have seen deals that involved sizable amounts of capital from mainstream investors. Through these deals, impact funds in India have been able to demonstrate an ability to catalyze infusion of mainstream capital.

The road ahead for impact investing in India, however, is not completely smooth. Some important challenges include the fact that domestic capital remains elusive; most impact capital is foreign. Also, with just 15 documented exits, the sector continues to grapple with investments in long gestation projects that are slow to scale. The sharp focus of most impact funds in India on scalable business models means that there is still a huge gap in availability of capital for impact enterprises that can create deep impact but may not be highly scalable. Bridging this gap through a new set of investors who are focused on taking pioneer risks and designing alternate financing structures to just equity financing will be critical to seeing these models succeed and achieve financial sustainability.

Read more stories by Nisha Dutt & Usha Ganesh.