(Illustration by Julianna Brion)

(Illustration by Julianna Brion)

Nonprofit leaders routinely confront the challenge of maintaining financial sustainability and doing more to serve their missions in an ever-changing world. We judge their performance according to their formal and fiduciary duties, as well as by the values they adopt in their governance. We expect leaders to create and implement strategies that achieve or maximize the values they embrace. To do so, they must make the best use of the capacities and resources at their disposal.

In the private sector, profitability tends to top the list of values. Corporations enshrine a return on equity—to maximize present value of shareholders’ holdings. We can subject nonprofit performance to a similar test: How does a nonprofit use its capacity and resources to do more and to do better in achieving or maximizing what it values?

This question has confronted me over decades of work with dozens of nonprofits as a founder and board president in volunteer roles; as an executive and program leader on nonprofit staffs; and as a consultant, management educator, and researcher in nonprofit strategic management. In what follows, I apply that experience, along with insights from research studies of nonprofits, to argue for the concept of the “invisible balance sheet” as a structure for helping nonprofit leaders to recognize, evaluate, and effectively pursue their values.

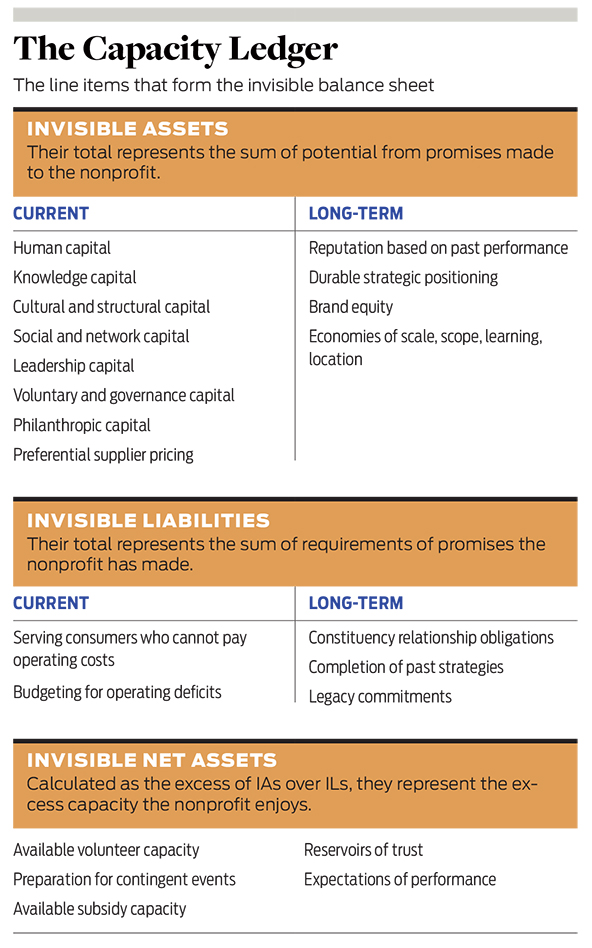

The invisible balance sheet works analogously to the financial balance sheet and other accountability structures, with their assets, liabilities, and net assets. Invisible assets are resources promised to an organization that potentially add value by helping it accomplish its mission. Invisible liabilities are the obligations that nonprofits take on that go beyond formal contracts with counterparties. An excess of invisible assets over invisible liabilities generates invisible net assets, representing free capacity or potential that nonprofits may be able to deploy. The invisible balance sheet helps nonprofit leaders and board members by boosting their ability to evaluate capacity during strategic planning and in ongoing governance. It can help leaders navigate their organizations in these times of financial and social turbulence.

Nonprofit Capacity

When we refer to nonprofit capacity, we can mean many different things. Some capacities are financial and physical. Nonprofits recognize and evaluate such capacities on audited financial statements, Form 990s, and regulatory reports. Conveniently, they are denominated in dollars and/or have physical presence and a documented contractual past. Moreover, many accounting conventions, financial statements, regulatory requirements, and other fiduciary structures are designed around those capacities.

These same structures also recognize the commitments that nonprofits make to acquire those assets and capacities. Collectively, the assets (liquid or not, short-term or other) are counterbalanced by obligations—i.e., liabilities—that are recognized through contracts, and likewise have various terms. Total assets minus total liabilities equal the net worth or owner’s equity in the proprietary firm, and net assets in the nonprofit enterprise. This is Nonprofit Accounting 101.

Of course, nonprofit leaders do not limit their view of capacity to what is on the balance sheet. Other capacities and potentials loom large in their thinking, principally their people (staff and volunteers) and their relationships with funders, donors, and other supporters. They may recognize the strengths in their internal systems, the loyalty they have generated, their relationships, or their location as capacity to use in support of mission.

To get a better sense of these strengths, consider some examples near (and dear) to me. The Bach Choir of Bethlehem, Pennsylvania, maintains a strong musical reputation with its annual Bethlehem Bach Festival. The main festival concerts have been held in Lehigh University’s Packer Memorial Church since 1912; the bonds joining the choir, the university, and the choir’s audiences are among the longest-lasting in American performing arts. A few blocks away, the multifaceted arts and culture nonprofit ArtsQuest offers year-round streams of performing-arts events with the architecturally lit blast furnaces of Bethlehem Steel as a backdrop, and through other districts of the city in seasonal festivals; its centerpiece is the annual Musikfest, attracting a million visitors every year. Thirty miles to the south, the Philadelphia Folksong Society has rented the same rural farm in Montgomery County from the same family since the 1960s to present the Philadelphia Folk Festival.

In all three cases, access to the sites has lasted over decades and survived COVID-19 interruptions and changes in the leadership of the nonprofits and their institutional and family hosts. Continued access to a venue reduces uncertainty for the nonprofits, while audiences benefit from familiarity with favored locations. Because the nonprofits do not own the sites, their enduring availability depends on continuing personal, family, institutional, civic, corporate, and community ties with counterparts who expect the nonprofits to deliver successful programs. To keep those ties up over successive generations of nonprofit leadership requires nurturing and monitoring. It demands capacity-building.

The point of capacity-building practices in training and organizational development is, in part, to help nonprofits use such resources most effectively. When participants break down a nonprofit’s strengths, weaknesses, opportunities, and threats in a SWOT analysis, such capacities, unseen but still real, typically appear in the strength quadrant.

Nonprofits also make promises, and nonprofit leaders assume responsibility for fulfilling them. Many nonprofits offer services for which users cannot pay the costs of delivery. Nonprofits issue vision statements that aspire to better worlds, commit to challenging theories of change as part of their mission, and measure whether they are making meaningful impacts. Consider the arts again: Economists William Baumol and William Bowen argued in 1966 that the performing arts were certain to incur operating deficits as costs mounted, and would systemically require subsidies.1 The truth of that argument does not stop 21st-century arts managers from promising and delivering dynamic seasons of great performance, because they have strong expectations that those subsidies will still be forthcoming. Outside the arts, nonprofits in human services commit to addressing the needs of vulnerable populations, with the same anticipation of support.

We can think of nonprofits as settings of trust and promises. The promises are omnidirectional (internal and external), multilateral (supplier, customer, competitor, donor, volunteer, beneficiary, payer), interpersonal, and institutional. Nonprofits both issue and receive promises. Some of them (but not all) are covered under employment law or the Uniform Commercial Code. Some are promises and potential that are itemized in annual reports and SWOT analyses. Some may appear in the footnotes of financial statements but not on the formal balance sheet or statement of financial position.

Even in stable times, human capital of all kinds—staff, volunteer, donor—can be viewed as a resource that needs constant nurturing, if only to prevent erosion.

The invisible balance sheet is a framework for examining those elusive, invisible capacities and the obligations that nonprofits undertake to attract them. In many cases, nonprofit leaders can use similar insights and assessments to those applied to a financial balance sheet or statement of financial position, to recognize a balance sheet that is not seen but is still consequential to governance. Roughly, the invisible-balance-sheet model envisions some capacities as invisible assets (IA) that have been promised to nonprofits, attracted by the commitments and service obligations the nonprofits make to address society’s needs. Nonprofits, like all entities, make promises about what they will accomplish. The promises to perform, to provide the social and public benefits that nonprofit leaders embrace, are invisible liabilities (IL).

“Embrace” is the operative term here, emerging from the realm of strongest voluntary determination, more than from the statutory realm of enforceable contracts. Liabilities are commitments of economic resources. Contractually, nonprofits, like other enterprises, commit to discharging liability via formal contracts for trade payables, debt instruments, and the like. Aspiring to perform and deliver mission-driven results, they commit additional visible (financial) and intangible and invisible resources to fulfilling the promises they willingly make (i.e., they embrace them)—promises that rely on subsidies and support. As they discharge their ILs by fulfilling the obligation, they systemically facilitate the continued availability of subsidies.

The presence of both IAs and ILs implies invisible net assets (INAs)—the free capacity or potential that nonprofit leaders may be able to deploy. As I will describe, nonprofits often make decisions that could (or should) be based on their understanding of their invisible assets, invisible liabilities, and, for strategic decisions, their invisible net assets.

To be clear, the invisible balance sheet offers merely an analogy for the nonprofit statement of financial position or balance sheet, not an equivalence. Its items do not pretend to conform to Financial Accounting Standards Board (FASB) standards, and their market worth can’t be measured in currency. But they comport with the well-known model in financial economics that sees firms at their root not as individuals but as nexuses of contracting relationships.2 In fact, many of the highest-valued assets and most profound obligations may not be legally contracted but are promised with as deep an intent to fulfill them as a written contract might stipulate. And that prominent feature of the sector, the willingness to deliver expected services and expected qualities, is possible only with promises. Boards can attend to this as they weigh strategic plans and action; executive directors and leaders should also be attentive to the presence of these assets and liabilities in the short run.

One element of the invisible balance sheet that does carry over from the statement of financial position is the notion of balance in the “accounting identity,” in which assets are defined as the sum of liabilities and net assets. Symmetrically, invisible assets are financed or counterbalanced by invisible liabilities and invisible net assets. In other words, some IAs are secured by the commitments nonprofits make to accomplish their mission in various ways, and some are present in the INAs as capacity available as a reserve or for growth. Let us turn to these invisible assets, liabilities, and net assets and review some helpful examples and approaches to measurement.

Invisible Assets

An asset is a thing of value to which the owner can claim title or ownership on the basis of past action, and from which the owner can derive future benefit. Its “value” derives from future economic benefits it may convey. Accounting practice already recognizes that some assets are intangible, but while “invisible” and “intangible” assets share qualities, they require different analytics. Intangible assets are valued on the balance sheet at cost or market, informed by an observable relationship with past or expected transactions. Firms put intangible assets on their balance sheets in relation to earnings they are expected to achieve, as in the case of oil-company reserves, or they mark them to market against other, similar transactions for assets of that type, such as intellectual property.

Analogously, an IA is a resource, promised to an organization at a point in time, that potentially adds value related to accomplishing mission. Here, “promised to” substitutes for the “ownership” quality of the relationship between an organization and its assets; the nature and degree of ownership stem from promise and trust, not formal contract. The extent of control reflects the confidence and trust between the parties who made commitments. The “point in time” is significant because it views IAs as stocks, rather than flows. However, IAs diverge from intangible assets because they lack available market price signals for valuation, so assessing their worth needs alternative metrics.

As in a balance sheet, some IAs have short- and moderate-length terms, while others may be more durable. Consistent with the nonprofit sector’s concentration in service activities, various forms of human capital constitute the principal IAs. Some are internal to the nonprofit, in the form of specialized knowledge in the workforce, be it paid or voluntary. The internal culture of nonprofits can be an asset. Leadership can be an asset. These capacities are present in all organizations, and the values they can offer are widely written about. Recognizing them as IAs does not automatically confer a high value on them, as leaders or other human capital can also exhibit comparatively low value.

Recognizing IAs as useful resources only starts the analytic process; their relevance as assets derives from their net efficacy—i.e., what they deliver and what they require for maintenance. Human-capital assets are time limited to planning horizons that are as long as the leaders, skilled workers, and beneficial culture persist. Ideally, great leaders guide superb workers in joyous collaboration and service, over long periods of time. But the opposite can also happen: Knowledge bases can be slight and of low relevance; leaders can falter; cultures can decline. Because workforce, leadership, structure, and culture are among the characteristics that executives can influence, they are value-adding characteristics for governing boards to observe and monitor.

Much nonprofit human capital takes the form of volunteer support. The willing donation of one’s time to serve in an organization setting is a vital promise that nonprofits receive and rely on. Practically all charitable nonprofits use some volunteer labor, if only on their boards. For some, it is mission critical; the underlying business models of Big Brothers Big Sisters of America, Meals on Wheels, community arts and athletic organizations, and others are based on volunteer labor. Volunteer availability is a complex matrix of demographics, labor market, and community factors. Skilled volunteers provide a capacity available to fulfill mission, so these nonprofits cultivate and manage volunteer pools to promote retention.

External relationships between a nonprofit and other entities should also be viewed as assets. Consider individual donors and institutional funders as sources of philanthropic support for either operations or capital. Their formal annual pledges and future grants awards appear in audited statements as receivables. But there are frequently implicit expectations of longer-term support, prompting development departments to engage in cultivation activities. The cost of those activities is the cost of maintaining the value of the donor pool.

Nonprofit mission statements emerge from the voluntary willingness of organizational leaders to improve the world in some fashion, independent of reward or legal mandate.

Capacity and potential from relationship-based promises have their own life cycles and may grow or decline over time. This pattern differentiates them from other real assets, which tend to depreciate relative to original book value. When nonprofits see growth in their donor population or volunteer pool or an improved staff culture, they are experiencing higher values of their invisible human-capital assets. But those same resources can decline in availability or efficacy. Labor market disruptions like the Great Resignation of 2020-2022, the trend of mass voluntary quittings by employees during and after the COVID-19 pandemic, reduced the pool of executive and administrative leaders in many nonprofits. As 2023 begins, layoffs are occurring in finance and tech. Even in stable times, human capital of all kinds—staff, volunteer, donor—can be viewed as a resource that needs constant nurturing, if only to prevent erosion. The financial metric of net capital investment (new investment less depreciation) can apply to IAs.

Some IAs may have longer life spans. The 21st century has seen a huge increase in the number of nonprofit organizations. But for many long-lived nonprofits, reputations and brands persist from the last century. These assets can contribute to their performance either via operational activities or through reputation and branding.

Nonprofits must make sure to protect the value of such long-term assets. Take, for example, the Susan G. Komen Foundation, a long-standing leading channel for contributions to breast-cancer research and treatment. But in a decision cited as one of the “follies” of 2012 in Ad Age, Komen’s board withheld routine funding from Planned Parenthood. The divisive move led to departures of important executives and trustees, and loss of support from many local and regional chapters. In addition, use of the color pink rapidly spread to competing breast-cancer organizations, as Komen lost some of its customary (but not proprietary) hold on the pink color-and-ribbon combination. Other breast-cancer fundraising groups have since leveraged in their own events and appeals the value Komen built. Komen’s brand, reputation, relationships with its donors, committed volunteers, and national scope—crucial assets to nurture and deploy—were reduced for some time, and with them, Komen’s ability to fulfill its mission.

Longer-term assets, such as brands, have value based on reputation, earned over substantial periods of time. Being oldest can mean being venerable, having a distinguished heritage. The current leaders of old organizations that were first, or biggest, or best known in their field inherit that reputational capital. Maintaining the value of that reputation requires performance at the margin that is at least as worthy as the reputation. Like human-capital assets, reputation and brand can increase or decrease in value, offering rationales for nonprofit leaders to monitor and invest in their reputational capital. Long-lived organizations have also made many promises—an issue to which I will return in my discussion of ILs.

Other longer-term strategic opportunities come from comparatively lower costs of operation, or from realizing economies of scale or scope—i.e., being able to distribute costs over more places and diverse program offerings. National operating footprints facilitate messaging and service delivery for the American Red Cross, the American Cancer Society, and The Salvation Army. Another resource resides in the willingness of suppliers to offer discounts, in-kind services or products, or other operating conveniences. While these have a transactional nature, they provide operating efficiencies and reduce the need for cash while enhancing service delivery.

What are IAs worth? A three-part test helps to understand their presence and value by considering their value, durability, and cost.

In evaluating an IA’s contribution to a nonprofit’s performance, resource-based theory provides an analytic framework.3 The essence of this theory is that strong competitors have resources with four key characteristics, known by the acronym VRIO: One is some inherent value that offers an operating or competitive benefit, such as through efficacy or another unique quality. The second property is rarity, or being in limited supply. The third is that the resource cannot be adequately imitated, and its value can’t be obtained another way. Finally, the resource is one that the nonprofit is suitably organized to use and exploit. Those characteristics match the three Pennsylvania arts organizations and their unique performance venues. But their absence also matches the Komen case: The pink brand emblem and ribbon could be imitated and were associated more with the cause than with the organization.

How long will IAs last? A longer time horizon for planning brings up questions of the life cycles of promises. As IAs are promised and anticipated, rather than contracted, their value fluctuates. Nonprofit leaders can estimate the probability that offered charitable and voluntary support will actually be delivered, the probability that promised facilities will be available, and generally whether those making the offers are moving into better or worse positions to fulfill their promises. Recent whipsaws, from growth to pandemic to recovery to inflation, illustrate tests of those promises.

What do IAs cost? Like real assets, invisible ones require maintenance and new investment, both to improve effectiveness and to promote enduring relevance and efficacy. They consume real-time economic resources in regular operations to maintain their value, efficacy, and quality. Knowledge and productive human capital require updating and complementary tools to reach their potential. Volunteer and donor potential both require cultivation, recognition, and management. Capacity-building is not free. The invisible-balance-sheet orientation routinely recognizes those costs as asset maintenance.

Invisible Liabilities

Liabilities, by contrast, are those obligations that organizations incur to operate, acquire productive assets, and build capacity to deliver desired results. They have terms ranging from the short run, such as payables due from operations, to longer-term debts for capital investment. Contractual liabilities have stated terms, including penalties for failure to discharge obligations. Nonprofits undertake these with payables, loans, mortgages, bonds, and the like.

All liabilities can be viewed as statements of obligation, or IOUs. The term “liability” is sometimes loosely applied to things that make operating tough, such as the liability of being new or of being in a difficult competitive position. But the focus here is on obligations assumed, not on conditions that may limit performance. So invisible liabilities are the obligations that nonprofits take on that go beyond formal contracts with counterparties. They emerge when the organization pursues altruism, excellence, or impact in the face of likely operating losses.

Nonprofit leaders may benefit from seeing their organizations as settings for balancing promises made and promises kept, and for recognizing forms of capacity as assets to be stewarded.

Beyond such contractual commitments, nonprofits willingly state how they will improve the world and embrace the burden of accomplishing that improvement. Taking on ILs is close to the heart of what nonprofits offer a complex society. Their mission statements emerge from past and/or present voluntary willingness of organizational leaders to improve the world in some fashion, independent of reward or legal mandate—nobody is forced to create a nonprofit. The broadest level of external commitment attaches to the mission statement and to achieving social impact over the long term. Still, a nonprofit mission, though aspirational and inspiring, is not a contract. It can’t be assigned as an obligation to any other entity, though other nonprofits may offer to share or adopt it. The priority of the obligation is a manifestation of the strength of the embrace.

The missions of nonprofits are part of the base for attracting the resources necessary to accomplish their work. In continuing operations, nonprofits create channels for other constituents to participate in reaching those results. These activities require the nonprofits to adopt liabilities. Nonprofits offer volunteers positive experiences and a path to help address social needs. In turn, the volunteer experience should meet or exceed what the person anticipated. Nonprofits offer donors (individuals, households, and small businesses) and institutional funders (corporate, foundation, or public) the service of being a channel or partner. In accepting their funds, the nonprofits assume liability for how efficiently they use the money. This assumed responsibility is subject to regular accountability to maintain those beneficial relationships.

Even more important are the obligations to beneficiaries to deliver services. I’ve served on the board of New Bethany Ministries in Bethlehem, a human-services nonprofit that offers street-level programs in nutrition and housing in high-poverty districts. Its indigent clients trust that its daily meal center and pantry will be there for them; the organization willingly, even eagerly, lets them hold this expectation. A former executive director there described her role to me as “the agent for the clients.” While those clients might never claim that service is “owed” to them, she spoke for the moral commitment that guided the organization to expend resources as if that claim existed. It had as strong an impact on decision-making as a contracted debt.

In another example, class sizes and student-body composition in private nonprofit colleges show their willingness and ability to accept financial challenges in pursuit of costly mission objectives. Muhlenberg College, where I teach, celebrates low student-to-faculty ratios as one defining characteristic of its educational offerings. Yet that is objectively costly relative to other, higher-volume delivery models in larger institutions of higher education. Some colleges pursue first-generation students and those from historically underrepresented communities, understanding that those students offer less net revenue because of financial-aid needs.

One cue for recognizing that a nonprofit is open to taking on ILs is what it prioritizes in its budgeting. Most business enterprises start by forecasting sales of their offerings of various products and services, which leads to estimates of gross margins and operating income accessible for investment, for distribution to owners, or to build financial capacity. Their capital plans may include raising more funds via debt or equity. By contrast, many nonprofits I have observed start their operating budgets with planned expenditures designed to reach programmatic and strategic goals. Then they plan to finance that spending with revenues from various anticipated sources. Some reach balanced spending plans only by gamely anticipating external funding to plug gaps between desired spending and known revenue sources.

Naturally, expense- and revenue-driven paths are intertwined, and nonprofits with strong earned income also emphasize the revenue side in their budgeting work. But those that start with spending to fulfill their raison d’être illustrate a willingness to proceed despite expected losses. Ultimately, accepting deficits in pursuit of mission makes ILs more contractual and financially binding.

At an institutional level, long-term ILs are created in the strategic management cycle. Nonprofits make plans to achieve mission-related impacts and offer anticipated results. The objectives and outcomes revealed in strategic plans create expectations. Such expectations ground a measure of accountability to internal and external stakeholders that cannot be fully discharged until the goals are reached and the benefits delivered. Those goals can also incorporate expectations about the quality or kind of programmatic delivery.

As if operating and long-term ILs did not present enough of a challenge, many nonprofits also inherit obligations created in the past that are still binding in the present. But legacy commitments may be viewed as combining substantive, symbolic, and ceremonial value. Preservation nonprofits are one setting where these legacies are central to mission, but nonprofits across the sector exhibit their debts to the past with lifetime recognitions and alumni celebrations.

Just as in the case of the valuation of IAs, nonprofit leaders must weigh the burdens imposed by ILs by examining the level of commitment made by the nonprofit, its expected duration, and the carrying cost. First, they must acknowledge that the commitment is, in essence, an obligation. Imagine a continuum of pledges ranging from the merely rhetorical to adopting, encouraging, and facilitating to avid pursuit. The commitments imposing the largest burdens are those that nonprofits pursue with resources.

A history of successful performance builds a reputation for accomplishment and also sets a standard of minimum performance, so that current and future achievements are no less than what was accomplished in the past. Fulfilling promises begets its own legacy of promises fulfilled, which begets external expectations that good performance will persist. Conversely, failure to fulfill promises makes a nonprofit appear less likely to accomplish its work and makes it a riskier place to support.

Nonprofit services for especially vulnerable populations create the most profound promises and can exact the highest resource costs borne by third parties relative to the share borne by consumers. Feeding the indigent is typically designed for that share to be zero. Performing arts and college education are designed so that the cost to recipients is more than zero but less than 100 percent. Other kinds of nonprofit services similarly operate at a loss but persist with subsidies of labor or other resources. The liability that arises from this kind of service is not contractual in the fashion of a repayment schedule for a loan, but it can exact a comparable economic burden. Its costs are revealed in the subsidies it requires, and in the effort required to obtain them.

Promises that go unfulfilled can continue to damage reputation and restrict access to other resources, as long as the commitments are remembered. Nonprofits and other organizations confronting their failures to achieve targets in diversity, equity, and inclusion, for instance, are increasingly subject to being reminded of these liabilities that have not yet been discharged. Such failures may not be the same as a default on a loan or the violation of a contract, but they can exact an equally weighty cost.

Invisible Net Assets

Nonprofit CFOs understand the overall financial health of their organizations in terms of net assets, which they calculate on their balance sheets by adding up all the assets and subtracting all the liabilities. Such net assets represent the nonprofit’s resilience and financial capacity.

Invisible net assets (INAs) are the share of nonprofit IAs that are not consumed by or committed to organizational action as ILs. They describe unburdened capacity that management may exploit for desirable action, such as by applying them to programmatic activities in pursuit of mission, using them to protect the organization, or finding ways to turn them into more revenue or reduced cost. Conceiving of INAs as the excess availability of IAs over the embraced promises of ILs also clarifies how they can be recognized, valued, improved, and used.

As assets, INAs have the potential to be deployed and represent capacity for action in the future. INAs reflect the confidence of outside and internal stakeholders in what nonprofits can accomplish, even taking into account the commitments they are already fulfilling. The contributors of IAs, who have made promises to nonprofits, evaluate how effectively those nonprofits have fulfilled their promises of impact. As these net calculations of promises made are formulated, contributors may condition their future support on the results of their evaluation. Satisfied contributors are more inclined to contribute more. These individual considerations for each contributor are aggregated into the nonprofit’s collective INAs.

For long-lasting nonprofits, the value of INAs as resources becomes evident when beneficial volunteer, donor, and institutional relationships are reliably available for operating or capital planning. They may originate inside or outside the organization. For clubs and cooperative nonprofits, for example, strong internal INAs rest in the collective weight of member capacity. An example is the share of an organization’s volunteers who are also among its donors. The boards and strongest financial supporters of community-based theaters, nonprofit choruses, and radio stations are often the actors, singers, and programmers—the ones who deliver the core artistic services. Crisis preparedness and succession planning are other internal INAs—they are latent, waiting to be used, not owed to anyone, but available. The worth and potential of INAs from external sources may be revealed early in capital campaigns during feasibility studies, when external consultants convert declarations of trust and confidence into financial targets. Whether internal or external, INAs represent free capacity to encourage growth, as well as reserves or insulation against external threats.

That capacity also completes the analogy with the financial balance sheet. An accounting or financial officer might call the proprietary firm’s excess of assets over liabilities retained earnings, net worth, or equity. It is wealth, available for distribution to owners, for net capital investment, or for reserves. Moreover, a principal objective of corporations is to maximize the present value of shareholder wealth; its leaders are responsible for devising strategies to accomplish that objective. Symmetrically, nonprofit leaders are responsible for maximizing the present value of those INAs by devising strategies that use and build on that capacity.

Putting the Invisible Balance Sheet to Work

So far, I have described the invisible balance sheet as a conceptual model that captures important characteristics of nonprofit governance and leadership. Lessons from that model offer nonprofit leaders tools to recognize and manage their IAs, ILs, and INAs. There are ways for nonprofit leaders to use the model, to monitor the balance between the promises they have made and promises they rely on. Thinking like a CFO, a leader weighs the invisible balance sheet, the time frame for its assets and liabilities, and the riskiness of the assets and obligations. In strategic planning, boards can make thoughtful decisions about how best to use INAs.

First, leaders must recognize their organization’s IAs and evaluate them by determining their worth and importance relative to each other. Recall that IAs have different forms. Leaders must assess the promises and capacities that are available from human capital (knowledge, cultural and structural, social and network, leadership, staff and voluntary, governance), from philanthropic capital, and from suppliers in the form of discounts. At the same time, leaders must assess longer-lived IAs, including reputation, durable strategic positioning, brand equity, or economies of scale.

For each of these forms of IA, invisible-balance-sheet analysis investigates its worth for the future, using the VRIO framework to assess their utility. A few questions make the case: How will each type help the organization get things done, and done well? That is its value. Are those assets hard to find (rare), and hard to imitate? Is the nonprofit organized to use those latent capacities? The organization’s past performance persists in its reputation, which is subject to the same tests to determine its value.

At the same time, leaders should recognize the organization’s ILs and evaluate their burden, duration, and cost. Again, the assessment should be made with a view to the future, not a restatement of the past. First, what promises did the nonprofit make to support each of those assets? What do beneficiaries expect? What has the nonprofit embraced, and—just as important—what do those counterparties think the nonprofit has embraced? What was committed to beneficiaries, to volunteers, to staff, to donors, to communities, and so on, and what expectations have been attached to those commitments?

Financial managers are trained to discount future cash flows to estimate value at the present time. Part of evaluating the worth of IAs and ILs is to consider how their present values reflect expectations about the future. Both IAs and ILs have life cycles and life stages, reflecting the natural appreciation and depreciation in human capital and relationships. Nonprofit leaders should monitor whether these resources are being eroded or enhanced (IAs), and whether external and internal expectations are growing (ILs). An improving economy with ample disposable income can lead a nonprofit to expect future financial support from donors—and a contracting economy can presage a drop in support. At any given moment, labor market conditions and other factors may lead to growth or decay in volunteering.

Monitoring and managing both sides of the invisible balance sheet is a part of the stewardship element of strong leadership. On the asset side, economic resources used to attract promises of contributed time and money are the maintenance costs of those IAs. Strategically, investments in volunteer and donor programs (cultivation, recognition, solicitation, etc.) should grow those resources. Budgeting practices reveal tensions between programmatic spending and resource-development outlays, but a leader who stewards his or her organization properly considers the longer-term value of those resources and interprets the spending as part of asset management. On the IL side, the leader should monitor the cumulative scale of promises the nonprofit has made and the degree to which counterparties accept those promises. To manage the invisible balance sheet, nonprofit leaders should right-size the liabilities of new performance commitments, taking care not to make promises they can’t keep.

However, INAs can also support those new commitments. Such reservoirs of trust and confidence provide support for expansion (more services, beneficiaries, other diversification). Reputation is an element of bargaining power in contracting and can help get preferential positions in collaborations and partnerships. Nonprofit leaders must navigate the trade-off between using capacity to innovate and make strategic investments and refusing to make promises that are hard to keep. In either case, nonprofits should seek to increase their credibility ratings and secure reputations for accomplishing what is necessary and what they say they will do.

The analogy with the balance sheet has limits, however. Take, for example, the accounting treatment of net assets as endowments, reserves, or resources for expansion. Unlike bank deposits, INAs are perishable and hard to attribute specifically to any source, or to subject to enduring restrictions, so nonprofits cannot see them as a permanently dedicated or restricted endowment but should instead view them as operating reserves of goodwill or bases for protection or expansion. Financial balance sheets can be used for analysis of liquidity and solvency, but that is perhaps a step too far for invisible balance sheets.

Developing measurement standards also requires a lot more work. Many judgment calls are needed to assign values to the individual items; that suggests opportunities for leaders, managers, and other stakeholders to share their evaluations. (For more on this challenge, see the invisible balance sheet exercise here.)

Beyond the simple management of contracts and compliance, nonprofit executives and boards should take long-term views, examining how the resources they depend on are made possible by how well they use them to accomplish their goals. Despite these and other limitations of the invisible-balance-sheet model, nonprofit leaders may benefit from seeing their organizations as settings for balancing promises made and promises kept, and for recognizing forms of capacity as assets to be stewarded and maintained. The invisible balance sheet highlights trust, confidence, and expectations as the currency of accountability; provides a framework for evaluating those resources; and gives leaders another way to evaluate, improve, and communicate nonprofit performance and impact.

To warm up your thinking about invisible assets, liabilities, and net assets, try this exercise.

Read more stories by Roland J. Kushner.