It is telling that so many in the impact investing sector—including us in this online series—consistently fall back on microfinance as the example of successful impact investing for the disadvantaged. Microfinance, despite recent controversy and misgivings, has indeed reached massive scale—an estimated 200 million people. But microfinance took three decades to attain this scale, and it still reaches a modest percentage of those in need.

The contrast to mobile telephony—a purely commercial innovation that has fundamentally improved the lives of the poor—is dramatic. Although the first commercial mobile cellular services were established in 1978 (around the time of the emergence of microfinance), the number of mobile accounts in the developing world soared from less than five percent of the population in 2000 to more than 70 percent (more than 4.5 billion people) today. Although the dynamics and challenges of microfinance and mobile telephony are quite different, we must ask ourselves how we can create more innovations that achieve the kind of breadth and rapid expansion that mobile telephony experienced.

In this online series, we’ve argued that it is both possible, and urgently necessary, for impact investors to head in this direction. But success will require a shift from current practice. Instead of cherry-picking investments in individual enterprises that will yield high return and high social impact, we need to commit to “priming the pump” to encourage the growth of new industry sectors. We’ll need to take more diverse risks (not just traditional firm-level business risks, but sector risks), and deploy a variety of capital types (from grants to a variety of high-risk for-profit investments)—to get early-stage innovators off the ground, and support the infrastructure that accelerates their success. This will also frequently require deploying political and policy capital—types of capital not often discussed in the impact investing arena. In order to promote the delivery of high quality products at reasonable prices, policymakers may need to confront vested interests to promote competitive markets that protect the interests of consumers.

We conclude the blog series by illustrating why these actions are of such great importance to billions of people.

Altering the S-Curve

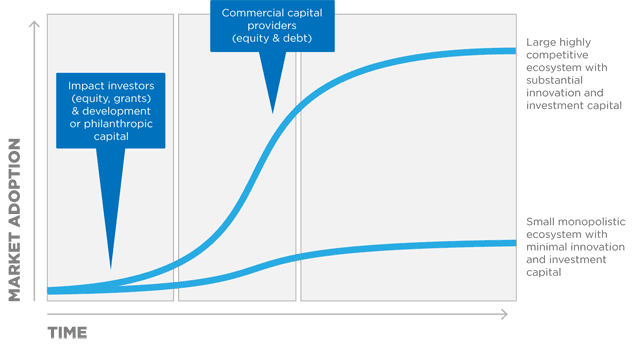

For years, analysts of commercial markets have used the so-called “S-curve” to describe the adoption of a new innovation across a society over time—from early adoption, through rapid growth and to maturity. Typically, the adoption of a new innovation happens slowly in the initial phases, then increases rapidly for a number of years before beginning to slow down to where a product reaches what appears to be a long-term saturation point.

The S-curve shows us in stark terms how seemingly small changes can dramatically impact millions of lives. Bringing forward the year of “take-off point or accelerating the rate of adoption, even by a small amount, can yield extraordinary leverage in terms of the number of lives impacted. These kinds of interventions can make an exceptional difference in the developing world, where very few market ecosystems develop rapidly and seamlessly.

The bottom curve in the chart above—with limited scale and very slow adoption of a new product—unfortunately represents the status quo for most sectors serving the disadvantaged. We have far too many examples of sectors captured by one or two monopolistic players that prevent further growth and innovation. In many slums, for example, water is provided by local gang lords, who will prevent anyone else from supplying water or demand graft in exchange for market access. The same situation holds for moneylenders that operate in remote villages where banks are absent. Such situations tragically force poor customers to pay high prices for low-quality products, limiting their choices and, ultimately, their economic mobility.

Emerging Sectors

Luckily, the picture is not entirely bleak. We are beginning to see the emergence of sectors that have a strong chance of beating the typical “lazy S-curve. The solar lighting sector is one robust contender. Starting around 2007, early stage impact investors helped companies like d.light test production of low-cost, environmentally friendly lighting that could serve the 1.4 billion poor people currently without access to grid electricity. Over time, a number of competitors have entered the field, driving prices down to below ten dollars for simple lanterns and increasing the quality and diversity of products offered. The growth of the solar lighting sector has in turn created secondary ecosystems, further helping to accelerate the market. A new crop of companies like M-KOPA and Eight19 have developed creative financing schemes enabling poor customers to afford lanterns by spreading out the schedule of payments.

Industry-specific government policy has played a huge role for the solar home products—both for good and ill. In places like India, solar lantern producers have had a harder time competing because of government subsidies for kerosene—a well-intentioned policy that unfortunately keeps the poor dependent on an environmentally hazardous and less efficient energy source. By contrast, in Bangladesh, the government has greatly accelerated the market for home solar systems by providing supportive financing terms. These financing plans have helped some 750,000 remote households and shops to access a suite of solar products that enable children to study at night and businesses to extend their hours past dark. Over 30,000 solar home systems are being installed every month in rural Bangladesh.

We also see great promise in the affordable private education sector. In the early days, commercial investors were skeptical that private schools could deliver affordable, high quality education to poor people in Kenya. But Bridge Academies has tested and refined a highly innovative “school in a box” model, delivering high quality instruction, and expanding to nearly 82 locations. In the process, they’ve started to receive attention from serious commercial investors. Not only will Bridge itself likely be able to expand operations to neighboring East African countries—we also expect copycat businesses to emerge, thus further accelerating the growth of the sector and delivering vastly improved educational opportunities to millions of children.

As previously mentioned, the success of Kenya’s MPesa mobile payment system, also portends an exciting new future for mobile payments. The success of mobile payments would not only create more efficient, safe and affordable payments for millions. It would also foster additional new sectors in related mobile services and mobile commerce, thus further enhancing opportunity and spawning economic growth.

Success for critical industry sectors is far from guaranteed. Any number of potential pitfalls—from political sensitivities to marketing challenges to local economic shocks—could slow down or halt the rate of growth. And even if these sectors are successful, we’ll be faced with a number of new and challenging questions. For example, having developed an innovative model of affordable education for the poor, should firms such as Bridge open-source their learning to encourage replication, or is it preferable keep trade secrets in order to maintain competitive advantage? How does corporate ownership and governance shape a firm’s focus on critical issues such as an adherence to a social mission? Does a firm even need an explicit social mission to have positive social impact? How do answers to these questions evolve when firms begin to tap commercial capital markets?

Getting to Takeoff

We do not pretend to have all the answers. We simply know that even small steps in the direction of bending the S-curve can alter the lives of millions. If we had worked earlier with policymakers in Andhra Pradesh to ensure healthy competition and reasonable consumer protection, millions more people would now have access to financial services in India. Or recall our earlier examples about medical technology for the base of the pyramid in India. Accelerating the point of takeoff for medical device industries by three to four years would mean an additional two billion treatments per year for the poor—which could mean the difference between life and death for many.

The impact investing sector, while still in its infancy, has made remarkable progress in building awareness that business can generate a positive social impact. Although individual firms remain the essential innovators and building blocks of social change, they are means to a broader end of creating innovations that can touch the lives of hundreds of millions. It is time now to evolve the conversation, and our resource commitments in the direction of sparking, nurturing, and scaling these new industry sectors that are the true promise of the impact investing industry.

What is readily apparent to us is that no one organization, or one type of organization, can do this alone. Success does not depend upon perfect coordination or a grand plan. After all, we are talking about innovation, which requires experimentation, learning, and serendipity. But success does require a determined, thoughtful, and frequently collaborative effort by those who believe that the power of markets and the inspiration of entrepreneurs can be tapped to create opportunity and a brighter future for billions.

Read more stories by Matt Bannick & Paula Goldman.