(Photo by iStock/sorbetto)

(Photo by iStock/sorbetto)

The vast majority of investors throughout the world have a single goal: to earn the highest financial return. These socially-neutral investors only want to maximize their risk-adjusted returns and would not accept a lower financial return from a socially beneficial investment. An increasing number of socially-motivated investors have other goals besides maximizing profits. They seek to align their investments with their social values (value alignment) and, where possible, to enable the companies in which they invest to create more social value (social value creation).

The thrust of this article is that, while it is relatively easy to achieve value alignment, actually creating social value is far more difficult.

Socially motivated investors who seek value alignment would prefer to own stocks only in companies that act in accordance with their moral or social values. Independent of having any effect on the company’s behavior, these investors may wish to affirmatively express their identities by owning stock in what they deem to be a good company, or to avoid “dirty hands” or complicity by refusing to own stock in what they deem to be a bad company. Value-aligned investors may be concerned with a firm’s outputs—its products and services; for example, they might want to own stock in a solar power company or avoid owning shares in a cigarette company. Or the investors may be concerned with a firm’s practices—the way it produces its outputs; they might want to own stock in companies that meet high environmental, social, and governance (ESG) standards, and eschew companies with poor ESG ratings. To achieve their goals, value-aligned investors must only examine their personal values and then learn whether the company’s behavior promotes or conflicts with those values.

Socially motivated investors who wish to create social value through their investments have the much more challenging task of causing an investee company to increase its socially valuable outputs—for example, by enabling it to provide additional health care or education to poor people in developing countries, or inducing it not to despoil the environment. Appropriately called “impact investments,” these investments must lower the cost of capital to the enterprise compared to ordinary commercial markets, thereby allowing it to produce more socially valuable outputs or to engage in more socially valuable practices—the criteria for creating social value.

Both investors who seek value alignment and those who seek to create social value face the question of what financial sacrifice, if any, they must make to achieve their social goals. When can investors achieve their social goals through non-concessionary investments, from which they expect a full risk-adjusted market-rate financial return? When must the investments be concessionary, sacrificing some financial return for social value?

The literature published by fund managers, foundations, and trade associations manifests considerable optimism about the extent to which socially-motivated investors can ensure value alignment and, indeed, create social value through non-concessionary investments. Some funds, like Calvert Investments, offer their investors (at least) value alignment with no financial concession, while others, like Generation Investment Management, offer alpha—better than risk-adjusted market returns. And some funds, like Equilibrium Capital, promise their investors social value creation without sacrificing financial return. Some foundations, like F.B. Heron Foundation, imply that they can create social value through non-concessionary investments of their endowments and urge their peers to follow suit.

We do not doubt that it is often possible to achieve value alignment with little or no financial concession. But though we disagree with those who define impact investing to include only concessionary investments, it is in fact quite difficult, albeit not impossible, to create value―to have social impact―while targeting risk-adjusted financial market returns.

In any event, we believe that the term “impact investor,” as its name implies, should be reserved for investors who seek impact rather than value alignment. The field can only grow responsibly if individual investors, impact investing trade associations, and fund managers are candid with themselves and others about the conditions necessary for real impact.

The three main points of this essay are:

- Impact investing in public markets. It is virtually impossible for investors to affect the outputs or behavior of firms whose securities trade in public markets through the financial mechanisms of buying and selling securities in the secondary market. Socially-motivated investors who would like to make ESG standards the norm must join forces with consumers, employees, corporative activists, and regulators.

- Concessionary investments in private markets. However, it is possible for concessionary impact investors to affect the outputs of firms in private market transactions by providing subsidies in the form of accepting financial returns below the level that socially-neutral investors would require. Foundations’ program-related investments are paradigmatic of such subsidies. The difficulties of concessionary impact investments lie in targeting the subsidy so as to benefit one’s intended beneficiaries rather than other investors or the company’s management, and in not adversely distorting the markets in which the firm operates.

- Non-concessionary investments in private markets. It is also possible for non-concessionary impact investors to affect the outputs of firms in private markets by taking advantage of private knowledge that they or their fund managers possess. Non-concessionary investors’ claims to have private information should be taken with a grain of salt, however. These investors are playing in a highly competitive game with the universe of private equity investors whose success depends on developing value-relevant private information.

Before turning to the substance of our argument, it is helpful to review the rather confusing terminology concerning socially-motivated investments used by foundations and other professional socially-motivated investors.

Terminology of Socially-Motivated Investors

Impact Investments are socially-motivated investments that are made for the purpose of increasing or improving the socially-valuable outputs and practices of investee enterprises: for example, manufacturing anti-malaria bed netting or creating jobs for the poor. In our terms, these investments seek to create social value. Impact investments can be made by all types of investors: foundations, family offices, endowments, funds, and individuals. Impact investments are meant to create social value by increasing the investee organization’s outputs rather than just aligning the investors’ portfolio decisions with their social values.

Impact investments may be concessionary or non-concessionary. Some impact investment funds, such as, DBL Partners, explicitly target market returns. Others, such as Acumen, expect to earn less than market returns. And some, such as Bridges Ventures and Omidyar Network, consider both types of investments.

Mission, or mission-related, investments refer to investments that are made by a foundation in pursuit of its charitable mission. They fall into two categories: The first are non-concessionary mission investments that have the primary purpose of generating financial returns for the foundation’s balance sheet and that are made in companies whose outputs or practices are consistent with the foundation’s mission. Non-concessionary mission investments seek at least value alignment. This article addresses the contested questions of whether and when non-concessionary mission investors can go beyond value alignment to create social value—a distinction largely absent from current discourse.

The second type are concessionary mission investments, typically made as program-related investments (PRIs). PRIs are a construct of the US Internal Revenue Code, which requires that their primary purpose be not to generate financial returns but rather to further the foundation’s charitable purposes. Like grants, PRIs count toward a foundation’s required annual payout of five percent of its endowment. And like grants, PRIs seek to create social value, that is, to increase or improve the investee’s socially-valuable outputs.

Socially-responsible investments are investments whose primary purpose is to generate financial returns and that are aligned with certain values―what we have called value alignment investing. These include, for example, good ESG practices—that may be independent of a foundation’s particular mission. In contrast to mission investing, which focuses on actively placing capital in business enterprises, socially responsible investing also includes divesting from, or not investing in, companies whose outputs (e.g. alcohol, tobacco, firearms, and gambling) or business practices (e.g. poor treatment of employees or environmental degradation) are antagonistic to the investor’s values. Value alignment investors may also engage in shareholder activism (e.g., initiating proxy proposals and voting proxies) to influence an investee’s behavior.

Most such investments take place in public markets and are non-concessionary—that is, they are expected to earn at least risk-adjusted market returns. As with non-concessionary mission investments, this article asks whether and when socially responsible investments can go beyond value alignment to create social value.

Impact as a Requisite of Value Creation

To say that a socially-motivated investment creates social value is to say that the investment produces a social impact—an outcome that would not occur but for the investment. For an investment to have social impact, it must meet both of these conditions:

- Enterprise impact. The investee business must produce the investor’s intended social outcomes; and

- Investment impact, additionality, or social value-added. The investment must increase the production of those outcomes.

To illustrate enterprise impact, suppose that you have invested in an enterprise that provides health care for the very poor in a developing country. Enterprise impact requires that enterprise-related health care professionals are in fact serving the poor (or will when the enterprise strategy is implemented) and, as a result, that their clients have (or will have) better health outcomes.

The matter of investment impact, additionality, or as we’ll call it henceforth, social value added, is unique to impact investing. For an investment to meet the condition of social value added, it must increase the amount or quality of the investee firm’s socially valuable outputs or practices. As we will explain below, an investor who believes that mobile telephony has tremendous social and economic benefits might have social impact by investing in a risky mobile telephone startup in a developing country, but cannot have impact by investing in AT&T. In the former case, the investor may provide essential capital that the start-up cannot get elsewhere; in the latter case, his investment will not result in additional phone access for even a single customer.

An investment can affect a business’s operations in two fundamental ways: through financial impact or signaling impact.

- Financial Impact. Assuming the investor believes that the investee enterprise has opportunities to increase its production of social value, an investment yields expected financial impact if it provides more capital, or capital at lower cost, than the enterprise would otherwise get from ordinary commercial, socially-neutral investors. Under these circumstances, the investment meets the criterion for social value-added. Conversely, a divestment would have financial impact if it deprived a wicked enterprise (that is, one that generates negative welfare consequences to the public at large) of needed capital that it cannot replace at an equivalent cost. But if the capital can be replaced at the same cost, then the divestment may create value alignment but does not create social value other than possibly through signaling impact. As we will see, divesting stock in a publicly traded company will generally not directly deprive a wicked enterprise of capital. Social impact investors, like general partners in private equity firms, may also provide non-monetary assistance, such as improving management and governance, fundraising, and networking. Because such assistance is almost always ancillary to providing financial impact, we will include it in this category rather than create a new one. (Investments are occasionally designed to improve an entire sector. This is the rationale for some of Omidyar Network’s and Gates Foundation’s investments.)

- Signaling Impact. The investment decision may indirectly affect an enterprise’s cost of capital by signaling approval or disapproval of the enterprise to consumers, employees, regulators, or other stakeholders, and thereby affect their behavior; or the investor may engage in shareholder activism by initiating or voting proxy resolutions with the goal of affecting the corporation’s behavior.

Whether an investment has either financial or signaling impact is a matter we address in the remainder of the article. We focus mainly on affirmative impact investments intended to increase the investee’s socially valuable outputs. But the same analysis applies to divestments intended to induce a firm to improve its practices.

Concessionary vs. Non-Concessionary Investments

As previously defined, a concessionary investment is one with a below-market risk-adjusted expected financial return. The concession is the economic equivalent of a donation or grant intended to produce a social return. Whether an investment by a foundation is non-concessionary or concessionary is a question of its expected risk-adjusted return, and not whether the funds come from the endowment or program budget, which is a matter of internal governance and accounting.

Socially-motivated concessionary investments have the potential to reduce an enterprise’s cost of capital since, by definition, socially-neutral investors wouldn’t invest on below-market terms. The potential upside of a concessionary investment is that it will enable the enterprise to produce more socially valuable outputs. Apart from the inevitable possibility of failure, the potential downsides are that the subsidy will not lead to improved social outcomes but merely redound to the benefit of other investors; or worse, that the subsidy will distort the markets in which the investee operates to the ultimate detriment of the investors’ intended beneficiaries. We will discuss the potential social value of non-concessionary investments in the next section.

Although we have characterized a concessionary investment as one that sacrifices risk-adjusted market returns, there are two ways in which even a seemingly non-concessionary investment may compromise the investor’s financial interests.

First, a socially-motivated investment may sacrifice portfolio diversification, thereby exposing the investor to a heightened degree of risk for which he will not be compensated. We would expect this effect to be most prominent where an investor divests from an entire sector (e.g., fossil fuels) or overweights a particular sector because of the potential for social gain (e.g., renewable energy).

If certain stocks or industries are perceived to be “mispriced” in that they offer extraordinary returns, risk-averse investors will rationally choose to sacrifice an element of diversification by overweighting the undervalued security or industry in their portfolio to the point where the benefit of greater expected return is offset by the cost of greater portfolio risk due to reduced diversification. The more risk-tolerant an investor is, the more he or she is willing to sacrifice diversification to achieve the greater expected return.

Similarly, if investments in (or divestment from) certain stocks or industries are believed to increase socially-desirable outcomes, then socially-motivated investors will rationally choose to sacrifice an element of diversification by overweighting (or underweighting) such securities or industries in their portfolios. They will do so up to the point where the perceived benefit from the socially desirable outcomes their action produces at the margin is offset by the cost of the greater portfolio risk they must take on for doing so. The greater the value investors place on the social gains their investments produce, the more they should be willing to sacrifice diversification to achieve it.

Beyond diversification costs, socially-motivated investments may incur incremental human capital costs in pursuit of socially-motivated investments. The due diligence effort of socially-neutral fund managers or investment staff is designed solely to enhance financial returns. By contrast, socially-motivated fund managers conduct due diligence and post-investment interventions to enhance social as well as financial performance—resulting in higher aggregate evaluation and monitoring costs. Such costs may be partially outsourced to fund managers and consultants who charge incremental fees for assembling socially-screened investment portfolios and incremental fees for manufacturing benchmarks against which such portfolios can be evaluated for investment performance.

These additional costs may be subsidized by socially-motivated investors, or by the individuals working for socially-motivated investors, who may accept lower compensation than they could get elsewhere because of their social commitment. Such hidden subsidies may make an investment even more concessionary than it appears on its face.

Three Big Questions

The rest of this article explores three big questions. What impact can socially-motivated investors have on publicly-held companies? What impact can these investors have on privately-held companies? And what impact can these investors have on companies when working in concert with consumers, corporate activists, and other socially-motivated people and organizations?

Financial Impact in Public Markets

When can investments or divestments in public capital markets have impact by affecting the behavior of investee firms directly through purely financial mechanisms? The answer is, virtually never.

Suppose that a publicly-traded company produces outputs that are valued by a socially-motived investor, for example clean energy or drugs to cure dread diseases. If you are an impact investor who values these social goods, you would buy shares of the company if you believed that your purchase, along with the purchases of others like you, would cause the share price to increase, thus causing the cost of capital to the company to fall. As a result, the company would be able to finance more projects that produce the social benefits that you value. The company would need to sell fewer shares to raise a given amount of capital; or more capital could be raised for a given number of shares issued, thereby financing an increased volume of desirable projects.

But the vast majority of investors in public markets are socially neutral—hence, indifferent to a firm’s social value. Therefore in public markets, any premium in the valuation of shares that results from socially-motivated investors clamoring to own them presents an opportunity for socially-neutral bargain-hunters to profit from selling shares that are overpriced (from a purely financial perspective). If there existed two companies, alike in all respects except that one produces socially-valuable goods and the other does not, any increase in the share price of the former will prompt socially-neutral investors to sell its shares and buy shares of the latter. This process would continue until the stock prices of the two companies were identical, thereby eliminating any impact on the share price based on the socially-motivated trading, and therefore neutralizing any social value added. Indeed, the socially-neutral investors needn’t own the overpriced shares to effect this arbitrage. They could borrow the shares owned by others and sell the borrowed shares—the common practice called short-selling.

In any event, purchasing an existing share of stock in a company that produces socially-desirable outcomes is not equivalent to purchasing new shares issued by that company. One person’s purchase of shares is another person’s sale. Unless the firm raises fresh capital in the primary markets, the scale of its activities are largely unaffected by transactions in the secondary market.

Of course, firms sometimes do avail themselves of the primary markets. In principle, public firms could advertise for subsidized capital in the primary markets to finance socially desirable activities. For example, an electric power company whose stock trades at $100 per share could announce that it is seeking investors to purchase newly-issued shares at $120 apiece so that the firm could afford to convert coal-fired plants to cleaner-burning gas-fired plants without causing existing investors to suffer a decline in share price below $100. If investors deemed the social value of improving the environment in this way to be worth at least $20 per share and can lock in the company’s environmental commitment, they would find such an investment attractive even knowing that the share would fall in value to $100 in the secondary market. In effect, this would be a $20 per share grant to the company conditioned on using the grant, in combination with raising non-concessionary capital, to convert its plants.

We don’t recall ever having seen an offering by a public company that has this characteristic, but in principle, a socially-motivated investor could have social impact by investing in a public company’s primary issuance of shares on subsidized or concessionary terms. (In several instances, the Bill & Melinda Gates Foundation has made PRIs of this sort to induce a small-cap biotech company to develop products for neglected diseases in developing countries.) This example provides a natural segue to the more pervasive opportunities for social impact available to investors in private markets.

Financial Impact in Private Markets

Let’s now turn to private markets, where information about the value of a firm is significantly less widely shared, ownership interests do not trade freely, and short-selling of overpriced claims is non-existent. In private markets, socially-neutral investors cannot eliminate through arbitrage the subsidy from socially-motivated investors in the same way they can in public markets.

An impact investor who is willing to sacrifice risk-adjusted returns sometimes can increase the socially-valuable outputs of an enterprise operating in non-public markets because socially-neutral investors would not provide capital on the same favorable terms. The impact investor would make a concessionary investment under such circumstances if he believed that a subsidy (equivalent to the difference between a market return and the expected return from the concessionary investment) to the investee enterprise would produce social value in an amount that warrants the subsidy.

Those investors who value producing social impact most highly will include the social value-producing company in their portfolio and will feel appropriately compensated for doing so. The marginal socially-motivated investor will be indifferent between investing in the social good producer at a discounted expected risk-adjusted financial return, along with receiving a social impact “bonus,” and investing in a socially-neutral investment at a higher risk-adjusted return but no social impact bonus. The most socially-minded investors who place the largest value on producing impact will get a bargain. They will receive a higher financial return than they would have required to find the investment attractive. And the least socially-minded investors will simply not include the social-impact investment in their portfolio.

A typical investee of a concessionary impact investment might be a start-up that has the potential to produce significant social benefits for, say, poor people living in developing countries, but is too risky to attract commercial investors. The rationale for the impact investment might be to prove the business’s commercial viability in order to eventually attract socially-neutral investors to supply growth capital.

The opportunity for social impact through non-concessionary investments also is greater in private than in public markets. Among other things, these markets are not informationally efficient. An investment officer for a fund that makes impact investments in a particular sector may possess the same kind of special knowledge about, say, enterprises delivering health or education services to underserved populations as venture capitalists and private equity investors have about technology, social media, and biotech industries. In both cases, their knowledge and expertise, not widely held by others, enables the fund managers to make savvy investments that either are not noticed or mistakenly thought to be too risky by other investors. While the conventional venture capitalist or private equity investor has special information about an investee’s financial prospects, the non-concessionary impact investor seeks special information about an investee’s potential social impact as well.

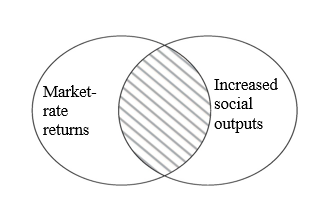

However, the non-concessionary impact investor faces difficulties, perhaps even conflicts, not faced by her concessionary cousin. Both investors seek to create social value, which, as we’ve seen, requires meeting two criteria: that the investee firm itself produces socially valuable outputs, and that the investment reduces the cost of capital to the investee firm (compared to investments from socially-neutral investors) and thereby can be expected to increase the firm’s socially valuable outputs. But whereas the concessionary investor is willing to sacrifice financial return to meet these criteria, the non-concessionary investor must satisfy a third criterion: the investment must be expected to earn a risk-adjusted market-rate return. If one were to draw a Venn diagram of the choices, a non-concessionary impact investor limits itself to the area of overlap between market-rate financial returns and increased social outputs.

To understand the non-concessionary investor’s difficulties in seeking to operate in the overlap, imagine that she is the general partner of a fund that promises its limited partners both social impact and market-rate returns. If there are many opportunities that present this overlap in the fund’s particular domain, everyone is happy. But if such opportunities are scarce, the general partner will have to compromise one or the other goal. Especially because she and her limited partners will find it much easier to measure financial success than social impact, the latter is likely to be sacrificed, intentionally or not.

There’s a further difficulty as well. Assuming that the enterprise has the capacity to scale its outputs, the more that is invested, the more the enterprise will be able to produce socially-valuable outputs. The general partner can direct investments to the enterprise in two ways: by attracting more investors to her fund, thereby increasing her investable funds; or by spreading the word about the investment to other investors, including competing funds. Foundations making (inevitably concessionary) PRIs are often happy to get the word out with the hope of sharing the burden. But unless our general partner needs co-funders beyond her budget to make the investment viable, she will typically wish to reserve the opportunities for her own limited partners in order to attract more investors to its funds, thereby restricting social impact.

The Power of Consumers, Employees, Corporate Activists, and Regulators

This article focuses on the power of investors to achieve social impact through financial leverage. We should note, however, that other stakeholders also can exert leverage, and sometimes more effectively. When one investor pulls out of a publicly-traded company, another takes his place, while each consumer who refuses to purchase apparel made by exploiting labor detracts incrementally from the seller’s bottom line. A company that treats its workers poorly may not be able to recruit valuable employees. And a company that despoils the environment may be scrutinized by regulators who have immense power over its practices.

Consumers are particularly influential when they act in concert as part of an organized movement intended to affect a firm economically or to influence regulators. Investors can contribute to such a movement symbolically and perhaps instill a degree of fear of unanticipated consequences in corporate managers. Although they seldom have direct economic clout, the signaling effect of divestment by a high profile investor may provide publicity and support for stakeholder efforts, including ESG-type proxy proposals.

The potential for an investment decision to contribute to this effort to influence firm behavior is highly dependent on the specific context. At one extreme, a silent investment or divestment decision not noticed by other stakeholders will have no influence, since investment decisions can have signaling power only if they are known. At the other extreme is a highly publicized decision made as part of a concerted boycott movement.

The 1990s movement to divest from companies doing business with South Africa and the current movement to divest from companies extracting fossil fuels are examples of divestment playing a role in broad social movements to condemn and influence the behavior of its targets. The strategies are essentially political, with the more stakeholders who express disapproval of the behavior the more effective.

At least one empirical study of the South Africa divestment movement by Siew Hong Teoh, Ivo Welch, and C. Paul Wazzan is consistent with this analysis. The study suggests that divestment had little if any effect on the capital markets, though it may have contributed to publicizing the moral issues. It is too early to assess the effects of the current movement targeting companies that extract fossil fuels. As of this writing in mid-2016, the coal industry is economically distressed and the oil industry is also faring poorly. But other factors, such as the advent of plentiful natural gas through fracking, improvements in solar and wind energy in part through government subsidies, and government regulations, such as renewable energy portfolio standards, may fully account for the situation. Few doubt that changes in consumer behavior, such as increased use of public transportation and electric and energy-efficient automobiles, and regulatory changes, such as a carbon tax, could significantly reduce CO2 emissions. Divestment may serve as a rallying point for such other actions, but as we have argued in this paper, it will have little if any direct economic consequences.

Advice to Investors

We conclude the article by offering five pieces of advice to the large majority of impact investors who do not make direct investments, but who instead place their confidence in the general partners of so-called impact funds.

- First, it is difficult, though by no means impossible, for a fund to create social value—as opposed to achieve value alignment—while also promising to deliver market-rate financial returns or better. Funds that promise both deserve special scrutiny.

- Second, if the fund is serious about impact, it should report on impact as well as financial returns, including an estimate of an investment’s social value-added. A strong signal that the general partner is committed to social impact as well as financial returns would be that her compensation is based on social impact as well as financial returns. (We would be eager to learn whether any funds have actually adopted such a compensation scheme and how the social impact is measured for compensation purposes.)

- Third, make sure that the fund manager is using appropriate benchmarks for the fund’s performance. The appropriate benchmark against which to evaluate private investments is other private investments, including the significant illiquidity premium associated with such investments.

- Fourth, you should treat the presence of any public equities in a self-styled impact fund as the thirteenth strike of the clock, which calls the others into question.

A final piece of advice concerns all investors.

- The socially-screened mutual fund industry should be regarded as offering investors a value alignment strategy, not an impact investment strategy. Investors in such funds should take care to understand the premium expense ratios charged by the sponsors of such funds as well as the sacrifice in diversification these funds may offer. Investors should also be skeptical of claims of social value-added that may appear in the marketing materials for such funds.

Read more stories by Ronald Gilson, Mark Wolfson & Paul Brest.