(Illustration by Vicki Turner)

(Illustration by Vicki Turner)

When the philanthropic sector refers to the Great Wealth Transfer, it usually means the transfer of family wealth from the Baby Boomer generation to their children.

Practices for Transitions in a Time Between Worlds

There is no manual for living through our wildly unpredictable times. How do we imagine, prepare for, and shape an unknown future? Who do we need to be or become? Instead of a road map, we offer this supplement to illuminate inquiries, capacities, and practices that we believe can open consequential new pathways to a better tomorrow. Sponsored by Joseph Rowntree Foundation

-

These Times Ask More of Us

-

The Work of Hospicing

-

Stewarding Loss

-

The Decelerator

-

Grief Tending

-

Prefiguring a Future We Want

-

A Creatrix Praxis Space for Liberation

-

Collective Imagination

-

An Infrastructure of Care for the Oracular

-

Awakening Complexity Consciousness

-

Server Farm

-

Sites of Practice

-

Reactivating Exiled Capacities

-

Rewiring the Great Wealth Transfer

-

A Regenerative Economy in Action

-

Tackling the Wealth Defense Industry

-

Secret Guides and Weird Waymarkers

Vanguard recently estimated that by 2030, some $10.6 trillion will have been transferred between generations in the United States, $3.5 trillion in Europe, and $2.8 trillion in Asia. These are enormous figures. To put the numbers in context, it is worth noting that globally, the private equity industry had $8.2 trillion of assets under management at the end of 2023.

The impact community is right to focus on this transfer of wealth and consider how these assets can shape the future, for better or worse. But there is another great wealth transfer happening every day that has contributed to this enormous accumulation of wealth: the monopolization of the economy. Industry concentration, whereby a few companies control an industry or many industries, has soared in developed nations in the last few decades, contributing to rising inequality in significant ways. This wealth transfer comes from the pocketbooks of consumers, from workers’ wages, and from the reduced profits of small and independent businesses as wealth flows to powerful companies and their shareholders.

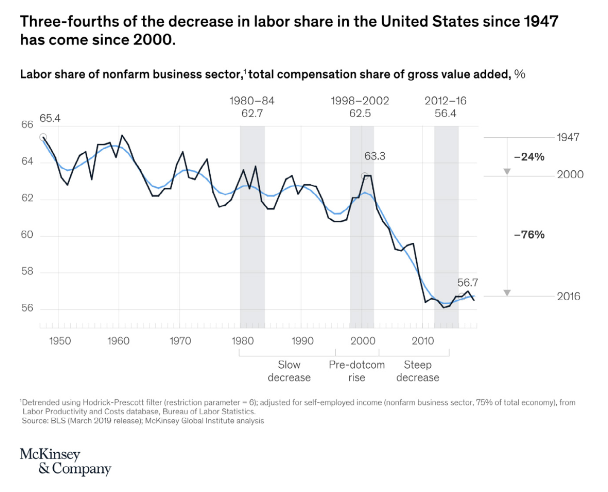

Take workers, for example. The labor share (how much GDP goes to workers versus capital owners), has fallen since its peak in 1970 in the United States. For decades, the labor share was two-thirds of GDP globally, but the labor share began to decline, from 65-66 percent of GDP in 1980 to 58-59 percent today. This decline may not sound dire, but it represents some $6 trillion less going to workers globally each year.

Another way to identify how much of the economic pie is going to workers is to look at the labor share of corporate income. This figure has declined since the 1980s, and since 2000, the rate of decline has accelerated. A 2019 McKinsey Global Institute analysis found that superstar firms and consolidation across industries was the third-most-important source of falling labor shares (behind economic supercycles, boom-bust dynamics, and rising depreciation due to a shift to intangible value, such as intellectual property).

Click to enlarge (Source: A new look at the declining labor share of income in the United States, McKinsey & Company)

Click to enlarge (Source: A new look at the declining labor share of income in the United States, McKinsey & Company)

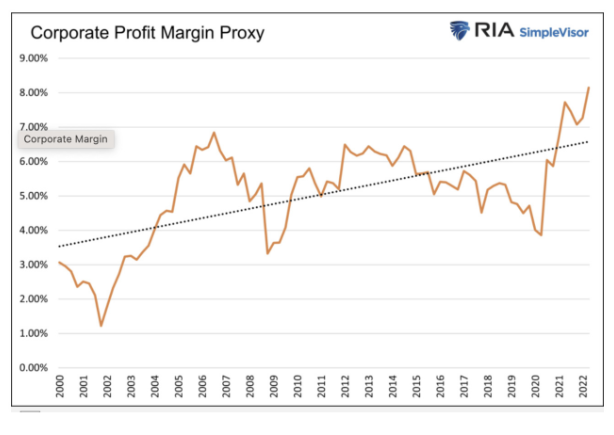

Coupled with flagging unionization and the rise of gig work and contract labor, workers’ bargaining power against powerful companies has eroded. Despite recent wage gains, workers still lag far behind companies and shareholders in receiving their share of the economic pie. In 2022, US corporations counted their highest profit margins since 1950, even amid the pandemic and high levels of inflation. In addition, in the last two decades, corporate profit margins have risen.

(Source: “Corporate Profit Growth Will Slow, Says The U.S. Fed,” investing.com)

(Source: “Corporate Profit Growth Will Slow, Says The U.S. Fed,” investing.com)

This trend toward concentration of market power and capital is the backdrop against which all investment, impact investment, and philanthropic investment conversations take place. Rather than individual investment decisions, the solution to concentration will come from public policy, newly structured investment mechanisms, and a radical scaling of alternative ownership and governance models.

But before we consider new frameworks for wealth, and what we call rewiring wealth, we should acknowledge that the current system of capital origination, intermediation, and allocation works like a Swiss clock. Every component feeds into another with great precision. While we deliberate on how to mend the current system, there is nothing broken about it; the current financial and economic system functions as it was designed. It focuses on achieving the goal of capital growth and preservation, serving a small minority of humans (7.2 billion people now sustain the privileged lifestyles of 800 million, or the top 10 percent). This economic logic also subsumes the value of nature and biodiversity.

This wealth system does not belong to the natural world. Instead, this artificial system was created by humans, which makes it entirely within our capacity to build something different. The current system was created according to values of ownership, extraction, and antisocial competition. But we can construct an alternative system, structuring it around a different value set: regeneration, reciprocity, care, and generosity. This system could encode our symbiotic relationship with one another and with nature. Wealth generated by this alternative system would benefit us all.

To realize this vision, we need a combination of factors to align. First, we need public policy and public investment, and an increasing recognition that “free” markets are incapable of solving the complex problems of economic distribution, climate change, and other collective challenges. This will entail the state asserting its right to structure markets in the public interest, including stronger antitrust enforcement, investment in public innovation, and industrial policy to reshape the terms and conditions of markets. Such policies are predistributive, not redistributive, and address market structure to ensure that markets are fair and competitive, create widely shared ownership and prosperity, and allow the best ideas, products, and services to flourish. Monopolization and the abuse of market power erodes the conditions of the economy in ways that harm us all. Philanthropies, investment advisors, and other ecosystem participants who care about sustainable futures ignore market power issues at their peril.

Second, we need to scale alternative ownership and governance models that can encode different legal rights to different economic stakeholders. Steward ownership is one example, where businesses are owned and operated by employees or other community members to circulate profits and economic gains more widely. A new book, Assets in Common, details historical and current examples of these corporate forms.

In Quebec, Canada, for example, a new legal vehicle has been in place since 2021: Community Benefits Trust/Fiducie d’Utilité Sociale. This instrument enables ownership and governance of a portfolio of community assets, including civic assets and community real estate. It can serve as a trustee for the voices of future generations and biodiversity and nature as it attains legal status. It can issue investment instruments such as long-term civic infrastructure bonds to capitalize its portfolio to align with the mission of community benefit. Philanthropies and impact investors should focus on seeding the next generation of disruptive businesses and technologies with different ownership structures.

Finally, we need new capital allocation toward transformation (different stewardship of capital and new asset classes). If this sounds too radical, the reality is that these alternative ways of raising, stewarding, and allocating capital already exist. Organizations such as Coralus and Civic Square demonstrate what a system can look like when powered by a multi-capital model that fuses trust, learning, creativity, and relationships. Within these alternative systems, new transformation pathways have emerged, focusing on a common vision for regenerative business models at industry scale. Companies, individuals, communities, and entire ecosystems of organizations are coming together to reimagine sectors such as journalism, clean energy, health care, and plastics. Given these examples across nearly every sector, dreaming up alternative ways of running businesses is no longer necessary. Transformation lies in how capital is pooled, stewarded, and allocated toward regenerative businesses at scale.

This is where rewiring wealth enters the discussion. Rewiring wealth proposes that a new generation of wealth holders allocate capital in radically different ways. First, foundations and private family offices would move capital away from VC funds and other traditional asset managers. Instead, capital could be allocated to organizations and ecosystems that have already established transformation pathways to scale regenerative business models. These organizations and ecosystems would become the new asset managers, albeit with collective governance models and identified transformation pathways at their disposal, enabling them to move funds for the purpose of making the biggest societal and environmental contributions.

Second, existing capital models, including impact investing mechanisms, all require that ventures take on funding to pay an interest rate to compensate for the risk that sits with capital holders, according to the current system. This risk, we believe, lies with those undertaking the transformation work of shifting industries away from extraction and toward regeneration. Organizations and communities taking on transformative capital would therefore receive payment for the labor and risk they assume. That’s right: Instead of being extracted from, these entities and individuals would be compensated through negative interest rates.

Third, anyone who has accepted venture funding can attest to how much reporting capital providers require. Impact funds can often be the most cumbersome when it comes to paperwork. An alternative model would be based on trust, and the only prescribed key performance indicators would take the form of a “hope dividend.” As capital enables transformation, each industry will shift toward regeneration in an act that instills hope in every stakeholder. The only return and reporting required for the entrusted capital would be the narrative of hope.

From the perspective of next generation wealth holders, this represents the smartest investment strategy. At the moment, our wealth is depleted by a deepening social and environmental crisis. Institutional investors now recognize systemic risks that can boomerang back to their portfolios owing to climate change, political division, national security issues, or antimicrobial resistance from large-scale industrial farming. Every asset class and sector, from real estate to agriculture to mining, is negatively affected. In 10 years, wealth that now sits in foundation endowments and private family office assets could amount to much less. The only way this trend might be slowed, or perhaps reversed, is if every industry is transformed toward a regenerative business model, thus decreasing the environmental and societal costs. As such, when private family offices and foundations rewire their capital models in the ways we have articulated above, they gain a significant return as the value of their assets depreciates at a lower rate.

In the meantime, seeding transformation pathways will lead to the emergence of new asset classes, for example, civic assets, regenerative soil, and community real estate. Wealth holders who rapidly shift their models toward new capital propositions would see an increase in the value of these assets and their underlying investments.

As such, the three proposed rewiring pathways to capital allocation and stewardship would lead to an alternative system designed with radically different outcomes. This system would benefit all of us and ensure our mutual thriving.

Read more stories by Denise Hearn & Anastasia Mourogova Millin.