At first glance, social impact bonds (SIBs) appear to be an ideology-free response to a range of social problems. As public resources are not always made available to adequately fund public and social services, SIBs leverage private investment to finance such services so that providers do not have to front the cost of delivery. Investors are rewarded if providers meet agreed-upon outcomes but lose their investment if providers do not meet those outcomes. On the face of it, SIBs might seem like a win-win for everyone involved.

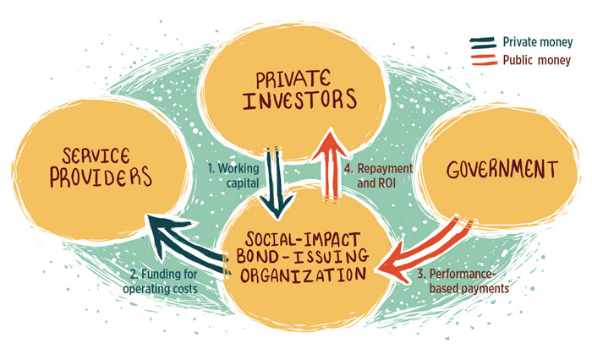

A model of a social impact bond.

A model of a social impact bond.

So it makes some sense that SIBs have become so popular. Since their introduction in 2010, 32 SIBs have been set up thus far in the United Kingdom, addressing diverse policy areas such as homelessness, mental health services, education, and unemployment. The UK Government Cabinet Office has established a Centre for Social Impact Bonds. The government also allocated more than $28 million of public funding to a Social Outcomes Fund in 2012 for the development of SIBs, and augmented this by a further $113.4 million from the UK Government’s Life Chances Fund in 2016—significant amounts of money by any measure. The UK’s Minister for Civil Society has said that SIBs will revolutionize the third sector and social service funding, and that a SIBs market in Britain could be worth $1.4 billion by 2020. Meanwhile, there are at least 10 SIBs operating in the United States and 19 more across 14 other countries, with Goldman Sachs also investing in the model. The development community has also adapted the SIB model in service of so-called development impact bonds (DIBs), primarily for use in the global south.

The ongoing hype around SIBs, their seemingly unstoppable proliferation worldwide, and the significant amounts of money investors are putting into them would suggest that they are widely regarded as the future of impact investing. However, we contend that such uncritical enthusiasm for the SIB model is a worrying trend. There are significant technical challenges to overcome in setting up and operating SIBs, which advocates insufficiently acknowledge. More substantively, however, SIBs fundamentally change the nature of public and social services, effectively reducing citizens to commodities.

Technical Issues with Social Impact Bonds

One rationale for introducing SIBs was that a focus on delivering outcomes would encourage experimentation, thereby stimulating innovation. Conventional public service providers are often criticized as being risk averse and preferring to stick with established practices, while SIBs would lead to new, exciting, and innovative service provision. However, there is almost no evidence that SIBs encourage innovation. In fact, almost all SIB-funded projects are based on well-established models. This should not be surprising: Financiers motivated by a return on investment (as opposed to meeting social objectives) have little incentive to fund risky innovative policy experiments.

The stakeholders who commission SIBs—funders and intermediaries—often assume a substantive role in service design and delivery. As a result, service providers have reported that they have less scope for flexibility than before, and are facing increased oversight and a significantly increased administrative burden.

The complex nature of stakeholders’ contracting arrangements generate considerable transaction costs. In addition, SIBs are technically difficult to commission and require considerable expert input, often (not coincidentally) by the very same experts pushing the model. The scale of operations required to justify these costs means that SIBs tend to be beyond the capacity of many third-sector organizations, such as social enterprises, which tend to operate on a relatively small scale. Few such organizations possess the financial skills or systems required to manage and monitor such investments.

As payment to investors is based on delivering outcomes, contracting arrangements require precise outcome measurement to avoid disputes. This raises numerous issues, including the selection and measurement of outcomes, the attribution of what leads to and who caused changes in selected indicators, and perverse incentives such as “parking” harder-to-serve clients and “creaming” those easier to support. Also, even if it could be proven that SIBs directly contributed to future cost savings, such effects are rarely final outcomes. Rather, they are improvement processes that depend upon sustaining at least some of the effort that brought them about, and not simply cashing out after short-term contractual targets have been met.

The sector might have gained further insight into these issues from the world’s first SIB, at Peterborough Prison, which was originally due to finish last year. However, it was terminated after only three years, due to the introduction of a new national policy. While interim results showed reoffending at the prison initially went down by 8.4 percent, the real success of this SIB is impossible to judge, and issues of attribution remain. This experience highlights another blind spot that seems characteristic among SIB cheerleaders: the determinant influence of the dynamic, extraneous policy environment and political climate on program outcomes.

Qualitatively Changing Service Delivery

These challenges should give SIB advocates cause to reconsider. The fact that they do not take pause reflects the ideological, rather than evidential, basis for SIBs’ popularity. However, we believe of greater concern is the unintentional (or otherwise) effect of introducing the SIB model into the realm of service delivery previously infused with a public-sector ethos. This represents a boundary shift that profoundly alters the character of the service.

The introduction of a profit incentive fundamentally alters the relationship between the service provider and user. The principal client and dominant stakeholder of any given SIB is its financier, not those who receive the services it finances and whose voice rarely figures into any discussion. The motivation propelling private investment in SIBs is profit or return on investment, rather than assisting or changing the circumstances of citizens in need. SIBs reduce this latter feature—which we might regard as the central purpose of social and public policy—to a by-product of investment. This does not seem to trouble SIBs’ many proponents, who blandly assume that the interests of private financiers can be aligned with the needs of service users, and who are content to see the changing fortunes of citizens instrumentalized as payment triggers. SIBs thereby transform citizens into commodities. The inevitably complex contracting arrangements that SIBs entail also transform the nature of policy accountability, with governance and reporting systems geared toward the needs of private funders rather than elected officials. SIBs exemplify the financialization and privatization of social and public policy; they reduce the rights of citizens both as service users and as a polity.

SIBs are undoubtedly an innovative idea. But, leaving aside their considerable technical problems, far more than being a mere technocratic and unideological development, they constitute an ideological shift in welfare service provision. SIBs are both an archetypal “solution looking for a problem” and an illustration of the cultural supremacy of market principles into all aspects of everyday life, including politics and policy.

There are better ways to harness resources for social good. For example, the public sector can still achieve broader policy changes by exercising economies of scale that go beyond the scope of local solutions. The national roll-out of the new recidivism policy that overtook the Peterborough Prison SIB case aptly demonstrated this. With some imagination, we might also devise solutions that are more attuned to underpinning ideals of solidarity and community represented by the third sector. For example, the first Community Bond recently launched in Scotland seeks to attract small scale investments (of around $70 to $7,000) from “community investors” to create a loan fund (of around $105,000 to $140,040), which will look to lend unsecured loans to local social enterprises and community businesses. Such initiatives may be much smaller than a commercial SIB, but they represent a simpler way of increasing and widening sources of finance for public services without sacrificing or altering their essential moral character.

Read more stories by Neil McHugh, Stephen Sinclair & Michael J. Roy.