(Image created by author, using DALL·E 3)

(Image created by author, using DALL·E 3)

Investors have a lot on their plates: inspecting quarterly reports, following market trends, meeting with management teams, sourcing deals, courting potential co-investors, and much more. It stands to reason that investing becomes even more burdensome when it includes dedication to positive impact. Think of all the time and effort that must be spent on understanding social and environmental problems, anticipating potential conflicts between business growth and mission fidelity, and analyzing impact data reported by investees.

Many have recognized this issue of difficulty as a central challenge for impact investing. In a seminal 2009 white paper, the Monitor Institute noted that “the long and difficult work of ensuring investment impact” could stand at odds with “existing financial markets and incentives.” More recently, three London School of Economics academics have highlighted the same tension, citing Confucius’s saying that “he who chases two rabbits catches neither.” “Impact investing is often associated with more expensive, complicated, time-consuming, or incomplete due diligence,” as Francois Botha wrote in Forbes, resulting in the perception of impact investments as “riskier propositions.”

Until now, however, there has been no systematic evidence to determine whether impact investing actually is more difficult than traditional investing. This is an important gap in our understanding of impact investing, including the tradeoffs it might pose and what makes the field distinct. As shown in the excerpts above, there is a presumption that impact investors are shouldering unique burdens to achieve impact, but is this true?

To answer this question, Katherine Klein and I, in collaboration with other members of the Impact Finance Research Consortium, administered a rich, multifaceted survey to over 200 impact fund managers across the globe (particularly in private equity and venture capital). We asked about investor relations, impact measurement, relations with portfolio companies, and, among other issues, the difficulty of impact investing, aiming to dig deeper into more substantive questions of how impact investors carry out their work.

Is impact investing more difficult than traditional investing?

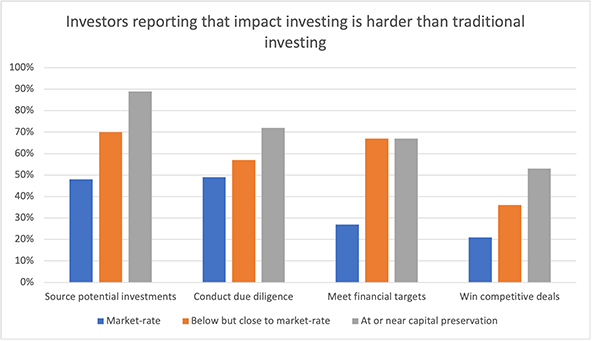

Our survey asked impact investors to report on how their work compares to traditional (or non-impact) investing when it comes to several activities, as shown in the figure below. Respondents could indicate that impact investing makes the activity much harder, somewhat harder, about the same, somewhat easier, or much easier. To keep things simple, I report only the percentages of respondents marking that impact investing makes a given activity somewhat or much harder, and break out respondents by those seeking returns that are market-rate, those that are below but close to market-rate, and those that are at or near capital preservation. We should pay special attention to market-rate investors, as this is the most logical comparison group for traditional investing.

As the graph shows, impact investors seeking market-rate returns reported lower levels of difficulty in impact investing—compared to traditional, non-impact investing—than did impact investors who were targeting lower financial returns. While there was some variation in how difficult market-rate impact investors find their work, most of them reported that they did not perceive their work to be harder than traditional investing across all the activities we asked about.

This is something of a counterintuitive result: Impact investing was consistently seen as more difficult by investors who didn’t need to achieve market returns alongside impact. Shouldn’t it be harder to “chase two rabbits”?

To be sure, a substantial portion of below-market-rate-seeking fund managers also did view impact investing as no harder than traditional investing. However, it is possible that these professionals face unique circumstances tied to their unique (below-market) return goals, such as a different set of competitors and different expectations from limited partners. But the larger point remains: One would expect that impact investors who seek market-rate returns face all the typical challenges of investing, plus whatever challenges come with combatting climate change, closing educational gaps, rectifying racial injustice, and tackling the myriad other entrenched and persistent problems we face. Given that assumption, one could easily imagine that market-rate-seeking impact investors would be more, not less, likely than their below-market-rate counterparts to view impact investing as harder than traditional investing. What explains the opposite result?

Why is targeting lower returns associated with higher levels of reported difficulty?

We explored numerous possible explanations for the pattern shared above. Could below-market-rate impact investors be less likely to have experience in traditional finance and therefore be more likely to overstate differences between impact and non-impact investing? Might market-rate-seeking impact investors ascribe less importance to impact in the investment process? Perhaps below-market-rate impact investors have less capacity—less capital, fewer employees, etc.—and are thus less equipped to deal with the challenges they face?

However, our results do not change even when we control for professional experience, self-reported importance of impact, and fund capacity; market-rate-seeking impact investors still perceive less difficulty in impact investing, compared to traditional investing.

One possible explanation surfaced in separate interview data I collected with Lauren Kaufmann on how impact investors assess social and environmental outcomes. Drawing on 135 interviews with impact investors, we found a clear tendency among market-rate-seeking impact investors in particular to emphasize how intertwined the impact and business models of their investees are, and to presume that the impact of a business necessarily scales with its growth (what impact investors sometimes refer to as collinearity). More specifically, 73 percent of market-rate-seeking interviewees expressed a belief in a strong correlation between impact and financial performance, compared to just 22 percent of interviewees targeting below-market-rate returns.

We further found that the result of this belief is that market-rate-seeking impact investors often also believe that they can gauge impact largely by monitoring the financial performance of their investments, simplifying their work considerably. For example, one interviewee commented that because “our impact strategy is built into the business strategy, we don’t have to try too hard [to measure impact] because it’s already built in.” In contrast, below-market-rate respondents commonly cited their freedom to take lower returns as a reason for their sharpened focus on impact, including assessing and reporting impact underperformance. As one such respondent explained, “we’re particularly rigorous on the impact front because we’re a nonprofit, because that’s our mission.” It seems reasonable to conclude that if market-rate impact investors mitigate the complexity of impact by treating it as something embedded and inherent in business performance, then they enjoy more cognitive license to shift to conventional investing practices focused on financial performance with the confidence that impact remains baked into the numbers.

If these data help answer the empirical question of whether impact investing is harder than traditional investing, however, we’re left with a normative question: Is something amiss if most market-rate impact investors do not find much added difficulty in pursuing impact?

Should impact investing be more difficult than traditional investing?

The lack of reported difficulty I’ve uncovered may be encouraging to field-builders: low barriers to entry promise growth. But it might also indicate that impact investing is not quite living up to its original value proposition, a central part of which has always been the idea that impact investors actively contribute to the impact of their investees. The strong version of that principle, to which I believe the field should aspire, centers on the concept of “additionality,” helpfully explained by Paul Brest and Kelly Born in their much-cited and much-discussed article on impact investing from over a decade ago:

Under our criterion of additionality, the investment must increase the quantity or quality of the social or environmental outcome beyond what would otherwise have occurred—where the counterfactual is that ordinary, socially neutral investors would have provided the same capital in any event. Under the additionality criterion, how can an impact investor expect market returns and still provide [investment impact] to the enterprise? After all, if it’s a good investment, one would expect socially neutral investors to be in it as well.

In other words, for impact investors to have value-added impact, there should be something truly distinct about the deals that they seek out and structure, at least compared to the deals made by socially neutral investors. For those accepting concessionary returns in favor of impact, that criterion is rather easily met, as seeking subcommercial returns is clearly a differentiator. For market-rate impact investors, additionality probably requires an appetite for other transaction costs or market frictions that would normally deter socially neutral investors, such as investing in underserved regions with more challenging business environments or providing more impact-focused technical assistance to investees. Indeed, impact investors’ readiness to accept those costs and frictions is central to the catalytic capital strategy that often sets impact investors apart from their purely returns-focused peers. It is also the reason that Brest and Born argued that “although it is possible for impact investors to achieve social impact along with market-rate returns, it’s not easy to do and doesn’t happen nearly as often as many boosters would have you believe.”

But if most market-rate-seeking impact investors report no added difficulty in impact investing, then it seems likely that many of their deals are similar or identical to ones that any well-trained, profit-driven investor would find attractive. This conclusion accords not only with the interview findings discussed previously but also with a recent study by several Harvard Business School researchers, whose analysis of co-investment networks leads them to conclude that there is “limited support for the assertion that impact investors expand the financing frontier, either in the deal-selection stage or the post-investment stage.” If that is the case, are market-rate impact investors achieving the additionality that constitutes the unique value-add of impact investing?

Ultimately, this question boils down to what the purpose of impact investing should be. At a time when the broader field of responsible investing gains traction among executives and criticism among industry observers, can impact investing be the vanguard of the responsible investing movement or is it meant to be merely a synonym for it?

Given the stakes, I prefer the former. In a time of mounting environmental degradation and runaway social inequality, we need impact investing to be more than traditional investing with an impact report. Impact investors need to address the urgent problems that are currently neglected by capital markets, help their investees to center social impact in their growth strategies even if there are no knock-on benefits for financial performance, and find entrepreneurs from nontraditional backgrounds that mainstream private equity and venture capital players are overlooking. And they should do all that even at the cost of greater difficulty.

If it is to be done well, impact investing should be hard.

Read more stories by Maoz Brown.