You’ve heard it before: Charity doesn’t scale; business does. Social entrepreneurs and impact investors have been hard at work applying business best practices and market principles to some of the world’s most pressing issues—access to finance, water, energy, housing, health, and education—driven by a shared belief that for at least some problems, capitalism can provide an answer to the “problem of scale” that has consistently eluded the grasp of pure philanthropy and aid.

Scale matters because the size of the problems we’re trying to solve are massive: For instance, there are 2.5 billion unbanked people worldwide and 600 million people without access to energy in Sub-Saharan Africa alone.

But as the nascent impact investing industry grapples with the challenges of identifying, articulating, and measuring the scale of impact enterprises and market-based development, we’re worried that we’re focusing on the wrong things. Our collective brainpower is increasingly concentrated on careful accounting of firm-level outputs via systems such as IRIS (particularly the number of customers or households organizations serve) and making causal links between firm actions and outcomes through randomized control trials (RCTs) and other means. In our pursuit of scale as a proxy for impact, we find ourselves chasing boasts like McDonald’s “billions and billions” served. This works if you’re counting hamburgers, or the delivery of products or services by any large and mature entity. Indeed, our field has made immense progress in measuring direct impact; tools like IRIS and GIIRS play an essential role in measuring the reach of larger, more mature firms and investments at the individual firm level. But they are not the best tools for thinking about early-stage innovative firms or the impact of early innovators spurring change across a given sector. In other words, these measures tell only a very small part of the larger story; they miss critical nuance and other ways entrepreneurial innovators change the world.

We believe that there are not only direct pathways to scale but also indirect pathways to scale—specifically, scale through the indirect inspiration or motivation of copycats and competitive responses that build on, extend, and sometimes even replace the initial pioneer. These alternative stories of scale involve systemic-level ripples or “pinballs” sparked by initial innovators; they lead to the creation or growth of “whole new markets” (as Clay Christensen recently described) and unexpected actors that serve the needs of the low- and lower-middle income segments.

In fact, these indirect impacts are often the most important contribution of market innovators in the long term—more so than the direct customers they serve on their own in their early stages. But, as one of us argued recently, we still haven’t found effective ways to talk about or measure these contributions. And if we don’t tell these more-nuanced stories, we risk underinvesting in game-changing innovations, missing opportunities to give entire sectors (such as financial services) much more exciting—and impactful—trajectories.

As background, both Omidyar Network and Accion Venture Lab (our respective organizations) invest in firms globally at very early and high-risk stages of their life cycles—usually with some revenue, but well before breakeven and often in risky markets across Africa and Asia. Over time we’ve learned that there’s a long, nonlinear thread that runs between an early-stage investment and its eventual social impact. Firms fail. Firms succeed but run into massive established incumbent competitors. Firms pivot business models four (or more) times and eventually get it right, but don’t necessarily serve billions or even millions in their early stages—or ever.

Omidyar Network started looking at this issue in 2012 in its “Priming the Pump” series, which argued that social impact at scale requires more than just great innovative firms; it requires addressing an entire sector and its ecosystem of actors, including the market innovators and scalers, as well as other determinants of success such as regulators and infrastructure providers. Market creation is the work of many, rarely just one. Most cases of social impact at scale emerge from contexts with multiple firms and actors—microfinance, mobile money, and contract farming, for example, involve dozens or even hundreds of firms, all contributing to the creation of their respective markets.

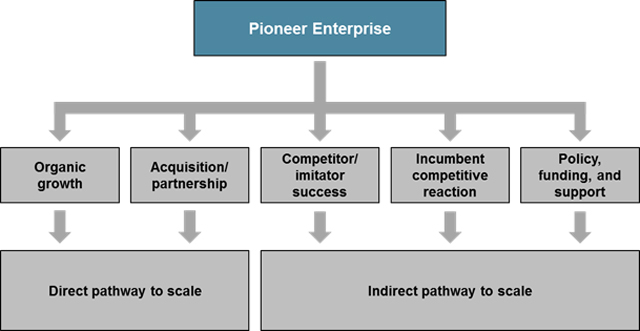

There are five pathways to impact at scale, only two of which rely on direct scaling of the original innovative firm.

There are five pathways to impact at scale, only two of which rely on direct scaling of the original innovative firm.

We see five routes to scale for those starting with early-stage innovators. But only two of these paths involve the initial firm delivering at scale (i.e. direct scale). The other three are variations in the way an initial firm can cause or contribute to scale beyond the immediate sphere of its operations (i.e. indirect scale).

Direct Pathways to Scale

First, the most obvious one: A company can grow big independently. This is the most direct path for a startup’s innovation to scale: to pioneer, prove, and scale all on its own. In the mainstream world, think Google and Facebook. In the impact world, think Compartamos (controversy aside), and perhaps d.light or Microensure. This pathway is the gold standard and has a number of obvious benefits as an impact story: The company retains its vision and mission, and will likely provide healthy financial returns for investors and managers alike (which can attract talent and further capital to the sector). It’s also, not surprisingly, often the hardest. As investors, our clear preference is for this first pathway to scale—the financial returns align well with the social returns as the enterprise grows to scale—and in all instances, we are passionate about helping entrepreneurs build great businesses, and we work like hell to ensure that our portfolio companies grow, expand, and succeed.

Second, a firm can achieve scale directly by innovating a new model, and then having an acquirer absorb and extend it—often with dramatically more financial, marketing, distribution, and brand muscle. Think here of Banco Bilbao Vizcaya Argentaria (BBVA)’s recent acquisition of retail bank innovator Simple; Coke’s and Starbucks’ purchases of Honest Tea and Ethos Water, respectively; or SABMiller’s purchase of Voltic and its base of the pyramid-focused CoolPac water sachet business in Ghana. In these instances, a new entrant proved an initial inspiration, but grew it in a new home and (sometimes) with a new brand and identity. This pathway to scale often turbocharges growth with access to new multinational resources, distribution points, and deep pockets; it can also lead to high enough returns to attract others into the market. (There are, of course, always risks that the initial idea and mission, once absorbed into a corporate machine, gets lost in the shuffle, resulting in reshaped technology or products that may not be aligned with the original, underserved market. The Consultative Group to Assist the Poor’s (CGAP’S) recent focus note, “The Art of the Responsible Exit in Microfinance Equity Sales,” explores this theme well.)

These are probably the ways most people think of a financially successful startup: Either grow big on your own or have someone else snatch you up. But these two paths are just scratching the surface.

As impact investors, we should think about success and impact more broadly than one firm’s performance. This more holistic field-building perspective reflects broader thinking about innovation from economists like Paul Romer and others. Romer suggests that successful innovators usually capture only a small fraction of their work’s benefits. This creates a market failure; potential innovators in both the private and public sectors do not have incentive to make socially beneficial investments. This leads to an underinvestment in innovation—especially social innovation. Our industry, so long as it considers only the direct outputs of impact enterprises, risks playing into this market failure and underinvesting in market-creating innovations that can generate public goods and shared intellectual capital, and ultimately take others to scale.

Indirect Pathways to Scale

One indirect path to scale is to inspire copycats—either a new entrant, or an existing player launching a new product or business line inspired by and based on the experience of the initial innovator. Examples include mobile money deployments springing up in the wake of M-PESA; the global microfinance movement, with dozens of successful institutions launching as pioneers Grameen, BRAC, BancoSol grew to scale; M-Shwari learning from the experience and idea of Jipange Kusave in Kenya; Eureka Forbes setting up more than 100 rural water kiosks after seeing the potential of WaterHealth International and Water Life (among others) in India; and Hertz’s entry into the car sharing business following Zipcar’s success.

Another indirect path is to motivate a competitive response by compelling an existing player to do something differently in a way that creates surplus value for the end customer. This could take the form of a defensive response (such as lowering prices) or a desire to capitalize on a never-before-recognized opportunity (such as using a new technology to develop a new service). One compelling example is Honest Tea’s introduction of a lower sugar juice pack for kids, which spurred category leader Capri Sun to reduce the calories in its classic formulation by 25 percent. The result was healthier products for more children. Likewise, companies like Cignifi and First Access have inspired mobile operators and other financial service providers to build their own in-house capabilities to analyze and use previously ignored cell phone data for credit assessment and financial services, creating benefits for customers (in terms of access and pricing) that extend far beyond the immediate reach of the initial innovators. These examples show ways an initial pioneer can spark changes in the way business is done and products are offered, at scale, well beyond the immediate reach of the pioneer’s business activities.

Time from start of operations to operating break-even microfinance lenders. (Image from “From Blueprint to Scale: The Case for Philanthropy in Impact Investing”, by Harvey Koh, Ashish Karamchandani and Robert Katz, April 2012)

Time from start of operations to operating break-even microfinance lenders. (Image from “From Blueprint to Scale: The Case for Philanthropy in Impact Investing”, by Harvey Koh, Ashish Karamchandani and Robert Katz, April 2012)

But let’s be honest: This is not what a frontline manager or investor wants to hear: Inspiring an established incumbent with deeper pockets, more market power, and other competitive advantages to compete against a startup doesn’t always work out well for the startup. But if impact investing is as focused on doing good as it is on making money—and it should be—then we have to acknowledge that even this “unbalanced” competition is potentially a success as long as it translates to something better for the customers themselves.

Pioneer firms can also motivate external changes that make it easier to scale impact. For example, when a new entrant reveals gaps in how organizations currently do business, it compels those organizations to address them, including philanthropists and governments who can step in to fund public good infrastructure. These gaps can include:

- A general lack of market or customer knowledge (for example, branchless banking innovators in Latin American and the Philippines drove CGAP’s early work assessing the market potential, customer needs, and preferences)

- A lack of customer awareness (Envirofit’s struggles motivated Shell Foundation’s public service campaigns in India explaining the harmful effects of indoor air pollution caused by inefficient cookstoves)

- A lack of quality industry self-regulation standards ensuring responsible and customer-friendly growth (MFIs’ work around the world drove the Smart Campaign to articulate and drive consensus around shared global standards for customer protection in the provision of financial services).

Similarly, a pioneer firm may promote indirect impact by influencing policy. When new entrants shake up existing industries, they typically expose ways that existing regulations aren’t up to the task. Innovations may fall victim to regulatory barriers erected for another time and place, often in unintended ways. Likewise beneath-the-radar startups may become collateral damage of policies or regulations written without full consideration of the needs of the “little guys” who don’t have the resources to support lobbying or policy advocacy efforts. Startups too often find themselves in the role of a coal mine canary, informing us whether a particular environment can sustain life—and if not, what will need to change to support a similar effort.

Why we don’t talk indirect impact, and what we can do about it

Inspiring copycats and motivating competitive responses, as well as ecosystem effects around public goods availability and policy change, can be very powerful paths to scaling impact, but we very often ignore or discount them. Why?

First, there is the obvious issue of perceptual salience—quite simply, these impacts are hard to see. When a company grows big on its own, its name becomes widely recognized as the progenitor of scale. But when a company scales through other pathways, we quite simply may not be aware of the original spark or “pinball”. Indirect paths to scale are particularly nebulous, nonlinear, and slow-burning.

Second, there are a number of practical challenges around measuring indirect impacts. Indirect impact trajectories are often hard to map ex ante, because it’s not clear beforehand who will react in what ways. Without knowing ahead of time what to expect, it’s hard to put in place a framework to measure outcomes. For instance, both eBay and PayPal have made huge impacts on modern e-commerce and payments. A very prescient person may have predicted this ex ante, but we doubt that same person could have predicted the rise of the well-chronicled “PayPal Mafia”—the early PayPal founders and employees who went on to start other iconic startups in the US tech ecosystem, such as LinkedIn and Tesla Motors.

And then there’s the elephant in the room: We want to measure firm-level metrics because we want to understand how well our investments are doing. For investors and pioneers, indirect paths to scale through copycats and competitors are irrelevant at best and antagonistic at worst. Managers and investors alike are not and cannot be indifferent to the results of indirect scaling; we stake our reputations and professional livelihoods on the success of the particular firms we lead or fund, not the success of the sector at large.

Let’s be real: In our dual roles as investors and field-builders, it’s nice to consider ways our companies can generate indirect benefits, but never in a manner that would be detrimental to our portfolio companies (to whom we owe our first and highest loyalty) and never as an excuse for poor company or fund performance. Right now, it’s complicated and a bit nebulous; as such, it’s probably up to the intermediaries, investors, and impact funders (rather than the startups) to lead the charge, as they have the appropriate incentives and access for such work but will be less exposed to the risks of replication and competition, and can thus encourage and assess the growth of sectors on the whole.

Of course, we’ll need a different way of talking about and measuring indirect impact. This will require getting comfortable with 1) much more contribution-based and less attribution-based assessment of impact in the field, and 2) taking a longer view, particularly for start-up ventures. Put differently, instead of focusing on making a rigorous, direct attribution of a given early-stage enterprise to reducing poverty, we ought to spend more time figuring out how to think about the contribution—in the form of both expected and unexpected ripples and “pinballs”—that a given firm has made to advancing change at the sector level.

This might be difficult in a world still focused on firm-level effects and tools like randomized control trial-based (RCT) attributions. There’s a time and place for RCTs, which can be extremely useful in the right settings, and more nimble “A/B testing” should be a part of any iterative product or business development process, but tracing the impact of early-stage innovations and sector-level indirect impacts will require new tools. Such an expanded view undoubtedly will create a challenge for impact measurement specialists and demands a high tolerance for fuzziness, but it’s a project which that we feel is worth taking on.

Finally, investors often downplay instances of indirect impact or paths to scale because it forces us to acknowledge and discuss failure. The growth of the sector can have direct and detrimental consequences for the growth of the initial firm—and sometimes leads to the exit of the inspiring firm altogether. Being open about these failures is extremely challenging. Failure is messy—sometimes startups persist in a zombie state for years, hammering on the same idea or pivoting to new opportunities, all the while keeping up appearances for the sake of customer and investor confidence.

There’s no easy answer here, for sure. However, perhaps we can learn from Silicon Valley, where failures are expected and accepted, and can be harvested for lessons, talent, and insights to help do better next time. We should all—including donors contributing to impact investing—expect and tolerate a certain level of failure, and learn from it. We should think of startups not only as vehicles to deliver impact according to an ex ante results framework, but also as real-time experiments to generate knowledge and spark unexpected public good spillover effects.

As we pioneer new ways to channel capitalism to address the needs of the bottom of the pyramid, let’s ensure that we are consciously seeding promising start-ups and innovators that will create impact along pathways both direct and indirect. In doing so, we will prepare the ground for the next wave of breakthroughs and social change at scale.

We would love to start a conversation here and crowd source other examples of indirect impact. We welcome your comments and a robust discussion.

Read more stories by Mike Kubzansky & Paul Breloff.