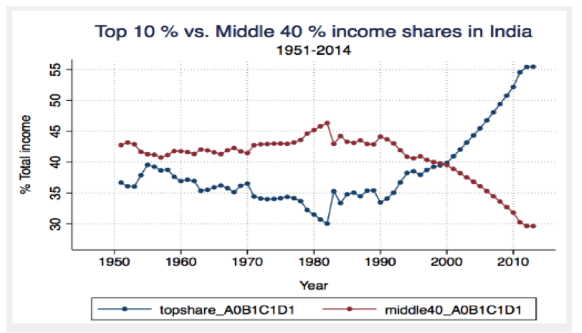

I often start the first-year managerial economics classes I teach by showing a graph to my MBA students (see below).

It shows that in 1951, middle-income Indians (from the middle 40th percentile, leaving out the 30 percent at the top and bottom) earned about 42 percent of the country’s total income, whereas in 2014 they earned only about 30 percent. In contrast, the percentage of income share of the top 10 percent of Indians rose from 35 percent in 1951 to 55 percent in 2014. This evolution toward acute inequality is now well documented—not just in India, but globally.

The question I ask my students after they see this graph is whether companies have any role in solving this growing inequality. The answer divides the class. Social welfare-oriented students start highlighting the role of stakeholder orientation (how much a company attends to its full range of stakeholders, including customers, competitors, employees, and shareholders) and business models focused at the base of the pyramid. Free-market proponents argue that the objective of companies is to maximize profits, citing troves of evidence for shareholder (vs. stakeholder) orientation that point to enhanced profitability, productivity, and survivability. The shareholder-focused company view usually prevails in these classroom debates.

(Image courtesy of Chancel and Piketty, 2017)

(Image courtesy of Chancel and Piketty, 2017)

However, other studies have indicated that there are important market benefits to the stakeholder orientation, including greater employee motivation, enhanced channel relationships, higher consumer loyalty, reputation spillovers from corporate community involvement in the ecosystem, and sustainable business operations in the long run. Extending this line of thought, and building on the work of R. Edward Freeman and other scholars who espouse this approach, a recent report I coauthored with Arzi Adbi and Ajay Bhaskarabhatla presents some early empirical evidence from developing economies showing that the entry of stakeholder-oriented companies into the market impacts market dynamics by influencing pricing and product differentiation norms. The report, which focuses on Indian pharmaceutical companies, also illustrates the potential for the approach to improve consumer access to products, in this case medicines.

As an example, the market entry of the stakeholder-oriented company Mankind Pharma, which started selling medicines to consumers in non-urban India in 1999, caused incumbent companies already selling the same product at the highest price points to reduce product prices and package sizes. We also found that existing companies selling the same product at lower price points tried to signal that their products were high quality by increasing their prices and package sizes. Finally, we found that stakeholder-oriented business models sometimes identify and realize synergies with relatively untapped stakeholders. Part of Mankind’s success in improving consumer access to its products was finding ways to partner with general physicians in non-urban India—a group that Indian pharmaceutical markets often overlook.

As a robustness check, we also conducted a study comparing incumbents’ behavior to the entry of low-cost, profit-maximizing companies, such as Cipla—an Indian pharmaceutical company well-known for its Walmart-like, low-cost disruption of HIV medicines markets worldwide. The results show that incumbents’ behavior in response to the entry of these types of companies is not the same as it is in response to the entry of stakeholder-oriented companies like Mankind. For example, Cipla’s engagement with general physicians was far less active in non-urban India, and when it entered the market, established companies at the high end of the price distribution did not react as aggressively with decreases in price and package sizes.

Given all of this, the potential for stakeholder-oriented businesses to make markets more competitive and serve previously overlooked customers seems high—and not just in India. The Chinese company Haier, for example, is using this approach to successfully sell washing machines and consumer durables to previously underserved customers. However, for the approach to gain greater traction, it's important to consider its limitations and challenges.

Generalizability and scalability

First, it remains to be seen whether the same results would occur in market contexts where social returns may be higher than private returns—for example, in areas such as financial inclusion, affordable housing, and affordable education. The expansion of business models like microfinance (such as Grameen Bank’s) from poor economies into wealthy ones have been few and far between. And in the Indian context, although enterprises like Aravind Eye Care System or Jaipur Foot are positively impacting the affordability and distribution of health-related services, they continue to find it challenging to scale and replicate their local business models to global contexts. The Tata Group offers another example. For a century, the company has advocated for greater economic equality, but its now-famous Tata Nano experiment to bring affordable cars to the global and the Indian middle classes has so far been unsuccessful.

Ownership Structure

Meanwhile, the ownership structure of companies—whether they are privately owned or publicly listed or take some form in between—may influence the extent to which those companies reflect and sustain stakeholder-orientation in their actions. Shareholder pressures, for example, can generate tensions between short- and long-term objectives. Shareholders may be less willing to accept a stakeholder orientation for a publicly listed company than for a founder-driven or a social mission-driven company. Empirical evidence for whether or not the public listing of stakeholder-oriented companies has an effect on their social orientation is limited. This question and others related to ownership structure are worth examining carefully across markets and economies going forward.

Institutional strength

A third consideration derives from the strength of existing institutions or changes in regulations. If a company with a stakeholder orientation is working in a market such as housing, finance, health care, or education, there is a danger that a strong, established institution (say charter schools) may take over the market, rendering the services or products of the stakeholder-oriented company less valuable.

Consumers’ taste for quality

Finally, to stay competitive, stakeholder-oriented companies may need to deal with consumers’ increasing desire for higher-quality goods. Once new customers are exposed to, say, a no-frills washing machine or a slightly lower-dose medicine from a stakeholder-oriented company, they may begin demanding products with more features. How customers’ taste for quality will evolve and how companies can effectively respond remains unclear.

Much more research remains to be done therefore before the field can robustly establish the social welfare-enhancing role stakeholder-oriented companies can play in markets across economies. For business leaders and others who believe that companies and markets have a pivotal role to play in solving the modern world’s inequality issues, supporting both quantitative and qualitative studies that investigate these questions will help develop our understanding of the viability and social impact of new business models. For companies, entrepreneurs, and managers, the stakeholder-oriented approach is a reminder that engaging with a wider range of stakeholders can open up new markets, increase consumer access to products or services, and create reputation spillovers for businesses—not to mention enable deeper channel relationships and trigger more sustainable business operations over time. For companies like Mankind or Haier, the next challenge will be to scale beyond local climes and make stakeholder orientation a more-accepted way to do business globally.

Read more stories by Chirantan Chatterjee.