The sustainability disclosure space has experienced significant changes over the past several years, most notably a movement toward integrated reporting (IR). Led by the International Integrated Reporting Council (IIRC), integrating reporting encourages companies and organizations to take a holistic view of reporting performance, including risks and opportunities pertaining to six categories of “capitals”: financial, manufactured, human, intellectual, natural, and social. As a true thought leader in the space, the IIRC convened a pilot program, consisting of more than 85 businesses and 30 institutional investors, to test principles, content, and the practical application of IR processes, which it sees as the “next step in the evolution of corporate reporting.” The IIRC is set to release its first version of the Integrated Reporting Framework in December.

So why is it important to take an integrated approach to financial and non-financial performance reporting? And does it simply mean that companies will start producing gargantuan reports with overwhelming amounts of information for investors and stakeholders?

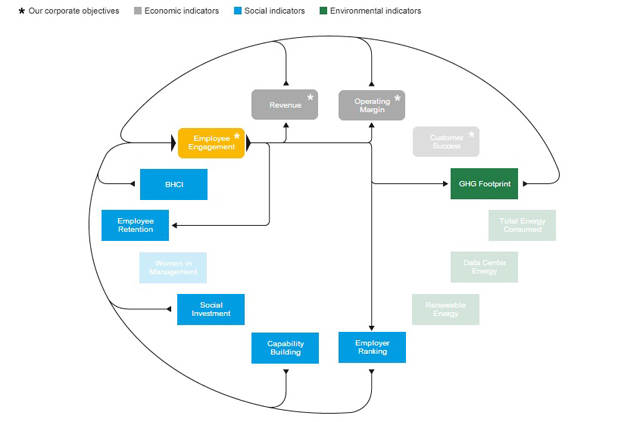

At SAP, a member of the IIRC’s pilot program, we see integrated reporting as a way to reframe how our customers can approach problems and create solutions that move beyond improving efficiency, and support transformational change. An integrated report both facilitates and reflects this new way of thinking about value creation. Most importantly, the integrated approach to reporting allows us to highlight the dependencies between financial and non-financial performance more easily, particularly since many of SAP’s non-financial performance indicators impact important business objectives.

Integrated reporting is based on the idea that a full picture of a company’s performance must include its social, environmental, and economic impacts. These realms are intrinsically linked; actions taken in one area affect another.

At the launch of SAP’s 2012 integrated annual report recently, SAP’s Chief Accounting Officer Christopher Hütten and I were joined by leading thinkers and experts such as Paul Druckman, CEO of the IIRC, and Aman Singh from CSRWire, to explore the benefits and challenges of taking on such a comprehensively integrated annual report. While it was certainly a substantial undertaking, the report highlights in great detail the important connections between financial and non-financial performance.

For example, SAP has avoided the cost of more than $285 million since the beginning of 2008 by becoming more energy efficient (in comparison to a business-as-usual extrapolation based on the number of employees). Additionally, we found that an increase or decrease of one percentage of SAP's employee retention rate will either save or cost the company approximately 81 million dollars, underlining the effect employee engagement initiatives can have on the bottom line.

These links are important to understand, and they help quantify the multi-dimensional value that specific activities can create: For example, in just one year, an internal ride-sharing software developed by SAP for employees in Germany generated more than 22,500 carpools, saving more than 500,000 kilometers of driving and creating an additional 1,400 days of internal networking among employees—all while keeping 47 tons of greenhouse gas emissions out of the air. SAP has estimated the value of this software through cost savings in company sponsored commuter fleet programs and travel, networking, and emission reduction, totaling over 3 million dollars in the first year. The journey continues as the software now becomes available as a service to customers.

When these kinds of relationships appear between financial and non-financial indicators, they do more than make the business case for sustainability. Ultimately, integrated reporting becomes a catalyst for a deeper understanding of how a company can create value now and how it will have to transform in the future.

As the global business and economic landscape changes, shareholders and stakeholders alike now demand more information to effectively evaluate a company’s performance, both financially and in their ability to truly create value. Considering financial results alone does not adequately capture a company’s ability to respond to business challenges. An integrated approach to reporting helps navigate the increasingly complex social, environmental, and economic contexts in which we all live and operate. This is not only relevant to companies, but certainly also to their customers.

Read more stories by Peter Graf.