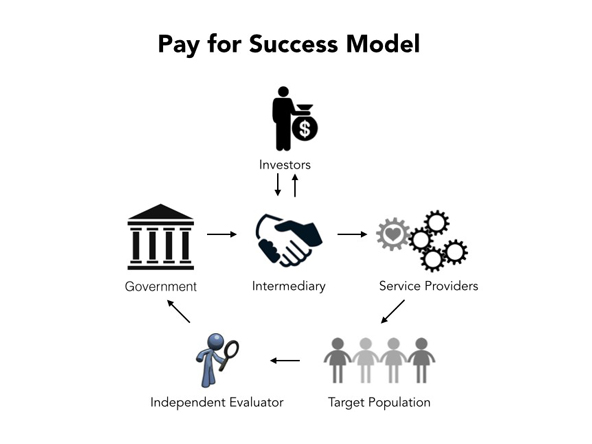

Most social impact bond (SIB) contracts include investors, intermediaries, service providers, and the government payor. The target population should be full partners on any project, while the role of evaluators differs widely between countries. (Image courtesy of USC Price Center for Social Innovation, adapted from the GAO, 2015)

Most social impact bond (SIB) contracts include investors, intermediaries, service providers, and the government payor. The target population should be full partners on any project, while the role of evaluators differs widely between countries. (Image courtesy of USC Price Center for Social Innovation, adapted from the GAO, 2015)

In 2017, Los Angeles County launched its first social impact bond (SIB). The Just-in-Reach project aims to improve the outcomes of a high-needs population—people with a history of mental illness or substance abuse coming out of prison—and determines success by the rate of housing stability and a reduction in recidivism. Even with the abundance of staff, funding, and legal support that the SIB partners—the County of Los Angeles, United Healthcare, and the Conrad N. Hilton Foundation—brought to the table, the contract took more than six years to develop.

The SIB model for commissioning social services is costly and complex, yet it has generated considerable enthusiasm on both sides of the Atlantic. Over the past few years, we have been examining the emergence of SIBs in the United Kingdom and elsewhere, with the aim of not only gleaning early lessons, but also understanding theoretically how SIBs fit into broader institutions of social change, why and how SIBs are evolving, and whether they can achieve their promise.

There are a wide variety of reasons why governments around the world and their partners choose SIBs to address particular social problems, including deferring payment, risk shifting, and facilitating social innovation. Understanding their different goals can help other practitioners determine whether developing an SIB is the right approach for them and, if so, what practical framework might work best.

Differing Theoretical Frameworks

Our research suggests that SIBs fit within three (not mutually exclusive) frameworks that connect to evolving theories on the provision of public goods and services, and that have different accountability structures.

New public management (NPM). Policymakers and researchers tend to think about the SIB approach to delivering public services as informed by, or an extension of, the new public management framework. This framework incorporates three integrating forces—markets, managers, and measurement—with the aim of generating more efficiency and accountability in the provision of public goods and services. Given SIB’s reliance on up-front investment and predetermined outcomes—versus a focus on measurement activities and inputs—a SIB contract is conceptually an extension of NPM.

Management of risk and complexity. Technological change and globalization—as well as increasing public demands on political representatives for more results-driven investments and greater accountability—have reduced many policymakers’ appetite for riskier public investments. Instead, they transfer both financial and political risk to third parties. In this respect, the SIB investor market in the United States has evolved even more than in the United Kingdom; deals in the United States routinely involve multiple investors with different risk preferences and expectations for return. Some US SIB contracts, such as Project Welcome Home in Santa Clara County, California, have as many as five investors.

Speed the process of social innovation. A third framework through which to understand SIBs is their supposed ability to improve the rate of social innovation. In the United Kingdom, it has been argued that private-sector providers of existing services may be more innovative than public providers. In the United States, by contrast, SIBs have typically been used to scale up promising pilots financed by the public sector or philanthropy.

Different Practical Approaches

These ways of looking at SIBs have translated into a variety of practical approaches. Here’s a look at how SIB markets in the United Kingdom, Finland, and the United States are currently developing in different ways and with different aims.

1. In the United Kingdom, much of the initial impetus for SIBs came from central government, which placed emphasis on: introducing new providers, stimulating innovation, transferring risk, and cost-cutting. As noted by the UK’s National Audit Office, the government placed relatively less emphasis on rigorous evaluation of program impacts. Its All About Me, a bond that seeks to match hard-to-place children with adoptive families, includes no evaluation of implementation or impact. Based on the characteristics of the children and the general rates of adoption, it was unlikely that the cohort would have been placed in a home without the intervention. Therefore the Cabinet Office assumed that “none of the cohort would have been placed without IAAM, and deadweight is therefore nil.”

2. In Finland, the Finnish Innovation Fund Sitra’s stated rationale for introducing SIBs was that the model had the potential to facilitate systematic change in public sector management by re-focusing public resources for workforce development away from measurement of inputs, and toward the acquisition of results and impact. Sitra’s Koto-SIB, which focuses on improving employment outcomes for refugees, exemplifies this shift, as instead of measuring short-term job placements, it measures the long-term earnings growth of participants.

3. In the United States, SIBs have focused on shifting risk to investors and speeding up the rate of social innovation. The attraction of SIBs to multiple investor types demonstrates the sophistication of the risk-sharing arrangements that have developed. SIBs have also been used to scale up promising pilots and have required rigorous evaluations to determine the efficacy of each program. The Just-in-Reach SIB in Los Angeles County we mentioned at the very beginning of this piece, for example, scaled an existing program by distributing risk between the Conrad N. Hilton Foundation, which views its contribution as a 0 percent loan to be paid back if the program is successful, and United Healthcare, which anticipates an expected return of 7 percent.

Risks and Opportunities

Analysts who assess the impact of an SIB through a single framework risk drawing faulty conclusions about whether using an SIB contract is worth the upfront transaction costs. For example, if the goal is public sector reform, then a narrow focus on the singular program outcomes the SIB finances will miss the broader system impacts. If the goal is to defer payments and shift political risk, then the standard program evaluation framework is inappropriate, because the goals go beyond the program outcomes themselves.

The same goes for opportunities. For example, if the goal is to diffuse social innovation more rapidly, then stakeholders can contextualize high transaction costs as a payment for innovation and development. Meanwhile, if a government agency wants to reduce exposure to political risk, then the process of creating an SIB should be transparent and should demonstrate to the public at large that the interventions are cost effective, and by extension, a legitimate use of public funds.

Navigating SIB Development

It may sound obvious, but appropriately spelled out goals, evaluation, and transparent contracts can go a long way toward addressing these risks and taking advantage of opportunities. We suggest the following strategies to guide the successful development and evaluation of SIBs:

1. Goal alignment. The Utah High Quality Preschool Program, which seeks to improve kindergarten readiness in support of long-term educational outcomes, is a good example of why goal alignment matters. The program generated controversy among some policymakers and observers for two reasons. First, the vast majority of the projected savings for government went to the investors. Second, the outcome measure—reductions in the need for special education and remedial services—was a proxy for the ultimate goal of higher graduation rates. Careful consideration of whether the goal was to identify savings or scale a promising pilot would have helped dispel this controversy.

2. Evaluation of both services and SIB mechanisms. Although several SIBs in the United Kingdom have included no evaluation, in the long run, rigorous evaluation is important for building credibility for investors. Many SIBs in the United States have commissioned randomized controlled trials (RCTs) focused on whether the services investors funded delivered the intended outcomes. But while RCTs are good at identifying whether, for example, a program that serves homeless people increases participants’ retention of housing, they can tell us little about the relative merits of using an SIB rather than another financing mechanism to pay for the program. The field needs qualitative, process evaluations to evaluate the SIB mechanism itself. Since the goals in many contexts related to changing the focus of government from measuring the number of clients served to a set of outcomes, it is critical to understand whether that shift did take place.

3. Co-creation. SIBs like Duo for a Job in Belgium and those in Santa Clara County, California, have shown much promise in changing systems because of deep stakeholder involvement. But while there is a strong focus on co-creation (working with users of services and citizens to co-design services that fit their needs) in UK public service reform, it is often missing in the construction of SIBs. If SIBs are to reach their full potential and avoid being at odds with the wider public service reform agenda, they need to build in elements of co-creation from the start.

While there is no singular framework through which to understand SIBs the strategies above may help governments and their partners better weigh the risks and opportunities associated with the tool. SIBs are not a perfect financing mechanism for all social services, but they deserve additional research and experimentation.

Read more stories by Gary Painter, Kevin Albertson, Chris Fox & Chris O’Leary.