(Illustration by Joohee Yoon)

(Illustration by Joohee Yoon)

In April 2012, UK Prime Minister David Cameron launched Big Society Capital, a £600 million bank that aims to help grassroots charities and social enterprises by supporting intermediaries, such as venture philanthropy organizations, that provide the charities and social enterprises with finance and support. In its first tranche of funding, Big Society Capital provided £450,000 to a joint project of ThinkForward Social Impact and Private Equity Foundation to create a social impact bond to finance intensive school-based support programs to help disadvantaged young people living in the East End of London.

In 2010, Spain’s second largest bank, BBVA, launched a venture philanthropy project called the Momentum Project in partnership with the Barcelona business school ESADE and the Spanish PwC Foundation. The Momentum Project supports Spanish social businesses with an intense program of mentoring, courses at ESADE, and loans. The project has gone far beyond a simple corporate social responsibility (CSR) initiative, drawing in several departments within the bank and creating a new impact investment product for private banking clients. The project has become so popular within BBVA that it is being replicated internationally. There is now a Momentum Peru and a Momentum Mexico.

Venture philanthropy has even reached small towns in Sweden. Lindängen is an area with roughly 7,000 inhabitants in the borough of Fosie in Malmö, with tower-block apartments from the 1960s and 1970s in need of far-reaching refurbishment. Worse, the neighborhood has unusually high rates of unemployment and child poverty. The City of Malmö is considering a new program that aims at reusing social expenditures in a social invesment approach to refurbish the buildings and work with the inhabitants to enhance education, social cohesion, employment, and leisure opportunities in the neighborhood, while reducing the environmental impact. Bjarne Stenquist, from the City of Malmö’s environment department, is creating this as an area-based social investment fund for social and environmental sustainability that would bring together the private, public, and civic sectors in an impact-investment approach that could be used in other neglected areas.

These and similar activities across the continent suggest that the future for European venture philanthropy is bright. Having started in the early 2000s in the UK private equity and venture capital world, venture philanthropy then seeped into foundations across Europe. More recently it has spread as governments and corporations begin to inject significant capital into the field. With the growth in popularity and practice of social enterprise in Europe, and the fit between social entrepreneurs’ demand for flexible financing and openness to business support with what venture philanthropy has to offer, European venture philanthropy may be on the verge of growing from a noisy niche into an integral part of the broad philanthropic and socially responsible investment field.

Although venture philanthropy is poised to grow in Europe, it will not necessarily be under the banner of venture philanthropy, nor will it be undertaken primarily by dedicated venture philanthropy organizations. Instead, many of the programs are likely to be undertaken by traditional foundations, corporate philanthropy, public policy initiatives, and impact investors. This is not a bad thing, but it does mean that venture philanthropy may assume a different character from that in other parts of the world, particularly in the United States. One of the differences that has already emerged is that venture philanthropy in Europe is much more diverse than it is in the United States.

Although there is much to be encouraged about, we also see reasons to be cautious. One of the biggest risks to the growth of European venture philanthropy is that the amount of funds going into the field may continue to tighten because of Europe’s fiscal problems. Venture philanthropy is still in its early stages, and a prolonged period of restricted funding could cause the approach to falter before it has a chance to embed itself.

Ironically, those same fiscal problems may have the opposite effect, spurring government to look to venture philanthropy as an alternative way to tackle social problems. Instead of relying on the traditional social democratic or welfare model of funding and operating social services, governments throughout Europe are now actively experimenting with models based on social enterprises and social entrepreneurs. These new government approaches, combined with the growth of private venture philanthropy, may set the stage for significant changes in the European social landscape.

What Is Venture Philanthropy?

Before we dive into the state of venture philanthropy in Europe, it’s important to be clear what we mean by the term. There is no single global definition of venture philanthropy, and its definition has evolved over the years along with its practice. In Europe, venture philanthropy has taken on different forms in different countries, each with its own unique set of laws, institutions, culture, and history.

The practice of venture philanthropy can differ quite substantially from organization to organization, but a set of important characteristics1 distinguishes European venture philanthropy from other types of philanthropy and social investment:

Indeed, unlike in the United States, where most venture philanthropists are engaged in grantmaking to nonprofits, more than 50 percent of those practicing venture philanthropy in Europe do so using debt or equity rather than, or as well as, making grants. And many European venture philanthropists support social enterprises and businesses rather than charities.

European Philanthropy

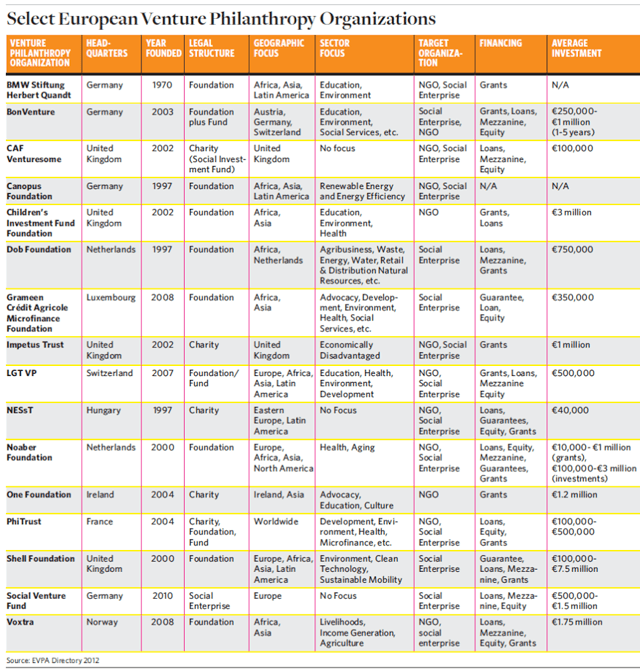

Throughout Europe, philanthropy plays a much smaller role in society than in the United States. In Europe, philanthropy makes up only 0.1 percent to 1 percent of GDP depending on the country, compared to 2 percent of GDP in the United States. And venture philanthropy is just a small part of overall European philanthropy. The 2012 EVPA Industry Survey, conducted by the European Venture Philanthropy Association (EVPA), revealed annual expenditures of €278 million by 61 European venture philanthropy respondents, only a fraction of the total European foundation expenditures of €46 billion by 60,000 foundations.2 All told, we estimate that there are between 80 and 100 venture philanthropy organizations in Europe and a larger body of interested organizations. (See “Select European Venture Philanthropy Organizations” below.)

European philanthropy is a fragmented and varied phenomenon, with significant differences between nations. Each country has its own historical, cultural, and social conditions, different legal frameworks and regulations, and differing levels of government involvement in the social sector. Taken together, this variation has resulted in a wide spectrum of philanthropic activity.

An insightful way to think about the types of European philanthropy is to group them into four different models, each based on the scale of the social sector and its relationship with the government:3

Liberal model (United Kingdom) | The social sector is relatively large, accounting for more than 5 percent of total employment, and focused mostly on providing services, particularly in education, health, and social welfare. Although the social sector receives about half its funding from government contracts, for historical reasons it is largely independent of government control. The social sector also receives a substantial amount of income from fees and charges. Only a small portion of funds comes from private donations and grantmaking foundations. UK philanthropy has a strong and vibrant tradition, ranking number one in Europe as a percentage of GDP.

Welfare partnership model (Germany, Netherlands, Belgium, France, and Spain) | The social sector is large, accounting for more than 5 percent of total employment, and composed mainly of organizations providing services. The sector is dominated and subsidized by the government, which spends a great deal of money on social welfare programs and accounts for well over half of the social sector’s funding. For historical reasons there is often a close and dependent relationship between the social sector and government. Philanthropy has traditionally been quite weak in these countries, constituting less than 0.3 percent of GDP.

Social democrat model (Sweden and other Nordic countries) | The social sector is small, accounting for less than 3 percent of total employment, and rooted in voluntarism, relying primarily on membership fees and charges for its funding rather than government money. The nature of the social sector derives from the fact that state-sponsored and -delivered social welfare programs are quite extensive, leaving little room for nonprofit organizations to provide services. The social sector is based primarily on an associational culture, with nonprofits functioning mostly as vehicles for people’s political, social, and recreational interests. The social sector is significantly independent of government control, but is limited in size and influence by a relatively small philanthropic base.

Developmental model (Czech Republic, Poland, Slovakia, and Hungary) | The social sector is small, accounting for between close to 0 and 2 percent of total employment, and relies much more than in other countries on private philanthropy for its funding. Although welfare spending is relatively high (a legacy in former Communist states), the government has not developed a close relationship with civil society and has tended to manage service delivery itself rather than partnering with the social sector. Nonprofit organizations have struggled to find an independent voice after years of suppression, although this situation is changing. Philanthropy is important in nurturing and financing the growth of nonprofits, although there is no strong philanthropic tradition.

In the United Kingdom, where the liberal model of philanthropy prevails, venture philanthropy and social investment have matured more rapidly than in the rest of Europe. That should be no surprise. The United Kingdom is perfect terrain, with a strong tradition of venture capital and entrepreneurship as well as a developed philanthropic sector. Indeed, in the United Kingdom, there is now a fairly rich ecosystem of venture philanthropy organizations. These include social investment players such as Bridges Ventures, Big Issue Invest, and Venturesome, and venture philanthropy players such the CAN Breakthrough, Impetus-Private Equity Foundation, and CIFF. The social enterprise sector is also growing significantly, providing a rich set of organizations to invest in. And there are large-scale government initiatives to boost and fund venture philanthropy (such as Big Society Capital). During the new era of public sector austerity this trend is likely to continue, because the government is keen to promote and experiment with less expensive ways to provide social services. One of these innovations is the pay-for-results model of social impact bonds. Given these conditions, it is likely that venture philanthropy and social investment will continue to grow in the United Kingdom.

In countries where the welfare partnership model of philanthropy dominates, such as France, Spain, and Germany, the social enterprise and venture philanthropy movements are still fairly young and just starting to gather momentum. The field is dotted with a few strong demonstration projects by private individuals and corporations with a growing but still small-scale interest in social enterprise and venture philanthropy. In Spain, for example, three years ago there were no venture philanthropy funds for social entrepreneurs. Today, local councils are running social entrepreneurship programs, large corporations such as La Caixa, BBVA, and Caixa Catalunya have set up grant and social investment programs, elite business schools such as ESADE and IESE have established social enterprise programs, and some private social impact investment funds have been set up. Despite these positive trends, strong barriers to growth remain, including the conservatism of foundations and the lack of human capital to launch and operate these hybrid initiatives. In all of these countries the field of venture philanthropy is still in a definitional phase. There are strong debates about what a social enterprise or social investment is, in particular whether the definition includes the large, historic cooperative sector, which some do not consider sufficiently “social” apart from its structure. In France, the nonprofit organization Finansol is seeking to create a more strict definition and labeling regime about what is a social investment (“finance solidaire”) to help retail investors place their funds more accurately.

Important factors affecting the nature and the growth of venture philanthropy and social investment in the partnership model countries are government initiatives and the particularities of the philanthropic landscape. In France, for example, the social investment sector received a significant catalyst in 2008 when a new law was passed requiring all corporate defined-contribution savings and retirement plans to establish a solidarity fund, to be invested in what the French government describes as a solidarity business. In Spain, which suffers extraordinary levels of unemployment, the social enterprise sector is heavily oriented toward initiatives that increase employment. The folding or privatization of the caja de ahorros (savings banks that traditionally have contributed a large share of social sector funding in Spain) is likely to wreak havoc while creating the need for more financially sustainable alternatives that venture philanthropy can help provide.

In countries where the social-democrat model of philanthropy is prevalent, such as Sweden and Norway, the entrepreneurial culture creates a potential fit for venture philanthropy. But because of the strength of the welfare state, philanthropy has not played a significant role in civil society, and so venture philanthropy has struggled to make an impact. That may change. Some recent high-profile initiatives, such as the setting up of the Ferd Social Entrepreneurship Fund by Johan H. Andresen Jr., the wealthiest man in Norway, have started to put social enterprise and venture philanthropy on the map.

In countries characterized by the developmental model of philanthropy, such as those in Eastern Europe, venture philanthropy has struggled to grow despite the valiant efforts of organizations such as NESsT. These countries, many of which suffered under decades of totalitarian rule, have had a small philanthropic sector. They also suffer from short-term thinking and a general lack of risk-taking, affecting both business and philanthropy. Meanwhile the government is becoming increasingly dominant in the social sector, with a risk that it will squeeze out private initiatives.

Evolution of European Venture Philanthropy

Venture philanthropy began in the United States in the 1990s and traveled across the Atlantic Ocean to Europe, where it took root in the early 2000s. The first phase was between 2000 and 2004, when business entrepreneurs and professionals from the private equity and venture capital world set up the first venture philanthropy funds. As with venture philanthropy in the United States, it was primarily a new type of donor (and new money) that was attracted to the concept. Business leaders, particularly those from the finance sector, were attracted because venture philanthropy combined the use of money and skills, and because the language was familiar. Many of them had the same professional background, which made for a close-knit and secure network within which venture philanthropy could start growing.

Because European venture philanthropy started in the finance sector (rather than in the technology sector as it did in the United States), it took on some unusual characteristics. One of these was the creation of innovative venture philanthropy organizations that were part social investment fund and part grantmaking institution. An example of such a fund is BonVenture, set up in 2002 in Germany by Erwin Stahl from the finance sector and funded by a few wealthy German families. BonVenture has a unique legal structure, combining a foundation that provides grants with a fund that provides loans and makes equity investments.

During the second phase, between 2004 and 2008, venture philanthropy began attracting the attention of existing European charitable foundations. Unlike in the United States, where venture philanthropy had set itself up in opposition to traditional philanthropy, European venture philanthropy was more inclusive from the beginning. In addition, the arrival of venture philanthropy coincided with a period when existing foundations were looking for new ways to better assist the social sector and align their investments with their social mission.

In the third phase, between 2008 and 2012, European venture philanthropists developed hybrid practices that were a bricolage of existing practices in the finance industry and the nonprofit sector. For example, many tried to “make money work harder” by re-investing any financial return in new investee organizations, rather than returning the money to investors. The hybridization of the business and social sectors may be one of venture philanthropy’s most powerful legacies and an extremely important step in moving philanthropy into an age where sector boundaries are blurring. The third phase was also a time when the government and large corporations began to experiment with venture philanthropy practices, adding two important sectors to the mix of actors.

Present State of European Venture Philanthropy

Perhaps the most outstanding trait of European venture philanthropy is its vibrant diversity and its presence in so many different countries. The danger with such a multiplicity of approaches, of course, is that it could lead to fragmented initiatives with little collective impact. But the advantages of diversity outweigh the risks, as diversity is more likely to drive innovation.

A good example of this diversity is NESsT, one of the pioneers of venture philanthropy in Eastern Europe. NESsT was established in 1997 as an international nonprofit organization that develops sustainable social enterprises to solve critical social problems in emerging market economies. In fifteen years, it has trained more than 3,900 social enterprises and entrepreneurs, developed more than 120 social enterprises, invested more than $8 million, and wound down 24 of its investments. It operates in Central and Eastern Europe and Latin America. Because it operates in emerging markets, its approach is quite different from venture philanthropy organizations in more mature countries, like the UK’s Impetus. NESsT has to focus on earlier stage organizations, often having to set up social enterprises to solve specific social problems rather than, as Impetus does, helping existing social enterprises scale up.

Another strength of European venture philanthropy is that because of the strong role that private equity and venture capital had in building the field, many of the organizations are financially sophisticated. It is becoming common practice for foundations using the venture philanthropy model to use financing instruments other than grants to support organizations. The 2012 EVPA survey4 found a significant increase in the use of equity and debt compared to the previous year; even for foundations and other nonprofits, the financing instrument most commonly used was debt, with grants and equity in second place. Although societal impact is the primary focus of venture philanthropy organizations, the relevance of some financial payback (either in capital or as an actual surplus on the investment) is becoming significantly more important. It is also important to note that European venture philanthropy organizations are increasingly focusing on social enterprise as a venture philanthropy investee (receiving 39 percent of funding), with relatively less funding going to nonprofit organizations.

European venture philanthropy has managed to combine financial sophistication with openness to social sector expertise and willingness to integrate the valuable experience of traditional philanthropy. One traditional foundation that adopted venture philanthropy is d.o.b. foundation in the Netherlands, a foundation that was set up in 1997 by the family of an entrepreneur who owned a chain of drugstores. Until 2005, d.o.b. was a traditional endowed foundation. It distributed a percentage of its endowment to a large number (about 120) of projects in 26 countries, with little control over and interaction with its grantees. In 2005, the foundation transformed from a project-based grantmaker to a venture philanthropy organization. It adjusted to a much smaller portfolio of 12 to 15 social purpose organizations supported through grants, loans, and equity combined with management support. The transformation involved a complete makeover of the foundation, including new staff, a much narrower focus, and a willingness to co-invest with other venture philanthropy organizations to share transaction costs and non-financial support.

European venture philanthropy has also exerted an influence on public policy at a national and Europe-wide level. This is partly because those involved in European venture philanthropy are often influential people within their fields and have access to the political process. It is also because of the efforts of the EVPA to organize and aggregate field-level efforts. For example, members of the association played an important role in the adoption of the EU Social Business Initiative and are assisting in the creation of a regulatory framework for marketing social entrepreneurship funds.

One important weakness of European venture philanthropy is that it still cannot clearly articulate its social impact. Without objective data, no one really knows beyond anecdotal case studies whether European venture philanthropy is creating real, incremental value in the communities it is serving. It is, however, encouraging that more organizations are focusing on measuring social impact. In EVPA’s 2012 survey, 90 percent of respondents reported that they were measuring social impact at least annually. But in many cases they are measuring only outputs (the number of poor people enrolled in a job training program, for instance) rather than the more important outcomes (the number of poor people who were in a job training program who got a job and were still working one year later). EVPA’s impact measurement initiative, launched in 2012, is providing practical recommendations on how to measure and manage social impact.

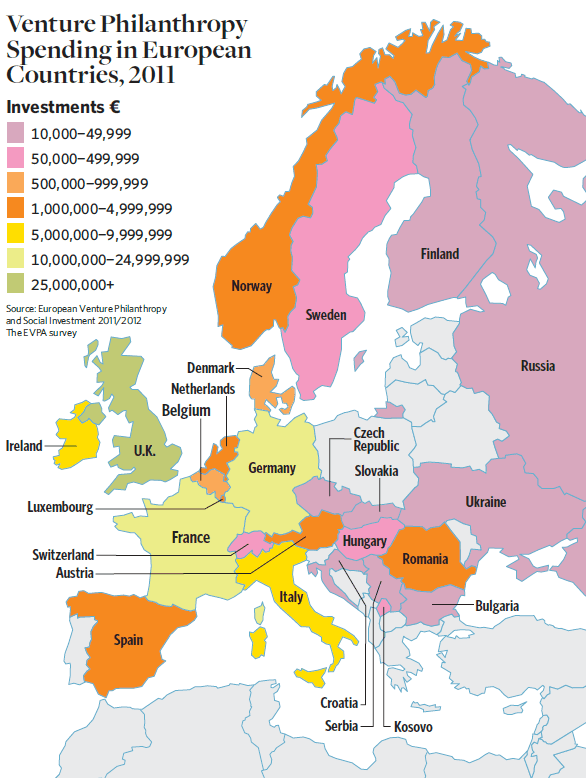

One of the reasons for the lack of attention to measurement is that European venture philanthropy organizations themselves are under-capitalized. Yet without clear evidence of social impact that would attract more money to the field, venture philanthropy may be destined to remain under-capitalized. The reality is that many European venture philanthropy organizations are engaged in a struggle for fundraising survival. The majority of organizations (61 percent) allocated less than €2.5 million to venture philanthropy and impact investing (as a total budget including investments and overhead expenses) in the last fiscal year; the average amount allocated was €7.4 million and the median was €1.3 million. Only a small percentage (8 percent) had a budget greater than €20 million. (See “Venture Philanthropy Spending in European Countries, 2011” below.)

As for the source of money, most European venture philanthropy organizations surveyed are not endowed. Financial institutions, individual donors, and investors represented the main sources of funding, composing roughly 19, 17, and 16 percent of total funding respectively. Government accounted for 15 percent of funding, corporations for 14 percent, and endowment income for 11 percent. External foundations represented 6 percent of funding, and institutional investors just 1 percent. The result is that a significant proportion of venture philanthropy organizations offer small amounts of money that arguably do not provide enough investment to create a transformational change.

The Future of European Venture Philanthropy

The big challenge that European venture philanthropy organizations face is how to increase the amount of capital being invested in venture philanthropy. The European venture philanthropy industry is still in its infancy, with many small organizations struggling to survive. For venture philanthropy to have an impact, the size of individual grants, loans, or equity may need to be in the millions of euros to give the grantee the breathing space it needs to stop the merry-go-round of fundraising or to invest appropriately in its social business. There may not be a huge number of social-purpose organizations that could absorb this type of funding, but if the stated objective of venture philanthropy is transformational and system-wide impact, then the amount of funds donated is critical.

In this context, the global recession is both an opportunity and a threat. On one hand, it is creating a demand for innovative solutions that favors venture philanthropy. While the economic and social crisis is deepening social problems, governments on austerity drives are slashing their spending. European venture philanthropy could help social-purpose organizations become robust enough to survive and even thrive in this difficult funding climate. The threat is that the recession will make raising funds for existing non-endowed venture philanthropy organizations even harder and halt the growth of new funds. We did see a record number of new funds established in 2011, however, suggesting a reinvigoration of venture philanthropy in Europe. The organizations that were founded in 2011 were also from diverse regions of Europe: Benelux, Eastern Europe, France, Italy, Scandinavia, Switzerland, and Austria, showing the strength of venture philanthropy activities across Europe.

Moreover, there was a 27 percent increase in the average annual financial expenditure of venture philanthropy organizations, from €4.1 million in 2010 to €5.2 million in 2011. The total expenditure of European venture philanthropy organizations in 2011 was €278 million for the 54 respondents that answered this question in the EVPA survey, an increase of 47 percent compared to €189 million in 2010 for 44 respondents. With limited, albeit growing, amounts of capital, venture philanthropists can leverage their resources by spreading their practices further afield to other types of organizations where larger-scale investments will help venture philanthropy increase its impact. This approach builds on venture philanthropy’s strength: It is a hybrid practice with strong potential for cross-sector collaboration. Promisingly, we are already witnessing some of the effects of venture philanthropy’s role as a catalyst in five areas.

First, traditional foundations are adding venture philanthropy as another tool in their toolkit. In the United Kingdom, where European venture philanthropy started, venture philanthropy has gone mainstream among foundations. Although many foundations do not use the term venture philanthropy, they increasingly support nonprofit organizations and social enterprises over multiple years, provide grants or other types of financing to support capacity building, and offer non-financial support.

Second, as corporate social responsibility becomes embedded in European business culture, the amount of funds invested by corporations in social-sector organizations is increasing. Venture philanthropy is already influencing the rapidly growing ranks of corporate philanthropy in leading corporate foundations such as BMW, Vodafone, and Shell. New entrants into the venture philanthropy market include Inspiring Scotland, a venture philanthropy fund co-invested by Lloyds TSB Foundation and the Scottish government that invests £10 million a year, as well as Fondazione CRT, one of the products of the Italian savings bank privatization in 1991 that has recently set up a venture philanthropy fund.

Third, European venture philanthropy is catalyzing collaborations between the government, philanthropic, and social sectors. One example is CIFF, a fund that works with governments to ensure the sustainability of its large-scale initiatives after it is gone and actively influences government policy. Another example is the social impact bond, a financial instrument pioneered in the United Kingdom that is used to fund programs that save the government money. The investors of the first social impact bond in Peterborough prison included 17 individuals and foundations, not surprisingly including EVPA members such as Esmée Fairbairn Foundation that have previously invested in venture philanthropy funds. One of the investees in the Peterborough bond, St Giles Trust, was previously funded by venture philanthropy pioneer Impetus Trust.

Fourth, the burgeoning number of social enterprises in Europe presents a growing opportunity for venture philanthropy investment. European governments are increasingly recognizing the potential of social enterprise and social investment and are starting to provide much-needed capital for intermediaries. The UK’s Big Society Capital, for example, will be capitalized with up to £600 million from dormant accounts and high-street banks to develop “socially orientated investment organizations.” The European Investment Fund is about to launch a fund of funds to invest in “social entrepreneurship funds.” And the European Single Market Act, adopted in April 2011, includes the launch of the Social Business Initiative that notably makes access to funding for social businesses a priority.

Fifth, the booming interest in impact investing provides an opportunity for venture philanthropy organizations to share their experience in supporting and financing early-stage social enterprises. It also presents an opportunity for venture philanthropists and impact investors to collaborate. Venture philanthropy can provide the missing middle between pure philanthropy on one hand and equity investments by impact investors on the other. Some European venture philanthropy funds, such as Noaber Foundation in the Netherlands, have both a grant-making foundation and an impact investment fund, and therefore are perfectly positioned to support a new organization through its development lifecycle.

Venture philanthropy is a growing force in Europe. The number of funds and organizations devoted to this approach is increasing, as is the amount of money invested. As important as those efforts are, venture philanthropy can have an even greater impact on society by focusing on the dissemination of its practices to impact investors, governments, traditional foundations, multilateral organizations, and other influential actors. This approach has already produced results, as demonstrated by the UK government launching Big Society Capital, BBVA bank promoting a venture philanthropy fund, and the City of Malmö setting up an area-based social investment fund. These examples, and more, are telling illustrations of venture philanthropy’s potential for enormous societal benefits throughout Europe.

Read more stories by Lisa Hehenberger, Leonora Buckland & Michael Hay.