(Illustration by David Herbick)

(Illustration by David Herbick)

Over the past century, new technologies, innovation in delivery models, and increased government support have drastically transformed the health of human populations. Most people living in the developed world now live longer and healthier lives than ever before. Yet for the 1.29 billion people living on less than $1.25 per day, quality health care remains out of reach. The World Health Organization estimates that every year more than 7.6 million children under the age of 5 die and more than 1.7 billion people lack access to essential medicines. This large and growing divide in access to high-quality health care between the wealthy and the poor seriously threatens global safety, security, and economic development. Increasingly, scholars, policymakers, investors, and entrepreneurs face a glaring challenge: to provide access to affordable high-quality health care, especially to essential medicines and vaccines, or see the divide between the wealthy and the poor grow.

Health care delivery depends on the synchronous provision of multiple inputs: motivated health care professionals; functioning equipment; well-organized information and financial flows; and adequate supply of medicines, vaccines, and other products. Improving the effectiveness, quality, and efficiency of health care delivery requires understanding the connections and complements among these inputs.

Against significant odds, health care delivery in developing countries is harnessing these inputs, becoming a hotbed of social innovation. And a large number of new business model innovations in health care are coming not from the richer developed countries but from the poorer developing countries. Three factors explain this trend. First, the pressing need to improve affordability has created stronger incentives for business model and process innovation in developing country health care markets. Second, the lack of a legacy health care payment system and the absence of strong entry barriers have led to fewer constraints for health care delivery innovation in developing countries. And third, innovations are resulting from cultural necessities.

In Afghanistan, for example, social and cultural norms have inhibited women from acting as community health workers. Meanwhile, male community health workers exist, but mostly fail to improve maternal and child health because women are the primary caregivers in Afghan society. The Women’s Courtyard was launched by UNICEF and the Department of Public Health Nangarhar in 2008 to tackle this problem. The program’s aim is to give Afghan women an understanding of polio as well as other vaccine-preventable diseases and related issues, such as hygiene and waterborne illnesses. In areas where the vaccination coverage rate is insufficient, 10 to 12 women community health workers create a “women’s courtyard,” and it is their responsibility to visit each household in their area and to explain to the mothers, sisters, or grandmothers of young children the need for vaccinations.

Many of today’s innovative health care delivery models are built around ways to deliver high-quality care at significantly lower cost by leveraging high patient numbers and process standardization. One of the most often cited examples is the Aravind Eye Hospitals in India, which provide cataract operations to large numbers of poor people at low prices through meticulous standardization of diagnosis, surgery, recovery, and discharge processes. Aravind’s high-volume, high-throughput model results in very high efficiency that keeps costs low without compromising quality. Similarly, Narayana Hrudayalaya Hospitals, a complex of health centers in southern India, is able to provide high-quality cardiovascular interventions at very low prices by using a meticulously standardized, high-volume model. LifeSpring Hospitals, also in India, provides maternity and infant delivery services at less than half of market prices, once again through the use of process standardization and high volumes.

Some innovators are leveraging low-cost franchise models by providing health care at patients’ homes—the lowest tier in the health care provision system. For example, VisionSpring provides affordable eye care to the poor by training its micro-entrepreneurs to diagnose vision problems and provide mass-produced eyeglasses in rural villages. Another example of innovative, developing-world health care involves tuberculosis treatment. Operation ASHA, a TB treatment nonprofit that administers antibiotics to 5.37 million people, uses a field delivery model, where health workers go to the homes of patients in 2,053 villages and slums in six states across India and Cambodia. The cost of treating a TB patient using Operation ASHA’s innovative but frugal model is $50, much lower than the cost of other models.

Other innovators use technology to change the structure of the health care delivery process. In Mexico, Medicall Home provides telephone-based medical consultations and triage for a monthly fee of $5, charged to patients’ phone bills. A similar service called MeraDoctor.co exists in India. World Health Partners (WHP) in India also uses telemedicine technology, and it has carefully designed a system of financial incentives to connect and organize health care providers into a tiered network.1 In a few years since the launch of its network in the Indian state of Uttar Pradesh, WHP has provided five to 10 times more family planning services than government and NGO networks through more than 800 providers, 76 telemedicine centers, and 1,400 pharmacies.

Although an important transition has begun in the structure of health care service delivery in many developing country markets, the product supply chain for medicines and vaccines is moving at a slower pace. Given the high interdependence of inputs needed in health care, innovation that is restricted to only one area will not generate large-scale improvements. Lack of financing and product awareness can be among the reasons people can’t or don’t access medicines and vaccines. But a larger problem is that in many low- and middle-income countries, the distribution network for medicines is generally ineffective and inefficient, resulting in low availability of medicines to the poorer sections of populations. This problem is especially pronounced in sub-Saharan Africa, where health care infrastructure is poor and the prevalence of communicable diseases is high. Also notable is that government-run systems are largely responsible for providing medicines and vaccines in many poor countries and regions.

There is a great need for process and business model innovation that can enable wide-scale distribution of high-quality medicines and vaccines at affordable prices. How can this happen? And why is the pace of change so slow? In some cases, large government-run supply chains hinder innovation in developing countries. Government monopoly over the medicine supply chain de-incentivizes innovative models that test new approaches at smaller scale. One might look to process and business model innovations, which have improved access and affordability for consumer products like mobile phones and top-up cards. But medicines are not cell phones or top-up cards; they require specialized preservation and administration. Moreover, medicines are both expensive and inaccessible to many because of a complex combination of institutions specializing in manufacturing, import, wholesaling, retailing, and various other auxiliary functions that need to join forces to make a drug available.2

If there is one product that exemplifies a successful supply chain in the developing world, it is Coca-Cola. Coke is sold in stores, restaurants, and vending machines in more than 200 countries. Over the past century, the company had created a tailored distribution system that surmounts vast differences in road infrastructure, retail market and cost structures, and customer needs in emerging markets. Indeed, when health care experts get together to bemoan the difficulty of distributing essential medicines in the developing world, Coca-Cola comes up. People ask: Why can’t medicines and vaccines be distributed through the same channels as Coca-Cola? Why can’t there be more tailored distribution models like Coca-Cola Micro Distribution Centers.

Yet these questions do not address the similarities and differences between soft drink and medical supply chains. This article compares the two supply chains in developing countries to highlight what can be learned from Coca-Cola’s distribution, what can be borrowed, and what is impossible to replicate. It also describes several new enterprises that have begun to mimic the effectiveness and efficiency of soft drink supply chains, while preserving the safety and traceability that are vital to medicine supply chains.

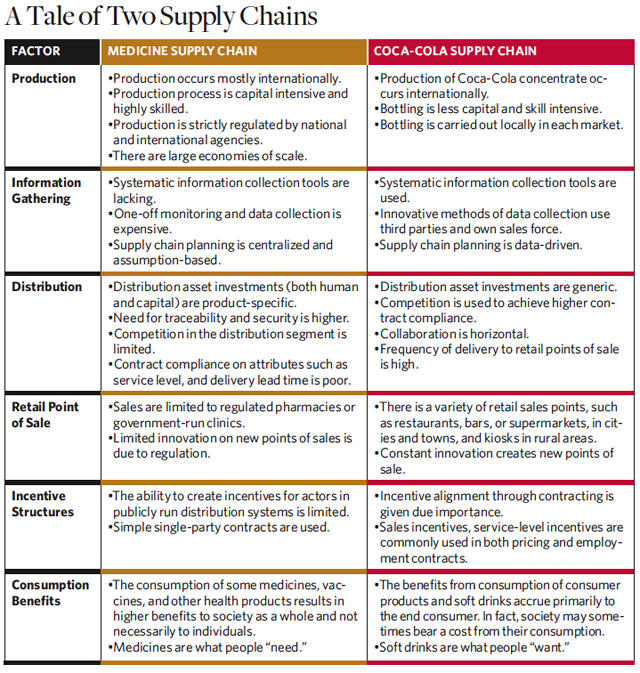

Production: Capital and Regulation Impediments

Coca-Cola started building its global network in the 1920s and since has used its franchised strategy to localize parts of the production of its soft drinks and to build distribution and sales infrastructure through partnerships with domestic companies in developing countries. Starting in the early 1900s, Coca-Cola built bottling operations in Cuba, Panama, Canada, Puerto Rico, the Philippines, France, and Guam, many of which were joint ventures or franchised bottling operations. To maintain control over the soft drink’s ingredients and to protect the intellectual property of its brand, Coca-Cola manufactures its concentrate only at select locations, including some wholly foreign-owned sites in the developing world. If there is no local concentrate production site in a specific country, the concentrate is imported and bottled by one or more bottling franchises that also carry out the in-country distribution. For example, to serve the geographically vast market in China, Coke works with three bottling companies that run 38 in-country bottling plants. Both the concentrate-manufacturing process and the bottling plant require relatively small capital investments.

Under this model, Coca-Cola manufactures concentrate in a few locations and sells it to bottling operations, which then carry out the functions of manufacturing, packaging, and distributing the finished branded beverages to retail locations, allowing Coca-Cola to achieve global reach and scale through the local knowledge and distribution strength of the local partner.

In contrast, most large pharmaceutical companies limit their manufacturing to one or two production facilities. This choice is due in part to the lower costs of international transport for medicines and vaccines relative to the higher costs of establishing a plant.3 Pharmaceutical companies also must comply with production regulations, as the manufacturing of medicines and vaccines is subject to international quality standards, to avoid counterfeits and other problems. In addition, compared to producing soft drinks, pharmaceutical production requires higher technical skills. The educational and vocational systems in many low-income countries are not yet supplying the engineers, pharmaceutical specialists, and other skilled workers crucial to running a high-quality pharmaceutical production plant.

Information: Gaps in Market Knowledge

Another central problem for medical supply chains in the developing world is the lack of systematic information collection regarding demand and supply. Obtaining an accurate estimate of the size of a market for specific medicines is extremely challenging, because of the lack of knowledge of the size, income levels, or location of various populations.4 In addition, because of the lack of well-established government infrastructures, public health information is often unreliable or inconsistent. Expensive one-off monitoring and evaluation reports are usually used. Such ad hoc and low frequency reporting is expensive and does not adequately capture trends and the dynamic nature of market demand.

Soft drink companies, in contrast, have realized the value of consumer market information and are willing to invest in information gathering, even if it requires time-consuming manual methods. In the case of Coca-Cola, employees of the bottling company work to coordinate deliveries and visit retailers on a regular basis to take orders. As they visit customers, they send in new orders electronically or by phone, keeping the cycle of sales, production, and delivery moving forward. Using the information they collect on each visit, they compile periodic consumption and stock status reports to ensure better logistical and financial planning. In some cases, third-party information aggregators invest in information gathering on behalf of multiple consumer product companies. This reduces the individual costs for each soft drink company to obtain information that is vital for planning.

Rather than investing in point-of-sale information gathering and demographic data, medicine supply chains are based on central planning assumptions. Supply chain planners for medicines tend to attribute the lack of planning data to the absence of formal information systems. Instead of using the existing mechanisms for collecting information or incentivizing third parties to do it on their behalf, they rely on expensive one-off monitoring and evaluation exercises.

But exceptions to this approach are emerging. The ACTwatch project is a multiyear, multi-country study funded by the Bill & Melinda Gates Foundation to use a third party to gather market data for antimalarial medicines. ACTwatch researchers have captured key trends in the retail availability, volumes, distribution channels, and use preferences for antimalarials in eight countries. Another example of innovation in information gathering is the SMS for Life project, a publicprivate partnership founded in 2009 that harnesses simple mobile phone technology to eliminate stock-outs and to improve access to essential medicines in sub-Saharan Africa. SMS for Life has scaled up in Tanzania, where better information on stock availability is contributing to reduced stock-outs of medicines in public health clinics.

Distribution: Traceability, Market, and Labor Impediments

Medicine distribution requires traceability to ensure security in the supply chain. In some cases, distribution is limited to state-run systems, such as central medical stores, which hinders the creation of incentive structures. Even when medicine distribution occurs through a private network in the developing world, the regulatory framework and small size of the market prevent adequate competition. This lack of competition and the absence of efficient legal systems make contract compliance and contract enforcement problematic. A well-functioning distribution network also requires investment in a specialized labor force. It requires quality control experts, pharmacists, doctors, and distribution and supply chain specialists, yet this level of professional specificity in poor countries is in short supply.

Nonetheless, small-scale innovation to improve traceability is emerging, even while the World Customs Organization reports that the fake drug market is estimated to be a $200 billion a year industry. Sproxil, for example, a for-profit social enterprise founded by a Ghanian based in Cambridge, Mass., has developed simple product authentication technology to minimize the presence of counterfeits in emerging markets. The company places a scratch-off label on products; after purchasing an item, consumers scratch off the label, revealing a unique, random code, which they send via SMS to a country-specific short code set up by Sproxil. The consumer then receives a text about whether the product is genuine. In 2010, NAFDAC, the Nigerian government agency overseeing food and drugs, endorsed the Sproxil platform, and the service has been widely deployed throughout Nigeria. In June 2011, Sproxil launched operations in India, and in July 2011 Kenya’s Pharmacy & Poisons Board adopted similar text message-based anticounterfeiting systems. As of early 2012, more than 1 million people in Africa checked their medicines using Sproxil’s text message-based verification service.

As for the market distribution similarities (or dissimilarities) of Coke vs. medicine, the franchised bottler model allows Coca- Cola to leverage local partner knowledge and understanding of domestic distribution channels. If the domestic partner does not fulfill its contracted obligations on quality, pricing, reach, brand promotion, or other attributes essential for better market reach, Coca-Cola can threaten to offer more local bottling contracts, to bring in more competition. This helps to ensure higher compliance with contract terms by the incumbent local partner.

In medicine supply chains, the partner is often the national government. Thus the medicine manufacturer has little if any ability to enforce its objectives. State-run distribution systems work with an incentive structure that is very different from that of the manufacturer. Government-run distribution systems are managed by civil servants who do not always have the accountability and incentive systems built around increased availability of medicines in clinics. Even when one works with a private import agent, structural and regulatory difficulties impede creative methods to ensure contract compliance.

In contrast, Coca-Cola uses a broad array of distribution channels to achieve expanded reach. Coca-Cola is mostly sold by bottlers through independent wholesale distributors, although direct retail sales are now gaining ground in some areas. Some of these wholesalers have been distributing products in their countries for many decades, and they have significant political clout in the regions where they operate. Trucks are the primary means of national distribution, with wholesalers often using bicycles at the local level. In markets where a conventional truck delivery model is not effective or efficient, Coca-Cola uses independently owned distributors, called the Micro Distribution Center, for delivery to small retailers.

For the medicine supply chain in developing countries, it is safer to limit the distribution of medicines to a few tightly regulated distribution channels, including transport by dedicated trucks and vans. New developments in tracking and tracing technology, however, have offered solutions that are opening up transport and distribution options. ColaLife, an independent nonprofit that grew out of a 2008 online campaign, for example, is trying to use Coca-Cola’s secondary distribution channels in developing countries to carry lifesaving “social products,” such as oral rehydration salts. Although the distribution problems can be solved using such an approach, demand generation remains a challenge.

Another example of distribution innovation is Living Goods in Uganda, which uses an Avon-like network of franchised community health agents, who provide door-to-door health education about childhood diarrhea, malnutrition, and malaria. In turn, the agents earn a living selling essential health products. Living Goods program staff meet with the community health agents at least once a month to resupply medicines, collect payments, communicate current promotions, and provide ongoing health education and business coaching. Ensuring sustainability and selecting the best product assortment are essential areas to be addressed in such distribution models.

Finally, for Coca-Cola, capital assets such as warehouses, storage depots, and the trucks and vans for effective distribution are often generic and widely available. In many markets, Coca-Cola outsources its warehousing and transportation operations to third-party companies. Creating pooled distribution helps Coca-Cola increase the frequency of shipments to the retail points of sale without increasing cost.

In the case of medicine supply chains, the human and physical assets required for effective distribution are highly specific. They require investment in staff training and specialized equipment, such as refrigerators. And because revenue earned from affordable medicines is low, there is little capital to invest in human or physical assets for pharmaceutical distribution. Moreover, the inability to pool distribution of drugs and medicines with other products results in a lower frequency of delivery to retailers.

But alternative models are being developed. For instance, VillageReach, a nonprofit in Mozambique that partners with governments, businesses, and other nonprofits, is bundling vaccines with other products to reach the country’s most isolated communities. The model is currently being implemented in 251 health centers serving more than 5.2 million people. In the region where it was implemented as a pilot, this approach has contributed to an increase in DPT-Hep B3 coverage rates from 68 percent to 95 percent, and a decrease of vaccine stock-outs from a high of 80 percent to routinely below 1 percent.

Retail Points of Sale: Limitations in Service and Delivery

Coca-Cola reaches a variety of sales outlets, such as restaurants, bars, and supermarkets in cities, towns, and small retail kiosks in rural areas. Growth in sales and market share comes from tapping into new points of sale and creating value propositions that bundle service and product delivery. The ability to create new bundles of products and services comes from the relatively low risk of poor quality in service. Coca-Cola also works to create new retail opportunities and spends time trying to understand the revenue and profit mix of each of its retailers.

In contrast, medicines are limited to certain dispensing points. These points must be able to ensure adequate equipment for storage and have staff capable of providing accurate dispensing advice. For example, only pharmacists are allowed to carry out certain activities related to dispensing medicines, and there are few trained pharmacists in most developing countries. Similarly, warehouses and distribution centers for pharmaceuticals are dedicated to medicine and cannot be shared with other commodities. There is very little evidence of effective bundling of service and product delivery in medicines, except for pharmacists dispensing advice. Some social marketing organizations, particularly those concerned with reproductive health, have been very successful in expanding reach. These organizations possess sufficient understanding of the business drivers at each point of sale, and they use points of sale similar to those of consumer product companies. But given the small size of developing country markets, pharmaceutical companies have little incentive to improve retailers’ understanding of issues such as what drives profitability and what product categories bring more customers into the store.

This situation is changing, however. The government of Tanzania in partnership with Management Sciences for Health has started a successful Accredited Drug Dispensing Outlet program to increase the retail points for dispensing essential drugs while ensuring high quality. Similar initiatives are under way in Zambia and Ghana. The Affordable Medicines Facility for Malaria is financing a pilot project of the Global Fund to Fight AIDS, Tuberculosis, and Malaria, designed to expand access to the most effective treatment for malaria and artemisinin-based combination therapies (ACTs) in retail outlets. To achieve this goal, the Global Fund has negotiated with drug manufacturers to reduce the price of ACTs, and to require that sales prices must be the same for both public and private sector first-line buyers.

Incentive Structures and Risk-Reward Sharing

In soft drink supply chains, a host of stakeholders are involved in making decisions about price, inventory, promotion, and other factors. Individual decision makers are rewarded for optimizing local objectives and coming up with solutions that mitigate risk. This could involve understocking a brand of drink. The manufacturer has a high incentive to ensure that the retailer keeps sufficient quantity of the product in stock. One approach for inducing the retailer to increase stock levels is to increase the profit margin on sales. But this leads to increased end customer price, which may lead to lower demand. In many instances, the wholesaler offers a different wholesale price to the retailer on sales above a specified level. This has the effect of increasing the retailer’s cost of having too little inventory.

In a similar vein, soft drink companies offer financial incentives to wholesale distributors to improve reach and sales in each outlet. Such contracts are the cornerstone of incentive management in soft drink distribution channels.

Coca-Cola has a comprehensive incentive framework for its internal staff, bottlers, retailers, and wholesalers. Internal employees are awarded points by their superiors and co-workers for achieving goals. These can be redeemed for merchandise, travel, and cash. To its retail partners, Coca-Cola often provides refrigerators at a 50 percent discount or offers a few dozen crates of free product for accomplishing a preset sales target. Monetary trade incentives are provided to wholesale distributors to increase the number of retail outlets and the amount of sales in each outlet.

Medicine manufacturers, on the other hand, have limited ability to create incentives for actors in the supply chain. The financial incentives used by Coca-Cola to increase sales—and, hence, availability—are also not as applicable in the case of medicines, as they could lead to abusive drug use as well as drug resistance and other related problems resulting from incorrect use of medicines.

A Promising Future Trajectory

As the examples above show, innovations in service delivery together with new models in medicine distribution can truly improve health care for the bottom billion. Innovations that help create a local manufacturing system for some parts of the medicine production process, the equivalent to bottling in the case of Coca-Cola, would help medicine supply chains better emulate Coca-Cola’s model for global scale and reach. Although some innovative models for this already exist, new ways of providing incentives to different actors in the medicine supply chain and collecting demand and supply information at different levels of the supply chain are needed.

Although it is useful to compare the supply chains for medicines and Coca-Cola, the consumption benefits of medicines vs. Coca-Cola are widely divergent—and thus the applicability of a truly market-driven supply chain for medicines is less clear than for consumer products. After all, the consumption of Coca-Cola benefits only the individual consumer (in his desire for a cool, sweet drink). In contrast, when individuals are treated for an infectious disease, the rate of transmission to society as a whole is reduced. The health care sector must make extra effort to convince people to take preventive and curative medicines and to come up with a way for society to pay for them. Yet if increased demand, subsidies, or other interventions can resolve some of this market imperfection, the difference in the nature of consumption benefits between medicines and Coca-Cola becomes less significant. By working together, social innovators, governments, and investors can make the goal of essential medicines and basic health care for the world’s poor feasible in a much shorter span of time.

Read more stories by Prashant Yadav, Orla Stapleton & Luk Van Wassenhove.