Illustration by Angie Wang

Illustration by Angie Wang

The growing threat of climate change is no longer a matter of contentious scientific debate. Climate scientists now agree that humanity’s “carbon budget”—the cumulative sum of greenhouse gases that humanity can emit while avoiding the worst effects of climate change—will be exhausted by roughly 2040 at current emission rates. While all levels of warming carry consequences, exceeding this budget will likely cause more than 2 degrees Celsius of warming, triggering irreversible, dangerous, and costly climatic change.

For decades, investors, policy makers, academics, and entrepreneurs have been debating the best path forward. In recent years, the costs of clean and efficient technologies such as solar photovoltaics (PV), LEDs, and electric vehicles have plummeted, and deployment of these technologies has skyrocketed.

While we all applaud these achievements, they have also led high-profile investment professionals such as Jigar Shah, academics such as Marc Jacobson, and other vocal figures to proclaim that the world already has the portfolio of solutions necessary to solve the climate crisis, and that investors and governments should focus their efforts on supporting the deployment of these later-stage solutions. This assertion calls into question the value of funding early-stage solutions and places the funding of early-stage and later-stage solutions in competition with one another.

On the contrary, we argue that investments in early- and late-stage solutions are complementary. The most effective portfolio to achieve climate change mitigation will require thoughtful investments in climate solutions along the entire “innovation continuum,” from conceptual ideas to solutions that are ready for commercial deployment and widespread impact. Drawing a distinction between so-called innovation and deployment presents a false dichotomy; innovation takes place as solutions are ideated, developed, and deployed.

An investment approach that supports and links solutions at the earliest stages of development to more mature solutions will improve the stock and the flow of solutions capable of mitigating greenhouse gas emissions. Yet this is not the investment approach we see in today’s financial marketplace. In fact, the amount of capital flowing to early-stage solutions is disturbingly low, despite the critical role that these investments play in mitigating climate change.

To correct this funding gap, new financing vehicles—especially from charitable asset owners—are needed that better align with the development of climate solutions that will secure a low-carbon future. These vehicles must harness capital that can tolerate long development timelines and accept high risk in exchange for high social and environmental impact. Philanthropists are the investors best suited to fund these vehicles.

While we focus our attention on funding for nascent solutions, we do not downplay the urgent need to perform basic research and deploy mature solutions. Indeed, the most concise summary of our approach is as follows: deploy the solutions we have, develop and improve the ones we need, and create more solutions through investments in research and development. As we will demonstrate, both research and deployment of existing solutions are key parts of an integrated innovation system. However, our assessment suggests that the capital gaps facing nascent climate solutions are particularly acute, and philanthropists, among all global asset owners, are uniquely positioned to help fill this gap.

The Process of Innovation

Scholars studying innovation have long held that innovation is the result of a complex process that spans all stages of solution development—from invention to demonstration and commercial deployment. Widespread deployment—such as that of solar PV and wind technologies today—represents the last stage of an innovation system, whose earliest stage begins with researchers achieving their proverbial “aha” moments in university laboratories. Arnulf Grubler and his co-authors at the International Institute for Applied Systems Analysis—one of the leading institutions studying innovation systems—define innovation as “putting ideas into practice through an (iterative) process of design, testing, and improvement.” 1

The innovation process is not unidirectional; all stages, from earliest to last, influence each other. In fact, developments in early- and late-stage solutions are complements: Difficulties met in deploying existing solutions create new questions and incentives for early-stage discovery, and early-stage discovery creates new opportunities for deploying existing solutions. For example, when oil and gas developers faced significant challenges extracting well-known shale resources, the challenge spurred the development of horizontal drilling and hydraulic fracturing techniques. Similarly, the iron lung was an adequately functional solution to extend the life of polio victims in the early 1900s, but its extreme toll on quality of life motivated research into alternative solutions, such as vaccines.

Conversely, the early stages of the innovation process yield insights that enable more rapid or effective deployment of existing solutions, create entirely new markets, and spark unanticipated “knock-on” effects. One such knock-on effect can be found in the application of perovskite crystals (first discovered in the 1830s) to photovoltaic applications (performed for the first time in 2009). Before this discovery, perovskites were used in a variety of applications; for example, ceramic capacitors, relying on ferroelectric perovskites, have been used widely in electronic applications ranging from computers to mobile phones. Their photovoltaic use, originally unanticipated, could lead to dramatically cheaper solar energy, driving down future greenhouse gas emissions.

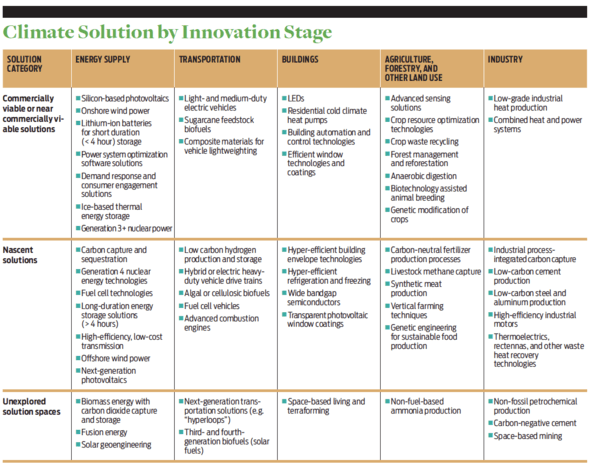

To simplify our discussion, we define three different stages of solutions: unexplored solution spaces, nascent solutions, and commercially viable or near-commercially viable solutions. The earliest stage of development is exploration, and we term solutions (or groups of solutions—i.e., solution spaces) in this stage “unexplored.”

- Unexplored solutions are ones that society might need or want but are still in the earliest stages of research and initial development.

- Nascent solutions are ones whose basic properties have been researched and proven, but ones that must be brought to commercial scale and competitiveness through further prototyping, testing, and demonstration.

- Commercially viable or near-commercially viable solutions are economically attractive to customers with minimal public support. Reaching economic competitiveness does not mean that innovation stops—these solutions will continue to develop through applied research and development, scale-up, and learning by doing.

Solving the climate challenge will require investments in solutions at each of these stages. Indeed, investments in unexplored and nascent solutions should not be viewed as competing in a zero-sum game against later-stage investments in commercially viable solutions. The world’s leading organizations on climate and energy systems echo this view. The International Energy Agency argues that staying within the 2 degrees Celsius target “does not depend on the appearance of break- through technologies,” but goes on to say that “technology innovation is essential, for example, in accelerating technology development, reducing technology costs or facilitating market access.”2 Other prominent figures have echoed this sentiment. For example, former US Secretary of Energy Ernest Moniz, in arguing that “clean energy innovation is the solution to climate change,” states that “put simply, we can’t beat climate change with only the technology we have today.”3

The Need for New Solutions

To demonstrate this thesis and bring more granularity to the current debate, we reviewed the best available literature and mapped a subset of climate solutions across the three stages of innovation and onto the Intergovernmental Panel on Climate Change (IPCC) economic sectors. The IPCC breaks the global economy into five broad greenhouse gas-emitting sectors: energy supply; transportation; buildings; agriculture, forestry, and other land use; and industrial production. This mapping is not intended to serve as an exhaustive technology-gap assessment, but rather to demonstrate how certain economic sectors do not currently have a comprehensive suite of economically competitive solutions. Building off of this mapping, we highlight examples of three fields of research that demand further investment in unexplored and nascent solutions as part of a climate change mitigation portfolio.

The case of solar PV illustrates the need for continued investment in the earliest stages of innovation even in a field where commercially or near-commercially viable solutions exist. Solar PV is widely considered to be economically viable without subsidy in many markets today. Recent research demonstrates that this competitiveness is due in large part to research and development efforts undertaken over the past 40 years.4 However, as penetration increases, the cost of solar PV systems must fall to remain competitive.5 Therefore, many solar PV experts argue that nascent solutions will need to be further developed in order for solar PV to continue to be deployed at the rate necessary to meet climate targets. Indeed, a group of solar PV researchers at MIT have found that “line-of sight technology [PV] improvements are insufficient to reach aggressive [climate] targets, which give the highest likelihood of preventing catastrophic climate change.”6

Waste-heat recovery technologies are an example of nascent technologies that also provide important climate mitigation opportunities. Nearly 60 percent of energy is wasted worldwide as heat, according to Lawrence Livermore National Laboratory. A number of nascent solutions, including thermoelectrics, thermionics, and rectennas—technologies that can capture typically wasted heat and convert it or use it directly—hold promise for dramatically increasing the efficiency of industrial processes in the near term, and of transportation and energy supply in the longer term; they also may open up new potential applications. Fortunately, many new ventures are developing solutions in these subsectors, such as Alphabet Energy in thermoelectrics, Spark Thermionics in thermionics, and RedWave Energy in rectennas. These nascent solutions will require significant and persistent financial support. The necessary capital has unfortunately proved challenging to secure in today’s financial marketplace.

Finally, carbon-negative technologies serve as an example of a relatively unexplored solution space. Many experts believe that humanity faces a risk of emitting too much greenhouse gas to stay below 2-degree warming targets, and that, as a result, greenhouse gases will need to be removed from the atmosphere through the use of carbon-negative technologies. The IPCC notes that “many [climate] models could not produce scenarios leading to about 450 ppm CO2eq [2-degree warming] by 2100 with limited technology portfolios, particularly when assumptions preclude or limit the use of BECCS [biomass energy with carbon dioxide capture and storage].” 7 However, BECCS—a carbon-negative technology—has scarcely been tested at commercial scale. And, as highlighted by the $4 billion cost overrun and eventual scrapping of the carbon-capture component of the Kemper County project in Mississippi, deploying carbon dioxide capture and storage at traditional power plants has proved particularly challenging at a commercial scale.

The Capital Gap for Nascent Solutions

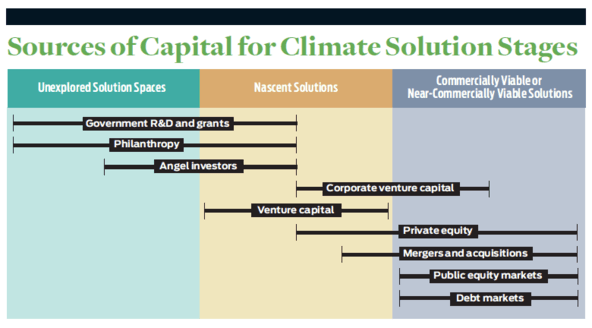

These are just three of many examples of unexplored and nascent solutions for climate change mitigation that are not receiving the funding they require in the current financial landscape. Where is the risk capital to be found to support these areas? We summarize in a chart the sources of capital that are available at each solution stage. Historically, federal governments and philanthropists have funded research in unexplored solution spaces through grants for research. Governments also often support the earliest stages of innovation. For example, the Advanced Research Projects Agency-Energy (ARPA-E) provides government grants to support the development of nascent solutions before and alongside venture capital firms. The US Department of Energy provides Small Business Vouchers through a pilot program to enable nascent companies to partner with national labs, and offers Small Business Innovation Research grants to other businesses.

Nonetheless, private venture capital is a critical source—arguably the most critical source—for the development of nascent solutions. Indeed, venture capital has helped finance 43 percent of public companies since 1979; collectively, these companies account for 57 percent of the total market capitalization and 82 percent of the research and development funding of companies in this set.8 As technologies move closer to readiness, corporate venture capital, private equity, and corporate partnerships are also critical to developing nascent solutions. A combination of project finance, asset finance, and public capital has provided the financial support necessary to achieve widespread deployment of commercially viable solutions.

Historically, venture capital has been the most effective funding vehicle for high-risk new ventures developing nascent solutions—whether related to climate change mitigation or otherwise. Since the inception and formalization of venture capital as an asset class in the early 1970s, the financial sector has assumed that venture investors are the most well-aligned source of private capital for moving ideas out of labs and into the marketplace. Therefore, although an effective innovation ecosystem demands a multitude of resources, such as human capital, novel ideas, infrastructure, and robust institutions, we focus our attention on the provision of risk capital.

While new ventures are not the only option for bringing nascent solutions to market, they have proved to be one of the most effective. This is particularly true for nascent solutions that are differentiated from incumbents and that require a distinctive understanding of the market. Despite the historically critical role of venture capital in nascent solution development and the importance of such solutions in combating the climate challenge, today’s venture capital funds are not participating in the earliest stages of financing for climate-relevant ventures. This absence creates a critical need for new funding mechanisms—a need that philanthropists are well positioned to meet.

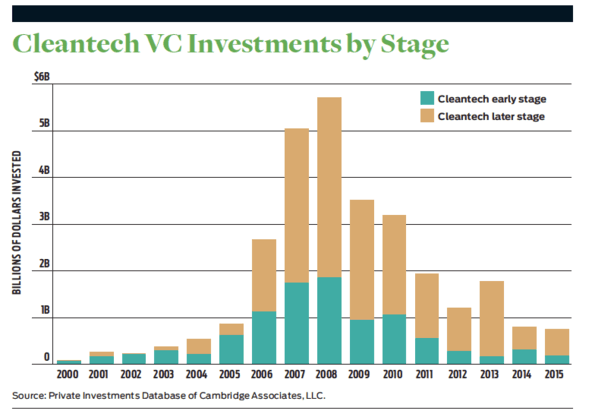

We have reviewed the total level of venture capital (VC) funding across a variety of sectors, including software, biotechnology, medical devices, and climate mitigation, and teased out the amount invested in “clean technology” (cleantech). (We have relied on information provided by Cambridge Associates LLC Private Investments Database—which includes data from institutional VC funds through year end 2015—and the National Venture Capital Association.) The data indicate that funding for climate change solutions experienced a boom and bust. Cleantech VC peaked at 16 percent of total VC dollars in 2010. However, VC funding for climate solutions fell precipitously to just 2 percent of all VC investments in 2015—its lowest level since 2005.

There are a number of reasons for the rise and fall in venture capital supporting climate solutions in the past decade. A 2016 MIT Energy Initiative report, Venture Capital and Cleantech: The Wrong Model for Clean Energy Innovation, highlights factors in the rise as ranging from high oil and gas prices to the 2007 release of Al Gore’s An Inconvenient Truth and the resulting increase in public awareness about climate change. Another driver may have been increased government support, as embodied by President George W. Bush’s 2008 creation of ARPA-E. The subsequent withdrawal of venture capital from funding climate solutions was also driven by a number of factors. High-profile busts such as Solyndra—which received more than $535 million in public (federal and state) financial support and nearly $1 billion in private funding before declaring bankruptcy—impeded political support and scared and scarred investors. Furthermore, funding under the 2009 American Recovery and Reinvestment Act—which provided “$90 billion in strategic clean energy investments and tax incentives” and was lauded by the White House as “the largest single investment in clean energy in history”—began to dry up. These factors and others led to poor overall performance for early-stage investors in climate solutions. Consequently, as total VC funding reached its highest levels in recent history ($59 billion in 2015), support for low-carbon technologies continued to decline.

In addition to the decline in overall cleantech VC investment, funding for early-stage ventures—those develop- ing nascent solutions—has been hit particularly hard. The earliest stages of venture development—seed- and Series A-stage investments—are critical for moving nascent solutions from the research setting into the commercial setting. The percentage of funding going to early-stage versus late-stage investment opportunities related to climate mitigation technologies peaked in 2002. The absolute level of early-stage funding peaked in 2008. Since those two peaks, absolute funding has plummeted, and the relative share of funding for nascent solutions has stabilized at around 20 percent.

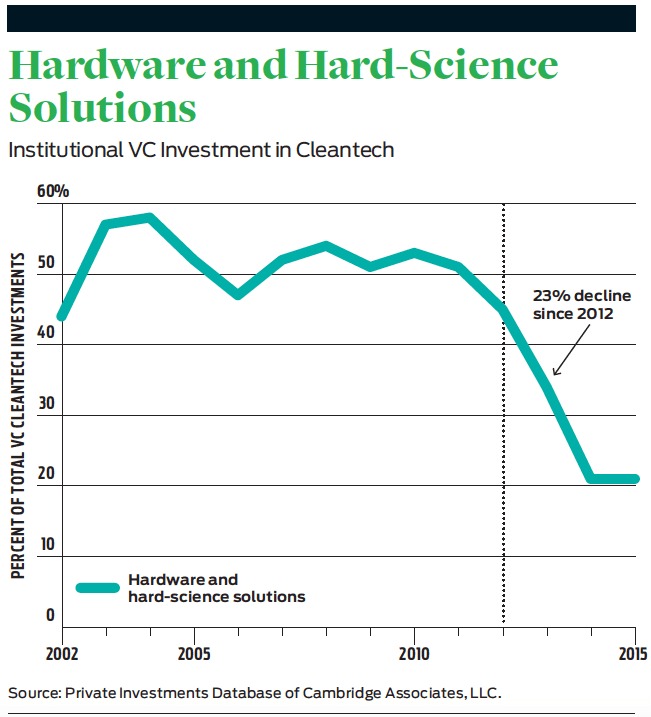

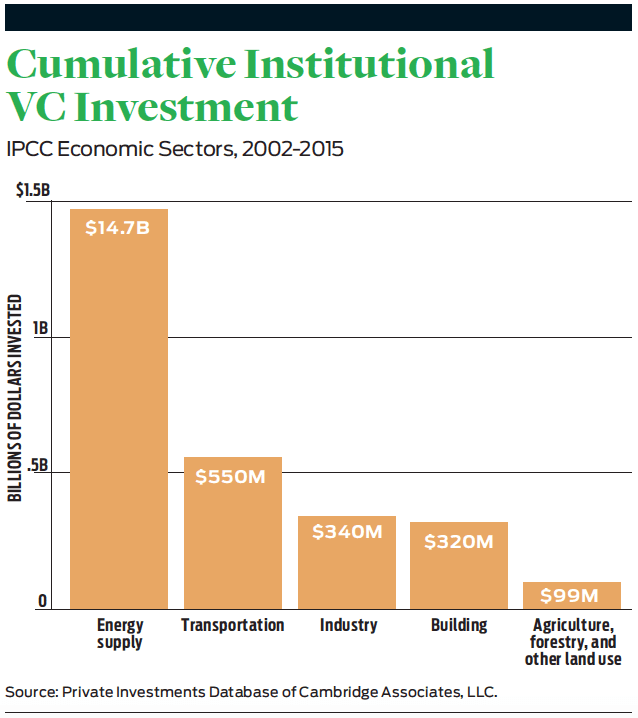

To explore which subsectors are receiving the most funding, we categorize investments based on the IPCC economic sectors. When they are broken out by subsector of investment, we see that venture investors have also moved away from investing in new hardware- or science-based solutions in recent years; this capital is now primarily owing to software or business-model solutions. As a result, the three-year average of funding dedicated to developing the next generation of climate solutions plunged from its peak of 58 percent in 2008 to 19 percent in 2015. However, society will likely need new hardware and new science-based innovation solutions to effectively combat climate change. Solutions such as negative-emissions technologies or carbon-negative cement will require the financial nurturing of nascent hardware and science technologies. This reality makes an acute funding gap particularly menacing.

As we have underscored, mitigating climate change requires funding for nascent hardware-, hard science-, and manufacturing-based ventures. But traditional venture funds are not supporting these new ventures to the degree necessitated by climate change. By mapping Cambridge Associates subsectors to the IPCC’s economic sectors, we see that specific economic sectors, such as energy supply, receive the bulk of investment. VC funding has slowed considerably in recent years for biofuels and biomaterials production, solar power manufacturing, wind power manufacturing, other power generation manufacturing, lighting, and advanced materials manufacturing. Funding for ventures that reduce the emissions from agriculture was nonexistent, even though agriculture represents nearly a quarter of all global greenhouse gas emissions.

While some have criticized the venture industry for failing to maintain a robust portfolio of investments in climate mitigation, data provides compelling evidence that this has less to do with a lack of interest or concern with climate mitigation, and more to do with an appropriate allocation of investment to meet the historical returns profile expected by investors. Unfortunately, this truth leaves nascent climate mitigation solutions with low investment levels.

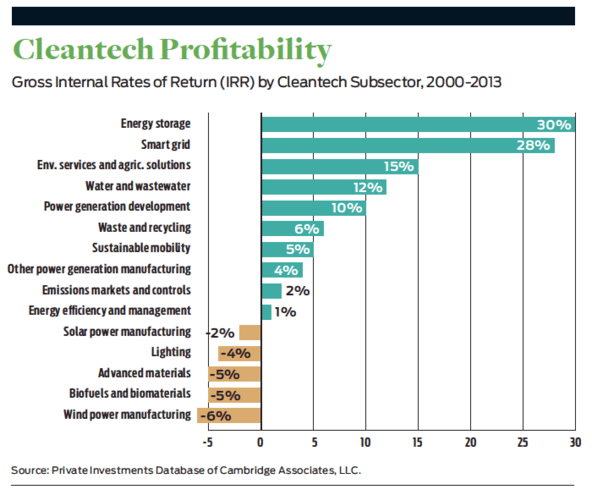

As we demonstrate in a separate chart, investments in hardware and hard-science development ventures have seen low or negative returns for investments made between 2000 and 2013. (See “Cleantech Profitability” below.) These results are echoed in the MIT Energy Initiative’s 2016 report, which reviewed clean technology returns for Series A-round investors. It found that nearly all clean technology companies funded in a Series A round after 2007 failed to return the initial capital invested.9 Over the same period, the S&P 500 gained roughly 50 percent, meaning that a private investor over the same time period could have achieved significantly better returns by investing in an S&P 500 index. The only subsectors that have seen average or above-average returns are those focused on deploying existing technologies. The pooled return for all clean-technology-related venture investments made between 2000 and the first quarter of 2017 was 4.1 percent.

In recent years, corporate VC funds—that is, venture capital groups housed within or majority funded by a corporate entity— have increased their involvement across all sectors of the innovation ecosystem. In 2015, corporate VCs participated in 21 percent of venture deals, accounting for 13 percent of dollars invested (with the remaining 79 percent of investments coming from traditional VC investors), the National Venture Capital Association reports.10 These corporate VC groups deployed an estimated $7.7 billion into 930 venture rounds, the highest investment total and deal count since 2000. While this is a positive development, the scale of the climate challenge is simply too large for them to tackle alone, especially given their imperative to focus on funding new ventures that will further their parent corporations’ interests. These interests do not always align with the goal of climate change mitigation.

The Unique Position of Philanthropists

To address climate change at scale requires continued investment in nascent climate solutions—an investment that is simply not happening in the current market. Charitable investors are uniquely positioned to help fill this gap.

Let us begin by distinguishing nascent climate solutions that might be a good fit for traditional venture capital versus those solutions that need a different type of investor, such as a philanthropist. Venture capital as an asset class has evolved over the past century. Its origins began with wealthy families making science-oriented private investments in the early 1900s. Today, the venture asset class focuses almost exclusively on companies that require small amounts of capital and produce fast financial returns. In short, VCs today prefer to fund companies such as Facebook, Instagram, Snap, Twitter, and WhatsApp rather than Intel or 3Com.11

In today’s VC market, it is nearly impossible to argue that a traditional venture investor should provide initial capital for a hardware- or science-based climate solution, when venture industry standards show that firms aim to deliver greater than 20 percent returns in less than 10 years. There are plenty of potentially commercially successful cleantech companies, but only those with an appropriate development timeline, level of technical risk, and regulatory environment, as well as appropriate capital requirements, will be funded by venture capital. This does not mean that venture capital is broken—rather, it is a highly optimized asset class that has proved to be a poor match for specific types of climate solutions.

In contrast, many of today’s unexplored or nascent climate solutions face higher hurdles. They require relatively long technical development timelines, demand capital-intensive demonstration tests that may yield negative results, tend not to receive financial valuations commensurate with technology companies of similar sizes or stages, or exist in subsectors that have delivered low financial returns over the past decade. This means that these solutions may wither due to lack of funding, regardless of whether they could ultimately deliver reductions in greenhouse gas emissions when deployed at scale.

The world needs a new and different financial vehicle to complement our existing financial system—a package that is purpose-built for unexplored and nascent climate solutions. This financial vehicle would have an appetite for long development time horizons, be able to build for-profit companies, tolerate high risk across a variety of dimensions, expect low financial returns but high social-impact returns, and have big dollars to put to work.

Although institutional investors with fiduciary priorities such as insurance companies, pension funds, university and foundation endowments, or sovereign wealth funds comprise the majority of invested capital in traditional VC funds, they all also comply with a “prudent person standard.” Accordingly, decision makers must prioritize the need to preserve their fund’s corpus and maintain regular investment income. As the data shows, this standard has ruled out investments in specific and critical types of unexplored and nascent climate solutions.

Charitable investors are uniquely positioned to design and support the new financial vehicle that the planet needs to play a critical role in mitigating the risk of investing in nascent solutions for larger institutional investors. In the United States, this group of charitable investors includes private, corporate, or community grant-making foundations; grant-making public charities; donor-advised funds; and individual donors. In 2015, US-based private foundations combined for a whopping $600 billion in assets under management (AUM), roughly $50 billion of which is granted annually. The top 10 US corporate foundations alone have approximately $10 billion in AUM, and annual corporate giving among all US corporate foundations is approximately $19 billion.

Donor-advised funds (DAFs) have continued to increase in popularity over the past 10 years; today, DAFs have approximately $70 billion in AUM and grant $13 billion annually. The 800 community foundations in the United States, which manage DAFs, grant roughly $5 billion of the $13 billion granted from DAFs annually. These numbers do not include important charitable actors such as family offices, households, and individuals that might not use a foundation or DAF structure. Individual philanthropists are critically important: In the United States in 2015, 72 percent of all charitable giving came from individuals, according to the National Philanthropic Trust.

By definition, these charitable asset owners have intergenerational timelines for investment, tolerate high risk (traditional grants have a negative 100 percent expectation of financial return), and are optimized for social outcomes rather than financial gain. Importantly, each of these charitable entities has the option to support market-based, for-profit solutions with charitable capital. Their options include providing direct equity or debt to early-stage, for-profit ventures that are developing nascent climate solutions, which foundations, in turn, can claim toward their charitable payout requirement as a program-related investment (PRI). Alternatively, they can support ventures indirectly by making a loan, equity investment, recoverable grant, grant, or donation to a public charity that in turn supports climate ventures directly.

PRIs are a clear mechanism for supporting such market-based solutions to climate change. Yet PRIs have historically been under-used in the field. Of the 5,861 PRIs on record from 1998 through 2014 with the Foundation Center, only 3 percent (172) pertain to science and engineering innovation. Less than 0.6 percent pertain to climate change mitigation. Of the 33 transactions relevant to science and engineering innovation and climate change, more than half exclusively targeted applications in the developing world. Although alleviating energy poverty is a critical and related social problem, it is distinct in many ways from reducing global greenhouse gas emissions. We are left with fewer than 15 PRIs over the past 20 years that focused on scientific solutions to climate change, in a time when investment in nascent climate solutions has never been more critical.

We interviewed dozens of philanthropists to understand why PRIs and other grantmaking mechanisms have been so underutilized in supporting early-stage solutions to climate change. Our listening tour discovered a long list of high barriers that have prevented charitable investors not only from using market-based grant mechanisms across charitable-cause areas but especially from stepping in to support nascent climate solutions to date. Most philanthropists do not know how acute the mismatch is between venture capital and nascent climate solutions, nor do they typically have the capacity to step in as a bridge between basic science and commercial impact.

For those who do, most grantmaking entities are not organizationally structured to behave like a VC firm. Deal sourcing, due diligence, and structuring of terms are outside the bounds of comfort and capacity for most charitable organizations and the grantmakers that manage them. Unfortunately, it’s nearly impossible for a charitable organization to hire the in-house talent that it would need to build a track record of success in early-stage climate investing and that may be equipped to invest across a broad and deep set of nascent solution sectors.

Last, and importantly, it is difficult for any single charitable investor to establish the “charitability” of a specific investment opportunity, for their own purposes and to comply with the tax rules that govern their grantmaking. Combined with the stigma associated with returns-focused investment that exists in the marketplace today concerning early-stage cleantech, the charitable investment community is left with skeptical advisors with their own fears of making repeat mistakes.

The world’s philanthropists have understandable reasons for today’s widespread reluctance to ll the capital gap for developing nascent solutions to climate change, especially on a firm-by-firm or individual-by-individual basis. This must change. The future of humanity depends on effective climate change mitigation and adaptation. Thoughtful philanthropic intervention to support nascent climate solutions at scale is a crucial tool in the fight against climate change. Existing asset classes will continue to fall short due to their risk tolerance and returns requirements. Philanthropists are uniquely positioned to intercede. We must do so for the good of humanity.

Read more stories by Scott P. Burger, Liqian Ma, Fiona Murray & Sarah Kearney.