The third anniversary of the Patient Protection and Affordable Care Act (ACA) has passed, and its critical implementation phase is quickly approaching. In just six months, four major ACA initiatives will take effect: Medicaid expansion, tax credits, health exchanges, and the individual mandate. As millions of previously uninsured Americans join the insurance marketplace, we’re facing the ACA’s “last mile gaps”—the enormous challenges of onboarding, educating, and serving these new consumers, particularly low- and moderate-income groups.

To illustrate these challenges, consider Bill and Anna, a newly married couple working two jobs while struggling to raise a baby. Like 25 percent of white Americans eligible for the ACA tax credit, they are unbanked, living paycheck to paycheck. Several sources could educate them about insurance options. However, without time for in-depth research, the ability to interpret complex healthcare documents, and a bank account that enables automated debit premium collection, they’re left underserved.

Moreover, if their cash flow is volatile, they are likely to underestimate their expected annual income when applying for the federal ACA subsidy. Thus, they may owe the government money at year’s end. This potential “top up” payment could cause them significant financial distress; Bill and Anna (and the majority of Americans) have very limited emergency savings. (According to a recent survey, more than half of Americans would probably be unable to raise $2,000 with 30 days notice.) Their African American and Hispanic American counterparts are even worse off: They are 43 percent more likely to be unbanked than whites and already suffer from existing healthcare disparities.

For decades, the financial industry has struggled to deliver mainstream products to those we colloquially refer to as the “underbanked.” According to a 2011 FDIC survey, more than 20 percent of US households are underbanked, meaning they lack consistent access to financing and relying heavily on high-cost, transaction-based alternatives such as payday loans. Checking accounts and prepaid cards are relatively simple—and much lower-cost—financial instruments compared to health insurance. Still, we’ve failed to provide traditional banking solutions to those in the bottom third of the population.

As such, bridging the barriers to insuring the uninsured may require a new and creative approach. Earlier this year, Omidyar Network and The Brookings Institution convened a group of policy-makers, entrepreneurs, funders, and tech gurus to discuss how cross-sector collaboration might reduce these last mile gaps. Participants included Enroll America, the Center for Medicare & Medicaid Innovation, Cigna, and the Kaiser Family Foundation, as well as start-ups and accelerators such as Luminate Health, 1776, and Health Recovery Solutions. The group identified three core areas where entrepreneurs can make a difference: onboarding, education, and financial products.

Onboarding

Enrolling uninsured or non-habitual users is the first and most formidable last mile gap. Insurers have served individuals largely through their employers, leaving little incentive to market directly to consumers. As the ACA increases the size and attractiveness of direct consumer options, successful onboarding will require building strong business-to-consumer expertise within this traditionally business-to-business-to-consumer industry.

Entrepreneurs can shape this transition by bringing users into the system. For example, mobile apps can help individuals navigate eligibility requirements for insurance subsidies and other programs based on their current status and critical life events (such as employment termination and pregnancy). Employers, acting as intermediaries, can refer their workers to companies with savvy onboarding strategies such as HelloWallet, Benefitter, and Liazon Health.

Entrepreneurs can also provide critical decision-making support to existing consumers. Platforms such as Cake Health help users manage their plans, save money, and improve their well-being.

Education

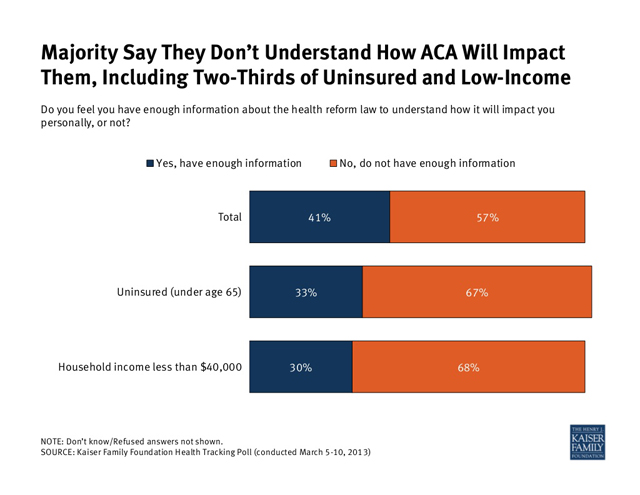

As the chart below demonstrates, most Americans have a poor understanding of how the ACA will impact them. Moreover, the nation’s 50 million uninsured are an incredibly diverse population, so we must tailor educational messaging to different demographic groups (such as Young Invincibles, older consumers, and ethnic groups). Critical areas include coverage options advising and budgeting assistance.

Cross-sector collaboration that leverages community centers, school-based health centers, established networks such as H&R Block, and mobile technology could improve education delivery in innovative and cost-effective ways. For example:

- Stories and straightforward graphics accessible via mobile phone can provide customized education, showing consumers how health insurance benefits them, helping them choose a plan, and visually depicting their treatment options.

- Platforms facilitating more frequent and seamless patient-doctor interaction can enable consumers to take greater ownership of their health. Resources such as OneMedical, ZocDoc, and HealthSpot are geared toward individuals, while community-based health plans such as PatientsLikeMe and CureTogether encourage patient-to-patient learning.

- Behavioral modification tools can also trigger better health outcomes. Examples include health apps like Mango Health, fitness apps like RunKeeper, and diet apps like Weight Watchers.

Financial Products

Significant payment obstacles threaten to stifle healthcare expansion. For example, most insurance companies plan to automatically collect premiums using consumer checking accounts. A recent report estimated that this practice would deny coverage to more than 8 million unbanked consumers eligible for ACA tax credits.

Payment solutions for the unbanked should include tools that smooth financial bumps, offer automated reminders of premium and payment deadlines, and provide flexible payment mechanisms. One promising idea involves increasing the use of pre-paid debit cards to allow those without bank accounts to make electronic health payments.

The ACA could be a game changer for those seeking to connect the underserved with insurance and other financial products. It presents a rare opportunity for entrepreneurs to maximize the social impact of billions of dollars of federal aid flowing into this market. The revenue opportunities the ACA creates may offer a compelling “backdoor” means of funding financial inclusion services. With ACA rollout scheduled for this fall, the time for harnessing its full potential is now.

So, what can entrepreneurs do? Start by sharing their ideas with incubators such as RockHealth, Blueprint Health, HealthBox, and Startup Health. Or take a risk and develop your own solutions.

Traversing the last mile gaps will be difficult, but the horizon for health innovation looks promising.

Read more stories by Chris Bishko & Kavita Patel.