The National Maritime Museum in Amsterdam—a building whose renovation in 2011 drew funding from Triodos Bank—hosts a meeting of a European Union group. (Photograph by Martijn Beekman, courtesy of the Dutch government)

The National Maritime Museum in Amsterdam—a building whose renovation in 2011 drew funding from Triodos Bank—hosts a meeting of a European Union group. (Photograph by Martijn Beekman, courtesy of the Dutch government)

When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing.” So said Chuck Prince, CEO of Citigroup, in July 2007.1 He was referring to the highly leveraged lending business that helped drive his company’s profits. At the time, Citigroup was the largest financial institution in the world, and Prince’s attitude toward the risks associated with that business model was common among bankers all around the world. Later that year, the “music” stopped, and a global financial crisis erupted. By December 2010, Citigroup had lost $147 billion in assets, and its losses continued to mount.2 The bank ultimately received a total of $476.2 billion in US government bailout funds.3

Citigroup was not alone. In one country after another, leading banks posted losses at an unprecedented scale. Many of them went into bankruptcy, and many others survived only by relying on government bailouts. The crisis revealed a pattern of illegal or unethical behavior at many banks. High-profile banking scandals from this period involved everything from money laundering to abusive mortgage practices. But in many cases, even banks that escaped these scandals had engaged in reckless business practices. In their quest for ever-greater profits, they had bought and sold a variety of complex, high-risk products that led to an accumulation of “toxic” assets.

Yet not all banks suffered losses during the financial crisis, and not all banks had fallen into the patterns of conduct that led to it. One bank that had resisted the call to “get up and dance” was Triodos Bank. “If the financial crisis has made one thing clear, it is that banks had completely lost touch with the real economy,” says Peter Blom, who has served as CEO of Triodos Bank since 1997. “You apparently need a crisis to create a consciousness [of what banking should be].” For Blom and his colleagues, the goal of banking for the “real economy” is to promote the triple-bottom-line values of “people, planet, and profit.” Banking, in other words, should focus on helping people to launch projects and build enterprises that are sustainable and socially beneficial.

Triodos grew steadily during the crisis period. Even as mainstream banks struggled to survive, this bank posted financial results that equaled or exceeded its precrisis performance. In 2008, its assets under management increased by 13 percent, and in 2009 they shot up by 30 percent. That same year, the Financial Times and the International Finance Corporation (a member of the World Bank Group) recognized this achievement by naming Triodos the Sustainable Bank of the Year.

Today, Triodos is the largest for-profit sustainable bank in Europe. Based in the Netherlands, it also operates in five other countries: Belgium, France, Germany, Spain, and the United Kingdom. The organization employs more than 1,100 people, and since 2002 its head count has increased by an average of 14 percent per year. In 2015, it had roughly €12.3 billion (about $13.6 billion) in assets under management—a figure that has grown at an average annual rate of 19 percent since 2002.

The story of Triodos is that of a “positive outlier” within the financial services industry. It is the story of leaders who decided, again and again, not to dance to the “music” that has long guided the executives at most mainstream banks. The leaders of Triodos have, over the course of its history, confronted and resisted a series of temptations—a series of pressures and opportunities that other banking leaders have generally been unable to resist. (See “The Tempting of Triodos” below.)

Incorporation

Triodos Bank traces its roots to the late 1960s, when its founders—Lex Bos, a management consultant; Dieter Brüll, a professor of law; Adriaan Deking Dura, an economist; and Rudolf Mees, a banker—formed a study group to explore ways that people could manage financial assets in an ethical and sustainable way. But the actual founding of the bank took place in 1980, at a time when neoliberal economic thinking was on the rise. During that era, the maximization of shareholder value became the Holy Grail of the financial services industry. Banks began to focus on generating ever-greater returns by trading actively in financial markets, and they poured resources into developing abstract mathematical models to calculate investment risk.

The founders of Triodos had a vision that contrasted sharply with that approach to banking. They wanted to use money exclusively to finance social, environmental, and cultural projects and enterprises that would strengthen the real economy. Early on, they laid the groundwork for the threefold mission that Triodos follows today: First, the bank aims to “create a society that protects and promotes the quality of life of all of its members.” Second, it works to help people and organizations “use their money” to further social and environmental goals and to “promote sustainable development.” And third, it strives to deliver “sustainable financial products” and superior service to its customers.4 “Triodos doesn’t take every opportunity to make money,” says Jan Lamers, a former member of the Triodos supervisory board. “Money can make the world worse. But it can also make the world better, and that’s what we aim to do with money.”

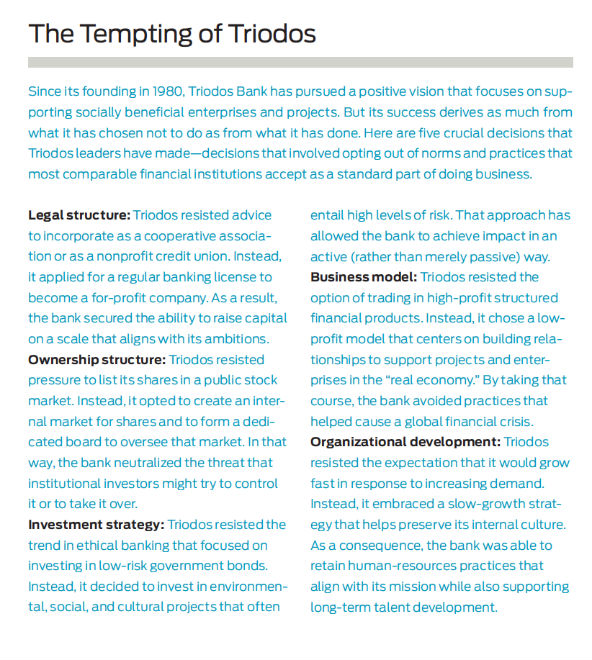

In setting up what would become Triodos Bank, the founders faced the first of the bank’s defining moments of temptation. They approached the Dutch central bank with a request for a license to incorporate their new entity as a for-profit banking institution. Why, central bank officials asked, didn’t they create a small-scale cooperative bank or a nonprofit credit union instead? That form of incorporation, after all, was common among banks that emphasized the pursuit of ethical or sustainable practices. Incorporating as a for-profit bank—especially one that issued shares to the public—was a risky choice in a world where companies treated the increase of shareholder value as their primary objective. Doing so made Triodos vulnerable to a potential take-over by institutional investors (hedge funds, investment banks, insurance companies, and the like) that would undermine the bank’s ability to honor its mission and values.

But the founders had high ambitions that they could not meet through a small institution with a nonprofit structure. So they pressed ahead with their initial plan. They did so partly because they wanted to develop an alternative model for how a for-profit corporation can operate. A current member of the Triodos executive board describes the founders’ attitude as follows: “They didn’t want to be dogmatic [about it], but they wanted to say, ‘This is a concept that would really work [to improve] society.’” That vision, this executive adds, remains “quite key to the mentality of Triodos Bank.”

Governance

To safeguard its mission, Triodos adopted a governance structure that insulates the bank’s leaders from undue external pressure. Along with an executive team that consists of the bank’s CEO, CFO, and COO, Triodos has a supervisory board that advises those executives and functions like a standard board of directors. In addition, the bank has established a separate body that oversees the administration of its shares. The Foundation for the Administration of Triodos Shares (known as SAAT, its acronym in Dutch) issues depository receipts that reflect the value of the bank’s shares, and a special SAAT board operates an internal market for trading those assets.

Any individual can buy shares directly from Triodos on its website. But the bank does not allow anyone to own more than 10 percent of the total number of shares, and the SAAT board retains voting rights for all shares. This internal market structure contrasts with the typical ownership model, in which banks list their shares on a public stock market, and it prevents institutional investors from amassing enough shares to influence (or to take over) management of the bank.

By the 1990s, Triodos had shown that it could succeed financially. At that point, regulators from the European Union (EU) began to put pressure on the bank to list its shares publicly. Triodos leaders again confronted a temptation: Should they take the path of least resistance and follow the regulators’ guidance? In this case, too, they decided to go their own way. They had designed their governance model in a deliberate effort to avoid the need to maximize short-term financial returns on behalf of shareholders. The SAAT structure allowed Triodos leaders to weigh the interests of all stakeholders—including customers, employees, and investees, as well as investors. “We always had an argument with the EU,” says one Triodos leader, who serves on the supervisory board. EU regulators contended that every market participant should be able to buy shares without limitation. But “for social entrepreneurs,” this leader explains, “it is absolutely crucial to be supported by people who understand their business—[who understand] that part of their business is social.”

To ensure that the bank meets the needs of all stakeholders, Triodos takes care in choosing members of the supervisory board and the SAAT board. Each board includes people from both business and civil society who show a strong interest in the bank’s core values. (With each board, the bank strives to achieve gender diversity as well.)

As Triodos continued to grow, and as the mainstream banking industry became ever more complex and opaque, the bank also made a serious commitment to transparency. It adopted a motto—“Know where your money goes”—that it uses today to guide its communication efforts. On its website, for example, visitors can click on a country-by-country map to locate and learn about the projects and enterprises in which Triodos has invested. “We inform our clients in a totally transparent way about the loans and investments that we make, and we go a lot further. We inform them about the salaries of our personnel, et cetera,” says Olivier Marquet, former managing director of Triodos Belgium. (Marquet left the bank in late 2015.)

Investment

During the 1980s and 1990s, the practice of socially responsible investing (SRI) steadily gathered momentum. The divestment campaign against the apartheid regime in South Africa provided inspiration, and served as a model, for other SRI initiatives. Mainstream banks started to offer SRI funds that excluded shares in companies that represented certain industries—weapons, arms manufacturing, and tobacco, for example—or that operated in countries with oppressive regimes. Small ethical-banking institutions, meanwhile, pursued strategies that revolved around investing in bonds issued by governments and municipalities in democratic countries.

For Triodos, the option to focus exclusively on one or both of these SRI approaches presented another form of temptation. But Triodos leaders chose to follow a more ambitious investment strategy. “We [don’t want] to become a traditional bank. We want to remain at the edge of innovation,” says Marquet. In that spirit, Triodos set out to create financial products—and to support projects and enterprises—that aren’t necessarily safe bets. As part of this strategy, Triodos has pioneered the use of new investment vehicles. In 1990, it launched the first investment fund in Europe for renewable energy. At the time, most competing banks considered renewables to be a very risky investment proposition. Today, it is almost impossible to find a bank that refuses to invest in that field. In 1994, Triodos launched a pair of investment funds that support microfinance efforts in emerging markets. That field, too, has become one that mainstream banks are increasingly willing to enter. Triodos went on to create the Sustainable Real Estate Investment Fund in 2004, the Triodos Culture Fund in 2006, and the Triodos Sustainable Trade Fund (a vehicle to finance organic and fair trade producers in emerging markets) in 2008.

Another aspect of Triodos’ investment strategy involves financing small startups that would otherwise be unable to access capital. In 2007, for example, Triodos invested in i-propeller, a Brussels-based startup—it’s part consultancy, part incubator, and part research lab—that supports shared value creation and social entrepreneurship. “Looking back, we were really lucky that Triodos believed in us,” says Johan Moyersoen, a cofounder of i-propeller. “In a Belgian context, our service offering was arguably 10 years ahead of its time. In the early days, at a sales pitch meeting with a business CEO, we typically needed to pull up a lot of statistics to make the point that social trends usher in important growth markets for business. Today, we can skip that part of our presentation: Businesses are not only aware of these trends; they also feel mounting pressures to engage.”

A portfolio that centers on creating new forms of ethical investment and financing early-stage ventures entails high operating costs—costs that lower the bank’s profit margin. But Triodos leaders believe that it’s necessary to devote resources to assessing each venture and the people behind it. Staff members at the bank work with each investee group to cocreate the right business model for its project or enterprise, and they bring “tenacity and passion” to that effort, says James Vaccaro, director of corporate strategy at Triodos.

One financial product that Triodos cocreated with and for its investees is a conversion loan that enables conventional farmers to shift to organic farming. When farmers make this shift, they typically see their incomes drop for about three years while they work to gain certification as organic producers. With the Triodos conversion loan, they can forgo repayment during that three-year period.

Relationships

In its engagement with investors and investees alike, Triodos practices “relationship innovation,” as one top leader calls it. Consider the bank’s corporate finance team, which works with clients that are unable to gain financing through standard channels. “Our role is to help social enterprises, charities, and environmental organizations raise risk capital from socially minded investors,” says Jeremy Pannell, corporate finance manager at Triodos Bank UK. “We operate primarily across three core sectors: social, arts and culture, and environmental. We’ve got two or three renewable projects live or in development at the moment, but we’ve also done a lot in the charity space and a lot in supporting social enterprises and ethical businesses.”

Starting in 2011, Triodos Bank UK collaborated with a pair of work integration social enterprises, Bristol Together and a sister organization called Midlands Together. These organizations buy derelict properties and then employ ex-offenders—people who have recently left prison—to refurbish them. Paul Harrod, the founder of Bristol Together, “approached us with an idea,” Pannell says. “It was a start-up initiative, with no track record, no trading history. But it had a very compelling social agenda, and the fact that it was propertybased meant that it was a potentially workable investment opportunity. We decided to support [the group] in raising a five-year bond.”

That initial bond was worth £600,000 (about $960,000), and Bristol Together used that money to buy two properties that it refurbished and sold at a profit. “So we thought, ‘We’ve got a model that can work commercially, provided that it’s in the right hands—and it does bring a social benefit,’” Pannell says. (Bristol Together employs 35 to 45 ex-offenders at any one time.) Having formed this relationship, Triodos Bank UK proceeded to help Bristol Together and Midlands Together issue bonds valued at £1 million (about $1.6 million at that time) and £3 million (about $4.8 million).

Relationships also play an essential role in how Triodos expands internationally. More than a dozen years passed after its founding before the bank opened a branch outside the Netherlands. Then, over the next two decades, Triodos opened branches in Belgium (1993), the United Kingdom (1993), Spain (2004), and Germany (2009). It also opened a representative office—a type of organization that operates with less independence than a full-fledged branch—in France (2012). The bank could have moved into these countries more quickly, but it made a deliberate choice to grow slowly.

Triodos develops new branches in a multistage process that starts when bank leaders make a connection with partners who share Triodos’ core values and who have strong roots in their communities. “We do it step by step,” says one leader who sits on the supervisory board. “We first make a business plan together [and undertake] a small project. This takes two to five years. Then we know these people quite well and suggest to them, ‘You are ready to open a branch.’ I personally would have liked to see branches in 10 to 15 countries [by now], but we only have resources to open branches in one country at a time.”

Crisis

The global financial crisis that began in 2007 shook the banking industry hard. The list of big-name companies that received government bailouts includes Bank of America, Barclay’s, Morgan Stanley, and Royal Bank of Scotland. Major banks in all parts of the world had to write down toxic assets. Prominent among these assets were derivatives, mortgage-backed securities, and other structured financial products. Such products had been hugely profitable and had allowed banks to meet—and often exceed—shareholder expectations. In the years before the crisis, bankers had brushed aside concerns about the risk of investing in these products by saying, in effect, “Everybody is doing it.”

Again and again during that period, other financial services institutions approached Triodos with opportunities to invest in structured products. In theory, these opportunities represented a powerful temptation: The high returns on such assets would give the bank additional resources that it could use to invest in socially responsible projects and enterprises. Triodos leaders, however, were quick to decline these overtures. “We did discuss it, but Triodos is not interested in that [kind of investment],” says Margot Scheltema, a former member of the bank’s supervisory board. “Triodos has a very simple pipeline.” The bank, in other words, continued to follow its original strategy: It takes in funds from shareholders and invests that money directly in projects and enterprises that align with its mission. Otherwise, it holds assets in low-risk investment vehicles.

By 2009, the financial crisis had led to a global economic recession, and mainstream banks struggled to maintain adequate levels of liquidity. Triodos faced the opposite problem. “Our challenge at the moment is that we have too much liquidity,” a senior Triodos leader said in late 2009. “We cannot immediately invest [our assets] in social entrepreneurs—not because they are not there, but because we need time.” Even so, investors poured money into Triodos. In September 2009, the bank conducted an issue of its shares that raised €100 million (about $140 million at that time), and it had to close the issue early because investor interest was so high. Other successful share issues followed in subsequent years.

At Troed y Rhiw, a sustainable farm in Ceredigion, South Wales, that receives funding from Triodos Bank, co-owner Nathan Richards works the land. (Photograph by Ashley Basil)

At Troed y Rhiw, a sustainable farm in Ceredigion, South Wales, that receives funding from Triodos Bank, co-owner Nathan Richards works the land. (Photograph by Ashley Basil)

For the first time, Triodos began to garner significant recognition from mainstream institutions. Being named the Sustainable Bank of the Year in 2009 was just one sign that Triodos was developing a higher profile. In 2010, the bank received the Queen’s Award for Enterprise from the UK government. The same year, Blom received an invitation to join the Club of Rome, a prestigious forum of thinkers and world leaders.

For Triodos leaders, the moment seemed ripe for promoting the advance of sustainable banking practices worldwide. In March 2009, the bank launched the Global Alliance for Banking on Values (GABV), a worldwide partnership of 36 independent financial institutions. These institutions have an estimated $100 billion in combined assets under management, and they reach more than 20 million people in countries that span six continents. What unites them is a commitment to supporting economically and environmentally sustainable development. GABV conducts research and engages in advocacy, and it enables collaboration and learning among members through several communities of practice. It also helped establish an investment fund called “Sustainability | Finance | Real Economies,” or SFRE. In early 2015, SFRE closed its initial round of investment with $40 million in committed funds.

Growth

Since the financial crisis, Triodos leaders have encountered more and more opportunities to expand the scale and scope of the bank’s operations. And they have consistently taken a measured approach to pursuing those opportunities.

Because of its strong performance during and after the crisis, Triodos has become an appealing target for institutional investors. Although the bank could raise equity easily and cheaply from those investors, it continues to limit their ability to buy Triodos shares. As before, the bank’s goal is to avoid the risk that large-scale investors might derail its mission or even launch a take-over bid. For that reason, Triodos puts an emphasis on attracting individual investors. As of 2015, the bank had 35,735 shareholders, and none of them held more than 10 percent of the total number of shares.

In this area, as in others, Triodos leaders focus on building relationships. “We want to know our shareholders,” says a member of the supervisory board. “If you come as an individual and want to buy shares, that’s okay. But if you come as an institution, we are going to sit down and talk with you. First, you need to be aware that you are [investing] not for the short term but for the long term. The return is about 5 percent. It could go up to 6 percent or 7 percent, but don’t think about [getting] 10 percent or 20 percent. And you have to leave the management of the bank to the bank’s management. You have to give them a free hand to [practice] innovation in our sector.”

Triodos has also been cautious about expanding its business through partnerships with other financial institutions. Since the crisis, mainstream banks have shown an increasing interest in working with Triodos either collaboratively or on a consulting basis. Triodos has deep expertise in areas such as housing and renewable energy, and other banks are now willing to pay for that expertise. But Triodos leaders are highly protective of the bank’s reputation. “We don’t want [other] banks to achieve a sort of ‘green label’ by saying, ‘We are in partnership with Triodos,’ because the fallout for Triodos could well be negative. So we take care before we go into partnership with other banks,” says Scheltema.

Perhaps the most important temptation that Triodos continues to face is one that involves the internal dynamics of the organization: To serve more customers in more places, and to invest more assets in more projects, the bank must move aggressively to hire more banking professionals. Yet Triodos leaders believe that expanding rapidly—even for the worthy purpose of achieving greater impact—would tear the very fabric of the bank. “We cannot grow faster, mostly because we cannot introduce too many new people at the same time. A too-fast introduction of new people could endanger our culture,” says Lamers.

Although Triodos works actively to recruit new talent, it also follows human-resources practices that constrain its ability to hire people at an accelerated pace. Consider its salary and bonus practices, in particular. On its website, Triodos describes its approach to compensation in this way: “Our salary system is based on the belief that the success—and earnings—of the bank depend on the combined efforts of everyone who works here.”5 The bank awards performance bonuses to employees only in special cases, and it limits the size of such payments to two months’ worth of an employee’s salary. That policy, which applies even to the bank’s top executives, marks a stark contrast to the extravagant bonus culture that characterizes many mainstream banks. “We don’t want people to join Triodos because they hope to make a packet of money,” says Scheltema. “That is a very conscious choice. Triodos uses its termsand- conditions policies as a means of attracting people who are motivated by things other than money.”

Resilience

Triodos Bank continues to ply a course of steady growth. To its shareholders, it offers an annual return on investment that ranges from 4 percent to 7 percent. It also continues to start new investment funds to serve additional markets. In 2014, for example, it launched the Organic Growth Fund, which supports organic food businesses and other consumer-oriented companies. In other ways, too, the bank continues to display leadership in the field of socially responsible banking. In 2015, Triodos became a certified B Corporation— a move that highlighted the bank’s deeply ingrained commitment to social, economic, and environmental values.

The story of Triodos Bank demonstrates that such a commitment can be the foundation for a sustainable business model. Indeed, research sponsored by GABV shows that socially responsible banks like Triodos are more sustainable—more resilient—than mainstream banks. They are less likely to suffer performance losses from economic shocks, and they recover from those shocks more quickly. The experience of the 2007-08 financial crisis shows just how fragile large financial companies can be. Their approach to banking not only threatened their own solvency; it also put the global financial system at risk of collapse.6 Triodos weathered the crisis, and proved its resilience, by adhering to value-based decisions that its leaders had made long before the crisis erupted.

A growing number of mainstream banks are trying to emulate Triodos, but whether those efforts will succeed remains unclear. Triodos has prospered in large part because it keeps all aspects of its operations—its corporate structure, its investment strategy, its business model, and its organizational culture—in close alignment. In each of these areas, it has resisted the temptation to depart from its mission or its values. Mainstream banks, by contrast, typically imitate the Triodos model in only a partial way. They confine their socially responsible banking activities to dedicated SRI or “green” funds, and they make little or no effort to change their overall investment strategy or their core business operations. This piecemeal approach is unlikely to promote resilience.

Blom, in summarizing his work at the bank, offers a simple formula for resilient banking. “Looking back on the many years I have spent at Triodos,” he says, “I am most proud of the fact that we have taught people to deal more consciously with money. We have helped ensure that money is serving people, and not the other way around. This [model] is tenable only so long as one cherishes long-term values.”

Read more stories by Ute Stephan & Marieke Huysentruyt.